To accrue financial assistance to employees in 1C ZUP 3.1, configure the salary calculation; if necessary, you can further configure or create calculation types for accrual and register financial assistance either in a document Material aid , or a document Vacation(if you need to accrue financial assistance for your vacation).

To calculate financial assistance to former employees, use a document Pay former employees .

Financial assistance in general (except for financial assistance for vacation)

Setting up 1C ZUP 3.1 for calculating financial assistance

In the payroll settings, check the box ():

As a result of checking the box, three types of accrual with the purpose will be added Material aid :

Each of these types of accrual has its own characteristics of setting up taxation and is used for registration various types financial assistance:

If necessary, by copying based on these types of calculations, you can create new types of accrual if, for example, it is customary in an organization to divide financial assistance not only according to methods of taxation, but also on some other basis, for example, according to the method of reflection in accounting. The main thing is that the purpose is indicated in the accrual type settings Material aid and is executed According to a separate document :

Using the document “Financial Assistance”

Calculation of financial assistance in 1C ZUP 8.3 in general case(except for financial assistance for vacation) complete in the document Material aid , which becomes available after checking the checkbox Paid material aid employees in the payroll settings.

In the document:

When registering financial assistance by code personal income tax 2760 (by default this is the accrual type Material aid ) a deduction is applied 503 V maximum amount 4,000 rub. Since 4,000 rub. - this is the amount of the annual deduction for financial assistance, then in the 1C ZUP 3.1 program it is tracked what the amount is by the deduction code 503 was applied for each employee in the current calendar year.

For Financial assistance at the birth of a child (personal income tax code 2762 ) it is important to indicate in the document Amount of children for the deduction to be applied 508 :

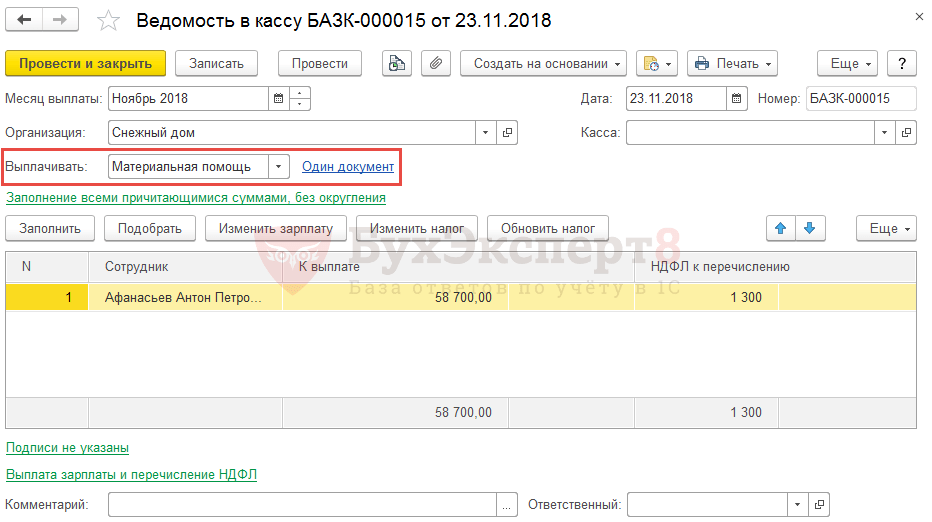

Payment of financial assistance

In case of payment of financial assistance during the inter-payment period, the payment in 1C ZUP 3.1 can be registered directly from the document Material aid on command Pay out .

As a result, a document will be created Statement... with payment method Material aid and with reference to this document Material aid .

You can also create a statement independently, directly from the statement journal, indicating the payment method Material aid and selecting the documents for which the payment is made.

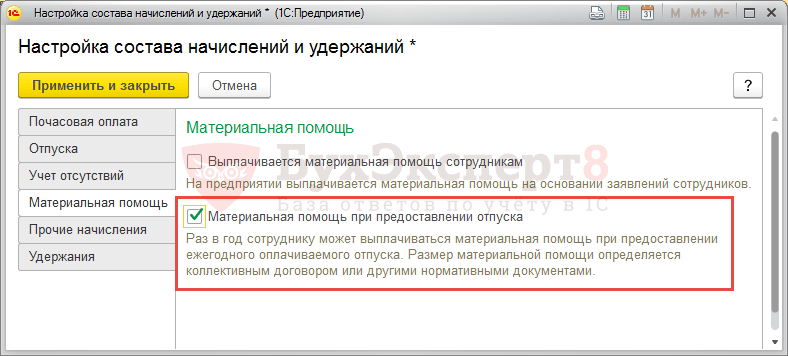

To calculate financial assistance for vacation in 1C ZUP 3.1, in the salary calculation settings, check the box Financial assistance when providing vacation (Settings – Payroll calculation – Setting up the composition of accruals and deductions – Financial assistance tab):

