3.0 for organizations maintaining accounting according to the simplified tax system, in addition to manual data entry, the opportunity is provided to fill out the KUDiR (Income and Expense Accounting Book) automatically according to the documents entered into the program.

KUDiR is a report that collects information from accumulation registers and distributes it among sections of the book.

The choice of parameters according to the order of recognition of expenses is set on the “STS” tab in the “Taxes and Reports” section, and the tax base should be determined by the type of income minus expenses:

When generating documents “Receipt to current account”, a record of income received is automatically created in the book. Let's take an example of the receipt of payment to an organization's account from a buyer:

After posting the document, an entry will be created in the KUDiR register.

Let's check it out. Go to the “Reports” menu tab, “STS” section and expand the “Book of Income and Expenses” item:

As you can see, the entry is reflected in section 1 of the book. When accounting for expenses, do not forget about the procedure for recognizing expenses specified in the accounting policy of the organization. Let's look at an example: under a supply agreement we write off advance payment to the supplier for the subsequent delivery of goods from the account:

Column 5 “Expenses taken into account when calculating tax base» is not filled in. It must be remembered that the advance payment to the supplier is included in the expense; the receipt and subsequent sale of the goods must be reflected.

We register in the program the invoice from the supplier, the sale to the buyer, after which the 5th column of the book will reflect the amount corresponding to the delivery, with VAT highlighted as a separate line:

Let's look at another example. Received materials were capitalized without prepayment. Let's create a book and check the record. She's not there:

We pay the supplier a certain amount for the supply and once again create a book:

We conclude that the expense will be recognized and reflected in the book of income and expenses only if the sequence of actions and documents is followed.

Let's consider the case in which the record of implementation does not end up in KUDiR. If the implementation was first completed in the program, and then payment was made on the previous date. To reflect the income and expenses in the book, you need to repost the sales document (sale). This has to do with making documents or adjustments. Entries for fixed assets and intangible assets will be reflected in the book only upon acceptance of intangible assets for accounting and commissioning.

Errors may appear in the report, the reason may be:

documents are not processed consistently;

when using the “Operation” document, the type of operation is incorrectly specified;

The organization's accounting policy is incorrectly configured.

It is possible to make entries manually in KUDiR. In this case, the document “Income and Expense Book Entries” is used, which is located on the “Operations” menu tab, section “STS”.

For clear example let's create a receipt cash order to receive cash at the cash register manually and create a book:

We see that there is a record in KUDiR, which means the operation was completed correctly.

How to configure KUDiR in 1C 8.3

Before you start creating KUDiR in 1C 8.3, you need to make a number of settings. This will avoid incorrect filling. Let's open and configure the accounting policy.

Where is the income and expense accounting book in 1C 8.3? Let's move on: Main – Settings – Accounting policies:

Then you need to select the one you need from the list of organizations and open its accounting policy:

If the object of taxation is set to Income minus expenses, then in 1C 8.3 access to the button Procedure for recognizing expenses is activated:

This function is used to select events that are needed in order to recognize expenses as reducing the tax base for single tax:

Some events have a checkbox that cannot be unchecked. This means that an event must occur in order for an expense to be recognized. Other checkboxes can be checked or unchecked depending on the needs of the organization:

- To get into KUDiR material costs you need to check the boxes: receipt of materials and payment of materials to the supplier.

According to current legislation, to account for acquisition costs material assets there is no need to check the boxes Transfer of materials to production and Reducing costs for the balance of work in progress.

- For recognition and inclusion in KUDiR expenses for purchasing goods events are required: receipt of goods, payment of goods to the supplier and sale of goods.

According to current legislation, the costs of paying for the cost of goods purchased for further implementation, are recognized as these goods are sold. Therefore, to account for these expenses, you need to check the Sales of goods checkbox.

Flag Receiving income (payment from the buyer) you can not put it without fear of consequences, thanks to amendments to the legislation since 2011.

- To reflect input VAT in KUDiR you need to check the following boxes: VAT is presented by the supplier and VAT is paid to the supplier.

