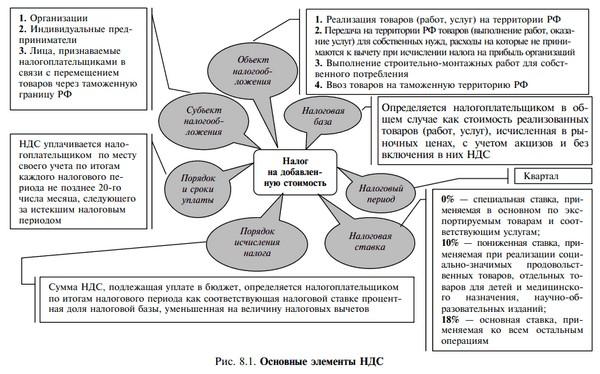

Separate VAT accounting is mandatory for enterprises that combine transactions subject to taxation with benefits. Organizations that combine UTII with the general system should also divide the “input” tax between types of financial and economic activities.

Separate accounting: rules and features

The methodology is applied by the taxpayer when, in the course of his activities, together with transactions subject to tax, he carries out actions for which deductions are not provided.

Principles of maintaining separate records for personal income tax.

| No. p / p | Type of activity | Accounting Rules |

|---|---|---|

| 1 | One type of financial and economic activity. | When purchasing services and products that are fully involved in a taxable process, taxpayers do not have any difficulties with reflecting them in accounting. After all, the buyer accepts the tax calculated by the supplier in full for deduction on the basis of Art. 170 of the Tax Code of the Russian Federation, paragraph 4 and art. 172 clause 1. If the purchased products will be used in activities for which a preferential tax regime is provided, then VAT will be entirely used to increase their value. |

| 2 | Certain types of economic and financial activities. | When purchased goods, fixed assets, intangible assets, services, property rights or various works will be used both in the preferential and taxable process, the division of VAT with separate accounting will be special. Then part of the tax amount calculated by the supplier can be used as a deduction, and the second half can be used to increase the cost of purchased goods. To calculate which part of the VAT will be considered a deduction and which part will be attributed to the increase in the basic cost, you will need to calculate the proportion (Article 170, paragraph 4, paragraph 4)* |

*The taxpayer makes a note in the expense book about the received invoice only in that part that will be used for the required deduction.

When is it necessary to keep separate records for personal income tax?

For transactions subject to taxation, it is necessary to pay VAT to the state treasury (Tax Code of the Russian Federation p. 146). There is no need to allocate VAT on other types of activities that are exempt from tax (Article 149). That is, you need to determine the profit for which the benefit is provided. But at the same time, it is necessary to highlight the “input” VAT attributable to operations of this kind, which is not accepted for deduction.

For tax-exempt activities, the “input” mandatory VAT includes the cost of purchased goods. In the absence of separate accounting, during an inspection by Federal Tax Service inspectors, the “input” mandatory VAT on goods purchased for use in non-taxable and taxable transactions will be restored. As well as general business expenses.

That is, a tax arrears arise, for which tax officials can impose penalties and charge interest. In addition, the company will not be able to include the restored deductions in the costs taken into account when determining the tax on income received (Tax Code of the Russian Federation, Art. 170, clause 4, paragraph 6).

When is hotel accounting not required?

It is not necessary to comply with such a rule when, during the reporting quarter, the amount of costs for the purchase, production and/or sale of products (property rights, various services, works) exempt from taxation does not exceed 5 percent of the total costs for the purchase, production and/or and sale of works (various services, goods and other property rights). Then the “input” tax presented by official suppliers in a given reporting quarter can be accepted as a deduction (NC Art. 170, clause 4, paragraph 7).

It is not necessary to comply with such a rule when, during the reporting quarter, the amount of costs for the purchase, production and/or sale of products (property rights, various services, works) exempt from taxation does not exceed 5 percent of the total costs for the purchase, production and/or and sale of works (various services, goods and other property rights). Then the “input” tax presented by official suppliers in a given reporting quarter can be accepted as a deduction (NC Art. 170, clause 4, paragraph 7).

Worth taking note! The procedure for calculating total costs for tax purposes is not provided for by the legislation of the Russian Federation, so an enterprise can calculate total costs based on accounting information.

For example, take into account all expenses (indirect, direct, general business, general production and others) associated with the implementation of tax-exempt activities.

Methodology for determining VAT

There are no specific methods for carrying out separate accounting (Tax Code of the Russian Federation, Chapter 21). Therefore, a different procedure may be used to make it possible to separate preferential transactions from the main activities subject to taxation.

VAT-exempt and taxable transactions should be conducted in various sub-accounts opened with the main accounting accounts. The preferred procedure for calculating the tax payable must be enshrined in the accounting policies of the enterprise.

If an organization actually applies a special method for calculating tax, but this is not reflected in its accounting policies, then it is possible to fully challenge the possible refusal of the authorized bodies to provide a deduction in the courts. In this case, you need to provide the necessary evidence that such a distinction for VAT takes place.

It is worth noting! But there are also cases of negative judicial practice for taxpayers who failed to prove that separate calculations are being carried out.

Rule "5%": features

If there are both export activities not subject to VAT tax and other transactions subject to this type of tax, separate VAT calculations must be carried out.

The main goal is to separate the “input” compulsory tax so that it can be legally deducted.

Exporters are also required to conduct a separate calculation of the DS tax for activities for which the benefit is provided. But do they have the right to use the 5 percent threshold when calculating the cost sharing ratio, both for sales and for other transactions outside the Russian Federation? Officials answer this unequivocally, no.

Simple examples of separate tax accounting

The calculation of all indicators should be reflected in the accounting certificate. How to determine the amount of tax deductible on total financial and economic costs.

Example

The main activity of Strela LLC is retail sales of goods. In addition, the company sometimes sells products to “wholesalers.” For the sale of goods at retail, the company pays UTII; for wholesale supplies, it uses the basic tax regime.

- In the second quarter, income from the sale of products at retail amounted to 12,000,000 rubles, wholesale - 3,540,000 (including tax - 540,000 rubles).

- Every month, the company pays rent and utilities 177,000 rubles, plus personal income tax - 27,000 rubles.

- At the end of June, the chief accountant determined the share of revenue received from the sale of products subject to taxation: 3,000,000 rubles (12,000,000 plus 3,000,000) * 100% = 20%.

- The calculated amount of tax on DS and expenses aimed at paying mandatory utility bills, which is deducted every month, is equal to the following amount: 27 thousand rubles x 20% = 5,400 rubles.

The amount of the main payment, which can legally be attributed to expenses, was: 27 thousand rubles – 5,400 rubles = 21,600 rubles.

That is, this amount is not subject to taxation, therefore, according to the legislation of the Russian Federation, the enterprise is not subject to payment.

A little in custody

The obligation to carry out a separate calculation required by all VAT suppliers arises when the taxpayer carries out both non-taxable and taxable economic and financial activities. The principles, conditions for the implementation of such accounting are reflected in the Tax Code of the Russian Federation, Art. 170 clauses 4.1 and 4.

If a company buys various materials, services or goods, which will then be used for both types of commercial activities, then, first of all, it is worth calculating the proportion on the basis of which the “input” VAT will be distributed. But at the same time, part of the tax will be used in the form of a deduction when accounting for certain transactions subject to taxation, and the rest will go to increase the value of existing assets that were involved in conducting activities that are not subject to VAT.

In contact with

In contact with