As a result of checking the box, the accrual type will appear Financial assistance for vacation . By default, the accrual type has a formula for calculating the amount that is a multiple of the salary (the multiple is set during the initial setup of the program). If necessary, the formula can be edited.

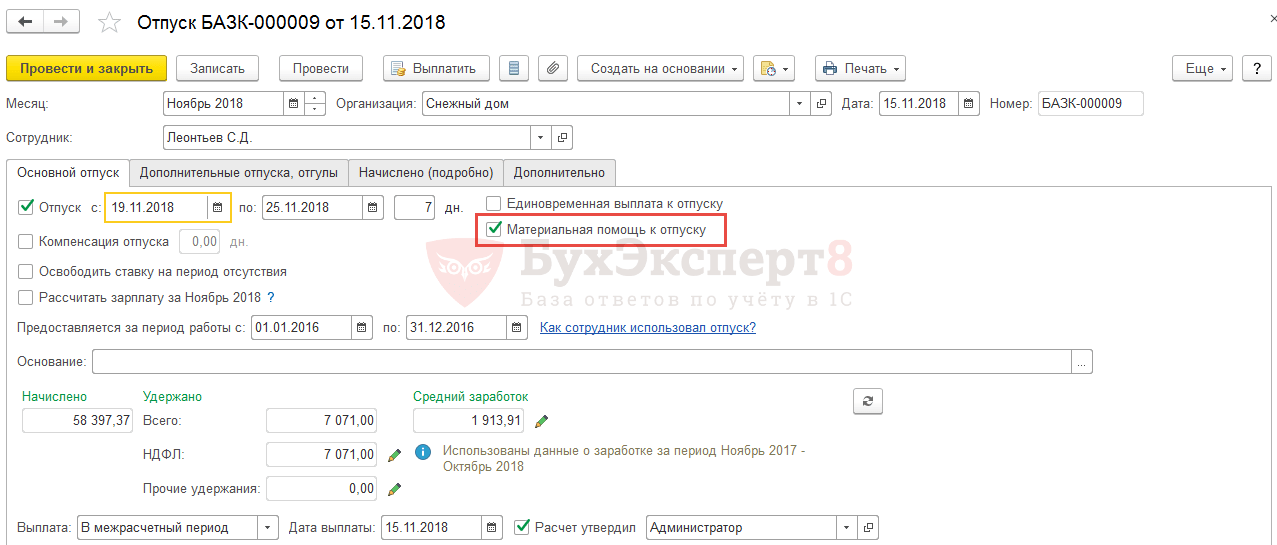

Reflect the accrual of financial assistance for vacation in 1C ZUP 3.1 in the document Vacation. To calculate such financial assistance, check the box on the main tab Financial assistance for vacation :

As a result, on the tab Accrued (details) calculation will occur according to the type of accrual Financial assistance for vacation :

Payment of financial assistance for vacation occurs along with vacation pay. The statement can be entered either directly from the document Vacation on command Pay out, or in the document journal Statement..., indicating the payment method Vacation and the document itself according to which the payment is made.

Financial assistance to former employees

The employer can also pay financial assistance to former employees. To register such financial assistance in 1C ZUP 3, in the salary calculation settings, check the box Income is paid to former employees of the company .

After that in the directory Types of payments to former employees Define the settings for paid financial assistance: personal income tax code and type of income from insurance premiums. Several types of financial assistance can be described with different settings, if required.

Please indicate the required type of payment in the document. Payments to former employees , select former employees (from the directory Individuals ) and indicate the amount of assistance paid.

Document Payment to former employees in 1C ZUP is used for the purposes of accounting for personal income tax, contributions and generating data in the document Reflection of salaries in accounting . Document Statement for calculating payments to former employees is not entered into the ZUP. It is assumed that settlements with former employees are recorded in the accounting program.