Also in this section there is also a checkbox Accepted expenses for goods (works, services). Each organization decides whether to install it or remove it independently. If you do not check the box, then the incoming VAT will go to KUDiR without waiting for implementation.

- For add. expenses included in the cost the main points are: Receipt of additional. expenses and payment to the supplier. If these 2 conditions are met, then the expenses will be reflected in the KUDiR without waiting for the inventory to be written off.

If you check the Write-off of inventories (this includes additional expenses) checkbox, the following condition will be met: additional. expenses will wait for sale and when the write-off (sale) of goods occurs, then additional expenses will be added. expenses will be in KUDiR.

- For customs payments The following are considered mandatory: The import of goods has been formalized and Customs duties have been paid.

There is also a third checkbox: Products written off. If it is supplied, then customs payments will be included in the expenses and will appear in the KUDiR only after the goods are sold. There is a certain document (Letter of the Federal Tax Service of the Russian Federation for Moscow dated August 3, 2011 No. 16-15/0759978), which prescribes doing exactly this. Therefore, it is better to check the box to avoid tax claims.

For more details on how to set the procedure for recognizing expenses in the parameters of the Accounting Policy under the simplified tax system in 1C 8.3 Accounting 3.0, read Or watch our video lesson:

Now you need to go to KUDiR and directly configure it in 1C 8.3. KUDiR is in the section Reports – simplified tax system – book of income accounting and expenses of the simplified tax system:

In the book form itself, click on Show settings:

To display detailed transcripts of strings, you need to check the Show transcripts checkbox:

What inaccuracies can be allowed when determining the costs of acquiring fixed assets for tax accounting when application of the simplified tax system“Income minus expenses” watch in our video:

How to fill out KUDiR in 1C 8.3

Now, after all the settings have been made, we will create KUDiR.

Important! Let us remind you once again that before forming KUDiR in 1C 8.3, it is necessary to close the month and restore the sequence.

On title page KUDiR, in addition to other data about the organization, it is necessary to ensure that the Object of taxation field is filled in.

KUDiR is divided into 4 sections:

- Income and expenses– income and expenses are recorded chronologically.

- Expenses for fixed assets and intangible assets– costs for the purchase, construction of fixed assets and intangible assets are reflected (only for enterprises that have chosen “income minus expenses”).

- Calculation of the amount of loss– losses are recorded that reduce the single tax base (only for enterprises that have chosen “income minus expenses”).

- Reducing the tax amount– paid payments are recorded insurance premiums“for yourself” and for employees, if any, by the amount of which the simplified tax system tax is reduced (under the simplified tax system “income”):

If the accounting policy settings are correctly completed, filling out KUDiR in 1C 8.3 will happen automatically and without any special difficulties. And the question will not arise why KUDiR is not formed in 1C 8.3.

How to avoid mistakes with the simplified tax system in 1C 8.3 and correctly reflect some types of income and expenses in KUDiR, read Or watch the following video:

Manual adjustment of KUDiR records

Sometimes an accountant is faced with the need to adjust KUDiR records. For this purpose, 1C 8.3 provides a document Entries in the book of income and expenses (USN). It's easy to find: Transactions – simplified tax system – entries in the book of income and expenses (USN):

The form that opens asks you to fill out the following document:

- Organization – select from the list of the Organization directory the desired organization that uses the simplified tax system (if there are several of them);

- date – by default the current number;

- Number – will be filled in automatically when you post the document:

- Income and expenses – data is entered to adjust section 1 of KUDiR;

- Calculation of costs for purchasing an OS – OS data is entered to adjust section 2 of KUDiR;

- Calculation of costs for the acquisition of intangible assets – data on intangible assets is entered to adjust section 2 of KUDiR:

After completing the document, the data will be included in KUDiR in the appropriate sections:

Checking the correctness of filling out KUDiR

1C 8.3 has a report which will help ensure that the KUDiR is filled out correctly. It's easy to find: Reports – Accounting Analysis – Status Analysis tax accounting according to the simplified tax system:

In the form that opens, just select the period, organization and click Generate. Each number can be deciphered by simply clicking on it:

For organizations operating under a simplified taxation system, the program implements the ability to automatically fill out the Income and Expense Accounting Book () based on primary documents. In addition to automatic completion, the program also allows you to fill out the report manually.