Watch our video tutorial on calculating financial assistance in 1C ZUP 3.1:

In this case, the accrual of assistance can be issued either at the request of the employee or at the initiative of the company. You can make a payment in two ways:

- as other expenses;

- as part of net profit.

In accordance with the law of the Russian Federation, Article 23 Art. 270 of the Tax Code, financial assistance that was included in the list of other expenses is not taxed. Thus, financial assistance should be posted to account 84.

Thanks to the program "1C: Salary and Personnel Management" 3.1. calculating financial assistance is not only faster, but also much easier, since you can immediately see all the deductions, the amount the employee will receive and other details regarding this type of expense.

Typically, financial assistance is a one-time payment.

Setting up 1C:ZUP 3.1

In some programs, the financial assistance payment function may be disabled. Therefore, you first need to activate it in the “Financial Assistance” document.

After this, you can apply for financial assistance due to the birth of a child, marriage, loss of a relative or illness.

To register a document for payment of financial assistance, you first need to create and fill it out. In the fields we indicate the following:

- In the “Month” column – indicate the month of registration of financial assistance in the program;

- Type of payment;

- Date of payment;

- Accrued. In this field, enter the amount of assistance;

- The amount of the deduction. This field is calculated automatically;

- personal income tax;

- To payoff. The amount that a person will receive “in hand”;

- Contributions. In this field, enter the amount of insurance premiums.

Financial assistance is paid interpayment or together with wages.

Example of registration of payment of financial assistance in the program

Below we will look at an example of registering the accrual of financial aid due to illness for a former employee who has already retired.

To calculate financial assistance to employees who no longer work for the company using this program, you need to go to the calculation settings and activate the function of paying former employees:

After this, in order to see exactly what insurance premium and personal income tax will be for this operation, we set up a directory:

There we select the appropriate type of payment, depending on the reason for the payment (payment in connection with retirement, reimbursement of the cost of medicines, etc.).

Registration of payment transaction

This document can also be in printed form:

When the accrual is completed, you should check the postings.

The provision of additional financial assistance to an employee by an enterprise is a fairly common occurrence. Therefore, 1C: ZUP provides the possibility of accounting for financial assistance in connection with the birth of a child, marriage, study or illness leave, as well as accounting for accruals to a former employee.

By decision general meeting founders of the organization, the amount of financial assistance payments may be included in the net profit or be added to other expenses.

As stated in paragraph 23 of Art. 270 of the Tax Code of the Russian Federation, the amount of material assistance included in other expenses is classified as expenses not taken into account for profit tax purposes. Therefore, if a company decides to provide financial assistance from retained earnings, then the posting will be carried out to account 84, otherwise account 91.02 will be used, and these are other expenses.

As an example, let's look at how to reflect in the software solution “1C: Salary and Personnel Management” ed. 3.1. reflection of financial assistance allocated to a retired former employee, Mamontova A.V.

Mamontova A.V. was provided with financial assistance in the amount of 20,000 rubles, since she underwent surgery. Please note that earlier this year no financial assistance was provided to employees who had already left the company.

Setting up 1C:ZUP 3.1

To make it possible to calculate financial aid in the program, go to the calculation settings wages and activate the option of paying income to former employees of the company:

Menu “Settings”->Payroll

It is worth noting that financial assistance is subject to personal income tax and insurance premiums differently. Therefore, it is necessary to configure the “Types of payments to former employees” directory:

Menu “Payments”->See. See also->Types of payments to former employees

To set up payments to employees of an enterprise dismissed due to the onset of retirement, as well as reimbursement to disabled people for the cost of medications, select the appropriate type of payment predefined in the program.

*Please note that in case of assistance to a previously dismissed but not retired employee, payment of financial assistance will be made with minus personal income tax at the rate of 13%.

Registration of financial assistance payments

The next step will be to register financial assistance. To do this, you need to use the document “Payment to former employees”, designed to record personal income tax amount and/or insurance premiums, and further reflect them in reporting, including regulatory reporting.

Menu “Payments”->Payments to former employees

We create new document. We will give explanations on the introduction of details in the document, which usually raise doubts:

- Month – the exact month of registration of financial assistance in the program is indicated;

- Type of payment – the “Types of Payments...” directory will help you decide on the type of payment. If the selected option provides for additional withholding of taxes or contributions, fields such as Personal Income Tax Code, Insurance premiums, and Deduction will be filled in automatically;

- Payment date – During the document processing, all transactions with personal income tax are recorded by the date specified in this field;

- When adding a former employee to the tabular section, a form will open with a limited selection of employees, which will include only those persons who have already received payments or those who previously worked in the company. If an employee left the company before the start of accounting in the program, he should simply be added to this list. This is done through the selection window:

- Accrued – amount of financial assistance;

- Deduction amount – the amount of income deduction, where personal income tax and insurance premiums are calculated automatically;

- Personal income tax – withholding data is reflected. Here you can also see information on calculating NFDL;

- To be paid – the final figure of financial assistance;

- Contributions – the amount of accrued insurance premiums is reflected.

*We would like to remind you that insurance premiums are subject to payments for labor and civil contracts, providing for the performance of work, as well as the provision of services (Part 1, Article 7 of the Federal Law dated July 24, 2009 No. 212-FZ and Clause 1 of Article 20.1 of the Federal Law dated July 24, 2009 No. 125-FZ).

IN this document A printed form is also provided, it looks like this:

Analysis

The “Non-salary income” report will help you obtain comprehensive information and analyze payments to former employees.

Menu “Payments”->Payment reports

When you enter the amount in 1C ZUP 3.0, the personal income tax deduction for this material assistance is automatically calculated, taking into account other income, within tax period. In our example, the employee needs to withhold 598 when paying financial assistance. rubles personal income tax, respectively, to pay him 9,402 rubles.

In the form of the “Material Assistance” document, it is possible to create an Order for unified form“On payment of financial assistance”:

In 1C ZUP 3.0 you can reflect the calculated moment, that is, indicate when the payment of financial assistance is planned. In our example, the payment is made along with the advance payment, so the date 01/20/2016 was automatically entered. We carry out the document:

Why is it important to indicate the payment date? Because material income is “other” income for personal income tax purposes, not salary. This means that the date of receipt of income is the date of payment.

In 2016, it is very important to keep correct records of the dates of receipt of income, since it is necessary to indicate the date of receipt of income on a quarterly basis. new form reporting 6-NDFL. Therefore, be careful with the payment date.

In 1C ZUP 3.0, the document Material Assistance has already accrued, that is, he accrued everything himself. The line with financial assistance will no longer appear in payroll.

Please rate this article:

In the last article we talked about the calculation of financial assistance in the 1C ZUP 2.5 program, and today we will look at how financial assistance is calculated in 1C 8.2 , namely in 1C Accounting 8 edition 2.0.

Let’s analyze its calculation using the example of financial assistance in connection with an employee’s marriage. We will have the same example: employee of Veda LLC M.V. Kotova. financial assistance was provided in connection with the wedding in the amount of 7,000 rubles.

The amount of financial assistance is usually established by the head of the organization and depends on the case of assistance and financial situation organizations. Also, the procedure for providing financial assistance may be prescribed in the collective agreement.

Material assistance in 1s 8.2 accrued without the decision of the founders of the enterprise on the expenditure of funds will be reflected in account 91 “Other income and expenses”. The amount of financial assistance is not taken into account for corporate income tax purposes.

In addition, the amount of financial assistance exceeding 4,000 rubles will be subject to contributions and personal income tax.

Please note that for personal income tax the period is taken calendar year. This means that if an employee has already received financial assistance in the amount of 4,000 rubles or more during the year, then the next assistance will be subject to personal income tax in full.

To calculate financial assistance in the 1C Accounting program 8, ed. 2 let's create first the new kind accruals. Located on the “Salary” tab.

We indicate the name “Financial assistance in connection with marriage” and add entry Dt 91.02 Kt 70. We indicate that these expenses are not taken into account for tax purposes.

By personal income tax line We indicate code 2760 “Financial assistance provided by employers to their employees, as well as to their former employees who quit due to retirement.” Income under this code in the amount of up to 4,000 rubles is not subject to personal income tax during the calendar year.

In our example, Kotova receives financial assistance for the first time in a year.

In the insurance premiums column, we indicate that financial assistance in 1C 8.2 is partially subject to insurance premiums, that is, only amounts over 4,000 rubles will be taxed.

The accrual of financial assistance in 1C Accounting 8 will be reflected in the document “Accrual of salaries to employees.” This accrual is a one-time charge, so information will be entered into the document manually. We select an employee, indicate the type of accrual and amount. Personal income tax will also be calculated based on the document.