It is important to know that when drawing up the report, the data from the “Book of Income and Expenses (Section I, II, III, IV)” is used - for each section separately.

For organizations where the tax base is determined by the formula income minus expenses, we recall that the procedure for recognizing expenses is determined in the register, on the simplified tax system tab:

Income accounting

Thus, if, for example, we reflect an organization in the program, then the income is automatically reflected in KUDiR.

Example 1:

To compile a Book of Income and Expenses in the form of a report, you need to go to the menu Reports – simplified tax system – book of income and expenses simplified tax system:

Expense accounting

As for expenses: first of all, you need to remember the procedure for recognizing expenses (setting up accounting policies).

Get 267 video lessons on 1C for free:

Example 2.

As you can see, column 5 “Expenses taken into account when calculating the tax base” is empty. At the same time, we remember that according to the procedure for recognizing expenses, before an expense in the form of payment to the supplier is recognized, delivery must be made.

As you can see, the cost of the received goods was included in the KUDiR. Input VAT it is displayed as a separate line.

Example 3.

What happens if the prepayment is excluded from the previous example?

In this example, we once again see that an entry in the Income and Expense Book appears only if the sequence of expense recognition is followed.

What to do if the entry does not fall into KUDiR or the book is not filled out?

In addition to the above program algorithm, it should also be noted that the sequence of documents also plays a role. That is, if, first of all, the system reflected the delivery, and then the payment “retroactively,” then it is required, for example, that the entry appear in KUDiR (this only applies to non-compliance with the sequence of entering documents into the system or adjusting the amounts of documents).

If we talk about fixed assets and intangible assets, then the corresponding records will appear in KUDiR only after or .

Article 346.24 of the Tax Code of the Russian Federation obliges firms and individual entrepreneurs who have chosen the simplified tax system to keep tax records through the Book of Income and Expenses (hereinafter referred to as KUDiR, Book). Violation of this requirement threatens the company with a fine of up to 10 thousand rubles per tax period. If the violation affects more than one such period, the fine will be up to 30 thousand rubles (Article 120). The KUDiR matrix, as well as the rules for filling it out, were approved by order of the Federal Tax Service of Russia dated October 22, 2012 No. 135n. In absolute accordance with it, 1C implements the functionality for creating a Book.

How to configure KUDiR in 1C 8.3

Setting up the compilation of a Book in 1C 8.3 should begin by checking the tax and reporting settings in the main menu.

If you find that any expenses or income are not reflected in the KUDiR, the problem should be looked for in this section.

You can also check your tax and reporting settings in another way by going through the “Main” menu, then “Accounting Policy”.

We find ourselves in the “Taxes and Reports Settings” menu.

Here you need to pay attention that there are a number of settings that cannot be edited due to requirements current legislation. At the same time, it is possible to make some amendments to the established policy, in particular to the “Transfer of materials to production” in the section “ Material costs" You can also check the box for receiving income (payment from the buyer) in the “Expenses for purchasing goods” section. In the “Input VAT” section, it is possible to accept expenses for purchased goods, works, and services. At the discretion of the taxpayer, it is established to include in the formation of KUDiR the costs of writing off goods (section “Customs payments”) or inventories (section “ Additional expenses, included in the cost").

How to fill out KUDiR in 1C

Like most reports in 1C, KUDiR is generated automatically based on the results of reporting or tax periods. After regulatory operations At the end of the month, the accountant needs to go to “Reports”, to the “STS” section - “STS Book of Income and Expenses”.

It is possible to select the desired tax period(this is a quarter, six months, 9 months and a year). By clicking the “Generate” button, a printed form of the Book is displayed on the screen.

On the left side is a list of sections:

- Section I. “Income and Expenses” shows all business transactions for the period in tabular form in chronological order, indicating the amounts.

- Section II. “Expenses on fixed assets and intangible assets” reflects information on expenses on fixed assets and intangible assets for the period. For organizations that have chosen the simplified tax system - income minus expenses.

- Section III. “Calculation of loss” is filled in if there are losses that reduce the company’s tax base for a number of years.

- Section IV. “Tax reduction” shows amounts that (clause 3.1 of Article 346.21 of the Tax Code) reduce the amount of calculated tax, for example, for insurance contributions to the Pension Fund or other contributions.

- Section V “Trade fee” reflects the amount of the trade fee, which reduces the amount of tax due for payment.

When you click on each line of a section, the corresponding generated report window opens on the right.

When you click the “Show settings” button, the KUDiR form settings open.

It is possible to display transcripts, include the columns “Income of total”, “Expenses of total” and “VAT printing mode”. When you check the box in the line “Include in the report form and fill out” and during the subsequent formation of the KUDiR, columns of all income and expenses are displayed on the screen, including those taken into account when calculating the tax base. This function allows you to visually monitor indicators that are not included in tax accounting.

Double-clicking on the indicator line allows you to display the primary document that served as the basis for inclusion in KUDiR.

The generated KUDiR form can be printed in the context of the sections of interest.

Manually making changes to KUDiR

For example, during visual inspection of KUDiR it was discovered that for some reason the expense recognized in tax accounting did not fall into the column “Including expenses taken into account when calculating the tax base.”

Double-click on this line to open the primary document.

We hover the cursor over the fourth button in the panel, the note “Show transactions and other movements of the document” pops up, when clicked, the movement of the document in accounting and tax accounting opens.

Go to the section “Book of Income and Expenses (Section 1)”.

At the top of the document, check the “Manual adjustment (allows editing of document movements)” checkbox. Then you can enter the amount of the document in the “Expenses” column.

In the KUDiR menu, press the “Generate” button again. The program will ask you to update the information as changes have been made.

With the subsequent formation of KUDiR, we see that expenses are reflected in both columns - both in accounting and tax accounting.

There is also another way to manually make changes to KUDiR. To do this, you need to select the section “Records of the book of income and expenses of the simplified tax system” in the “Operations” menu.

In the window that opens, we will generate an arbitrary document for the amount of making the necessary adjustments, in our example - 1.0 million rubles to the supplier for the goods supplied.

After of this document, we move on to the formation of KUDiR and see the line with our adjustment.

Analysis of accounting status

The finished book of accounting for income and expenses in 1C is analyzed in the “Reports” menu, then “Accounting analysis according to the simplified tax system”.

In the window that opens, select the period to be analyzed and click the “Generate” button.

Various items of income and expenses are displayed on the screen in the form of a block diagram. By clicking on each cell you can see a list of primary documents included in it. This function is successfully implemented in management accounting.

Carrying out accounting in the 1C program eliminates errors interpreted by regulatory authorities as a gross violation of accounting and reporting requirements. The program is aimed at maximum control of work accounting service and its individual links.

Simplified tax system: recognition of income and expenses (1C Accounting 8.3, edition 3.0)

2016-12-08T11:39:01+00:00Today we will look at a topic that raises perhaps the largest number of questions from novice (and not only) accountants - the procedure for recognizing income and expenses under the simplified taxation system (STS) in the 1C: Accounting 8 program family.

We will consider examples in 1C: Accounting 8.3 (edition 3.0). But in the “two” everything works the same way.

A short excursion into theory

We are interested in filling out the book of income and expenses (KUDIR). In this wonderful book:

- Column 4 is the “Total Income” column

- column 5 is “Accepted income”

- column 6 is the column “Total expenses”

- column 7 is “Accepted expenses”

We are primarily interested in columns 5 and 7. They influence the amount of the single tax we pay.

There are two main modes in "simplified":

- income (column 5)

- income (column 5) minus expenses (column 7)

To calculate the single tax, in the first case we simply multiply the amount of income by 6%, and in the second case we multiply the difference between income and expenses by 15%.

That's all in a nutshell.

Correctly calculating income and expenses is the most difficult task. Already based on the presence of four columns “total income” and “accepted income”, “total expenses” and “accepted expenses”, it turns out that not all income and expenses can be taken to calculate the tax.

You need to be able to correctly determine the moment of recognition of income or expense. Under the simplified tax system for this in mandatory used cash method.

Under the cash method, the date of receipt of income is the day the funds are received in bank accounts or at the cash desk. And it doesn’t matter whether it’s an advance or payment. The money has arrived - income has been received, and therefore immediately falls into columns 4 and 5.

As you can see, with income everything is extremely simple. Any receipt of money (to the cash register or to the current account) falls into general and recognized income, on which tax must be paid.

With expenses, things are a little more complicated.

For recognition expenses for purchasing materials- it is necessary to reflect the fact of their receipt and payment.

For recognition expenses for payment of services provided to us- it is necessary to reflect the fact of their provision and payment.

For recognition expenses for purchasing goods for subsequent resale - you need to reflect the fact of their receipt, payment and sale.

For recognition labor costs- you need to reflect the fact of its accrual and payment.

When paying via expense reports- in addition to the above conditions, it is necessary to reflect the fact of issuing money accountable person.

As you can see, for many of the listed situations there are several conditions for recognizing expenses. And these conditions can be met in different orders. In this case, the moment of recognition of the expense will be considered last condition met.

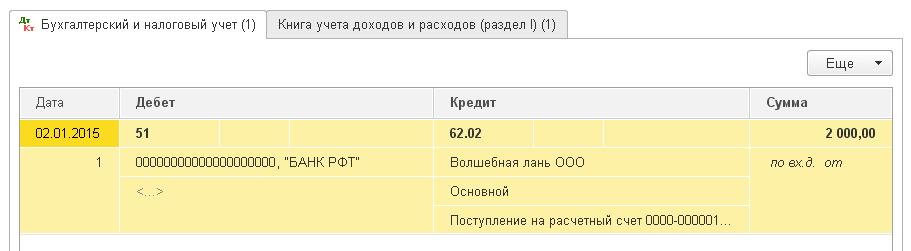

Advance payment from buyer to bank

The buyer transferred money to our bank account as an advance payment (advance payment). According to our assumption (cash method), this amount will immediately fall into “Total Income” (column 4) and “Accounted Income” (column 5):

bank receipt -> column 4 + column 5

We issue a statement (receipt to the current account) for 2000 rubles from the buyer of Magic Hind LLC:

We post and open document transactions (DtKt button). We see that the payment amount was assigned to 62.02 - everything is correct, because this is an advance:

Immediately go to the second tab “Income and Expense Accounting Book”. It is here that payment amounts are posted (or not posted) in the KUDIR columns. We see that the 2000 rubles received immediately fell into columns 4 and 5:

Advance from the buyer at the checkout

With a cash register, everything is similar to a bank. The buyer paid money to the cash register as an advance payment (advance payment). According to our assumption (cash method), this amount will immediately fall into columns 4 and 5:

cash receipt -> column 4 + column 5

We issue a cash receipt order (cash receipt) from the buyer "Svergunenko M. F." for the amount of 3000 rubles:

We post the document and go to its postings (DtKt button). We see that the payment amount was assigned to 62.02 - everything is correct, because this is an advance:

We immediately go to the “Income and Expenses Accounting Book” tab and see that our entire amount falls into columns 4 and 5:

Payment to the supplier for services rendered

Let's move on to expenses. This is where things get more interesting. But not in the case of payment for services provided to us. We just need to enter the act of provision of services and its payment into the program, then the act itself (according to the cash method) will not make any marks in the KUDIR columns, but the bank statement will immediately post the amount of payment in columns 6 and 7:

certificate of provision of services -> will not do anything

payment by bank -> column 6 + column 7

We enter into the program a certificate of provision of services from the supplier Aeroflot in the amount of 2500:

We post the document and go to its postings (DtKt button). We see that expenses (26th invoice) were attributed to 60.01 - everything is correct:

We do not see the “Book of Income and Expenses Accounting” bookmark, which means that the indicated 2500 did not fall into any of the KUDIR columns. Go ahead.

The next day we submit a statement of payment for the services provided to us:

We carry out the statement and look at its postings. We see that the payment amount was applied to 60.01:

We immediately go to the “Income and Expenses Accounting Book” tab and see that the paid 2,500 finally fell into columns 6 and 7:

Advance payment to the supplier for the provision of services

What if we made an advance payment to the supplier for services provided (advance payment)? And only then they issued an act of provision of services. Schematically it will look like this:

payment by bank -> fill in column 6

act of provision of services -> fill out column 7

Let’s enter into the program a bank statement (our advance payment to the supplier) in the amount of 4500:

Let’s post the document and open its postings (DtKt button). We see that the amount fell on 60.02 - everything is correct, because this is an advance:

Let’s immediately go to the “Income and Expenses Accounting Book” tab and see that the advance amount is included only in column 6:

And it is right. According to the cash method, in column 7 (accepted expenses), we will be able to take this amount only after entering the certificate of provision of services. Let's do it.

We will add an act of service provision to the program the next day:

Let's go through the document and look at the postings:

Let’s immediately go to the “Income and Expenses Accounting Book” tab and see that the payment amount finally falls into the seventh column:

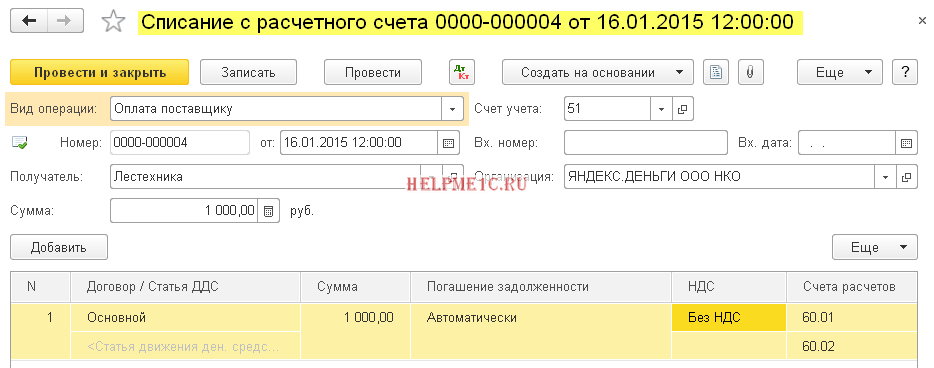

Payment to the supplier for materials

Important!

Further we will reason like this. We use the cash method. First there was the receipt of materials, then payment by bank. Obviously, it is the payment by bank (since there has already been a receipt) that will create entries in columns 6 and 7. Schematically it will be like this:

receipt of materials -> will not create anything

payment by bank for materials -> fill in column 6 and column 7

Let’s enter into the program the receipt of materials in the amount of 1000 rubles:

We see that the “Income and Expenses Accounting Book” tab does not appear next to the transactions. This means that the goods receipt document in in this case did not create records for any of the KUDIR columns.

We will issue a statement of payment for materials the following day:

Let’s post the document and open its postings (DtKt button):

Let’s immediately go to the “Income and Expenses Accounting Book” tab and see that the document has filled out columns 6 and 7:

Advance payment to the supplier for the supply of materials

Important! First, let’s correctly set up the procedure for recognizing expenses in accounting policy - .

In this case, payment comes first, then materials arrive. According to the logic of the cash method, full recognition of expenses (column 7) will be possible only after both documents have been completed. Schematically it would be like this:

payment by bank for the supply of materials -> fill out column 6

receipt of materials -> fill in column 7

Let’s add into the program a statement about the prepayment for materials for 3,200 rubles:

Let’s post the document and open its postings (DtKt button):

Let’s immediately go to the “Income and Expenses Accounting Book” tab and see that the statement has so far filled out only column 6 (total expenses):

To fill out the seventh column, the receipt of materials document is missing. Let's format it:

We post the document and look at its postings (DtKt button):

We immediately go to the “Income and Expenses Accounting Book” tab and see that the document receipt of materials has filled in the missing column 7:

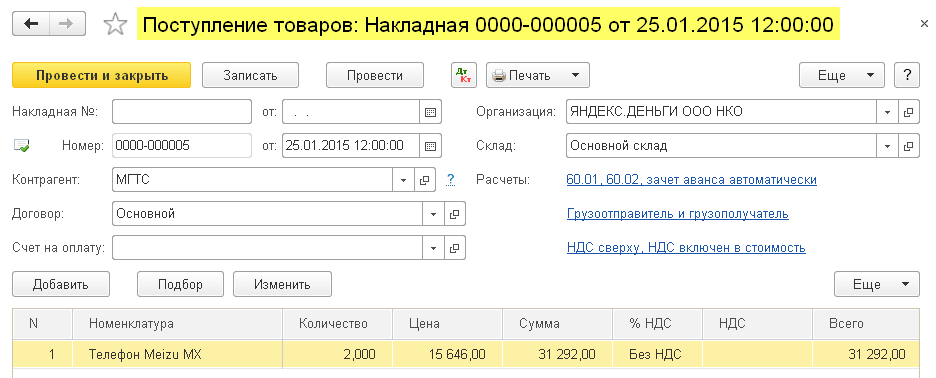

Payment to the supplier for goods

Important! First, let's correctly set up the procedure for recognizing expenses in the accounting policy -.

In general, the procedure for recognizing expenses for the purchase of goods for sale is similar to the situation with the receipt of materials - receipt and payment are also required here. But an additional (third) requirement is that expenses are recognized only as purchased goods are sold.

Schematically our scheme will be like this:

goods receipt -> fills nothing

payment for goods by bank -> fill out column 6

sales of paid goods -> fill out column 7

Let’s enter into the program the receipt of goods in the amount of 31,292 rubles:

Let’s post the document and open its postings (DtKt button):

We see that the “Income and Expense Accounting Book” tab is missing, which means the document did not record anything in the KUDIR columns.

Let's enter a statement of payment for goods to the supplier:

Let’s post the document and open its postings:

Let’s immediately go to the “Income and Expenses Accounting Book” tab and see that the payment amount is included in the total expenses (column 6). This amount will be included in the seventh column (expenses accepted) as the goods are sold.

Let's assume that all the goods are sold. Let's formalize its implementation:

Let’s post the document and open its postings (DtKt button):

Let’s immediately go to the “Income and Expenses Accounting Book” tab and see that the payment amount finally falls into the seventh column:

Advance payment to supplier for goods

Important! First, let's correctly set up the procedure for recognizing expenses in the accounting policy -.

Everything here is similar to paying the supplier for goods (previous point). Except that the payment amount will be included in the sixth column in the first document (bank statement). The scheme will be like this:

payment for goods by bank -> fill in column 6

goods receipt -> will not fill anything

sale of paid goods -> fill in column 7

Payment to the supplier through an advance report

Important! First, let's correctly set up the procedure for recognizing expenses in the accounting policy -.

If, in any of the situations described above, you replace payment by bank with payment through an accountable person, everything will work exactly the same.

But there is a nuance. The main condition for the expenses paid under advance report(in addition to those listed above) is the actual issuance of money to an accountable person (expenditure cash order).

Column 6 will be filled in with the RKO document.

Column 7 will be filled in when the next additional conditions: advance report+ (act of service provision or receipt of material or receipt of goods and its sale). Moreover, this column will be filled in with the document that is the latest in date.

Payment of wages

To fill out columns 6 and 7, you must have two documents at once: accrual and payment of wages.

Scheme 1:

payroll -> will not fill in anything

issuance of wages (RKO) -> fill in column 6 and column 7

Scheme 2:

issuance of wages before accrual (RKO) -> fill in column 6

payroll -> fill in column 7

We're great, that's all

By the way, for new lessons...

Sincerely, Vladimir Milkin(teacher and developer