E.A. Sharonova, economist

We are developing a convenient personal income tax register

The development of a tax register for personal income tax is left to the organization itself clause 1 art. 230 Tax Code of the Russian Federation. As a rule, all tax registers are available in accounting programs. But there are organizations that do not have the opportunity to buy these programs. If you are one of them, then this article is for you.

Where to begin

Before you make a personal income tax register for yourself, you need to determine what it is needed for. And you need it as a tax agent in order to:

- correctly calculate the tax to be withheld from the employee’s income;

- Based on register data, quickly fill out 2-NDFL certificates for each employee and at the end of the year report to the tax inspectorate clause 2 art. 230 Tax Code of the Russian Federation;

- when tax audit present the register to the inspectors and avoid a fine for its absence.

Therefore, the register must contain required details, directly mentioned in the Tax Code, as well as all the data that is in the 2-NDFL certificate. After all, it will be easier to fill it out.

Mandatory personal income tax register details

Mandatory details that must be in the personal income tax register include: clause 1 art. 230 Tax Code of the Russian Federation:

1) information allowing to identify the taxpayer (full name, tax identification number). It is also better to immediately indicate passport data (number, series, address of residence) in the register, since they are needed to fill out the 2-NDFL certificate;

2) taxpayer status (resident/non-resident);

3) types of paid income and their codes;

4) types of tax deductions provided and their codes;

5) the amount of income and the amount of deductions;

6) dates of payment of income;

7) tax withholding dates;

8) dates of tax transfer;

9) details of the payment document for the transfer of tax to the budget (date and number).

Reader's opinion

“How does personal income tax work here? The inspector does nothing and is happy. The employee sleeps peacefully (especially on the 5th and 20th). And the employer calculates, withholds, transfers, provides, reports, issues, represents. Moreover, for each recipient and for each payment! And all by myself! It’s good that I haven’t fined myself yet.”

Alexander,

chief accountant, Moscow

The first five details do not raise any questions, and there are no problems reflecting them in the tax register. All information about the employee can be prepared in the same way as in section 2 of the 2-NDFL certificate.

It is clear that you will take the amount of employee income from your own primary documents(settlement and payment statements, pay slips, acts, etc.). Income codes and deduction codes are taken from the Directories given in Appendices No. 3 and No. 4 to the Order of the Federal Tax Service, which approved the form of the 2-NDFL certificate and Recommendations for filling it out approved By Order of the Federal Tax Service dated November 17, 2010 No. ММВ-7-3/611@.

And the taxpayer status can be coded like this section II Recommendations, approved. By Order of the Federal Tax Service dated November 17, 2010 No. ММВ-7-3/611@ (hereinafter referred to as the Recommendations): number 1 means that the resident employee and his labor income are taxed at a rate of 13% clause 2 art. 207, paragraph 1, art. 224 Tax Code of the Russian Federation, and number 2 - that a non-resident and his income are taxed at a rate of 30% clause 2 art. 207, paragraph 3 of Art. 224 Tax Code of the Russian Federation.

If the employee is a foreigner or simply often goes abroad on business trips, then in order to record how his status changes during the year, you can make such a table at the beginning of the register.

It is also necessary to monitor the status throughout the year because deductions are provided to the employee only for income taxed at a rate of 13% pp. 3, 4 tbsp. 210 Tax Code of the Russian Federation. But let's look at the last four register details in more detail.

Income payment date

In ch. 23 of the Tax Code of the Russian Federation there is no such thing as “date of payment of income”. Therefore, we must proceed from the literal meaning of this term. In the personal income tax register, the date of actual payment of money to the employee must be indicated as the date of payment of any income. By the way, the Ministry of Finance also thinks so. For example, he explained that if salaries are paid by crediting money to employees’ card accounts, then the register must indicate exactly the date of transfer of money to the employee’s cards in Letter of the Ministry of Finance dated February 14, 2012 No. 03-04-06/6-37.

| Type of income | Income payment date clause 1 art. 223 Tax Code of the Russian Federation |

| Any income in cash (including wages, GPA payments, vacation pay, sick leave, dividends, etc.) | The day of payment of income from the cash register or transfer of money to the employee’s bank account |

| Revenues in in kind | The day of transfer of property to the employee (provision of services to him, performance of work for him) |

| Material benefit received from saving on interest when issuing a loan to an employee | The day the employee pays interest on the loan |

| Material benefit received from the acquisition of goods (work, services) or securities | The day an employee purchases goods (works, services), securities |

Since salaries must be paid twice a month (for the first half of the month - before the end of the month, usually from the 16th to the 30th, for the second half - after the end of the month, usually from the 1st to the 15th number Art. 136 Labor Code of the Russian Federation), then you will need to indicate two payment dates in the register.

Personal income tax withholding date

The organization is obliged to withhold personal income tax from the employee’s income when paying them. clause 4 art. 226 Tax Code of the Russian Federation. After which the withheld tax must be transferred to the budget, and income minus personal income tax must be transferred to the employee.

The tax subject to withholding must be calculated earlier - at the time of accrual of income to the employee. That is, on the day of accrual of salaries, bonuses, allowances, additional payments, sickness benefits, vacation pay, GPA income, etc. This will be the calculated tax, and you indicate it in the appropriate column of the personal income tax register.

But, as we have already said, it is necessary to withhold the calculated personal income tax from the employee’s income only when they are directly paid.

WE WARN THE EMPLOYEE

If job changes during the year, In order to receive children's deductions in a new place, you need to bring a 2-NDFL certificate from the previous one to the accounting department places of work. Otherwise, deductions simply will not be given.

In most cases, the tax withholding date will coincide with the date of payment of income (for example, when paying vacation pay, sick leave, Resolution of the Presidium of the Supreme Arbitration Court of 02/07/2012 No. 11709/11; Letters of the Ministry of Finance dated 06.06.2012 No. 03-04-08/8-139, dated 10.10.2007 No. 03-04-06-01/349). But there are two exceptions to this rule - payment of non-monetary income and income in the form of wages.

When paying income in kind (for example, when issuing gifts), it is impossible to withhold personal income tax at the time of payment of income. This must be done the next time money is paid to the employee, for example, when paying him a salary, vacation pay, sick pay, etc. clause 4 art. 226 Tax Code of the Russian Federation; Letter of the Ministry of Finance dated November 28, 2007 No. 03-04-06-01/420

Now let's look at the salary. It, as we have already said, is paid twice a month. So what, withhold personal income tax twice? The regulatory authorities have repeatedly explained what to calculate, withhold and transfer to personal income tax budget from salary (including for the first half of the month) is necessary once a month when making the final calculation of the employee’s income based on the results of each month for which he was accrued income Letters of the Ministry of Finance dated 08/15/2012 No. 03-04-06/8-143, dated 08/09/2012 No. 03-04-06/8-232, dated 07/17/2008 No. 03-04-06-01/214, dated 07/16. 2008 No. 03-04-06-01/209, Federal Tax Service for Moscow dated April 29, 2008 No. 21-11/041841@.

Thus, the date of receipt of income in the form of wages for both the first and second half of the month is the last day of the month for which the wages were accrued. And on the same date you need to calculate personal income tax for the month clause 2 art. 223 Tax Code of the Russian Federation. But you need to withhold tax on the date of payment of income - on the day you receive money from the bank for the payment of wages for the second half of the month (when issued from the cash register) or transfer to employee cards in clause 4 art. 226 Tax Code of the Russian Federation.

It would seem that everything is simple: when paying wages for the first half of the month (advance), there is no need to withhold personal income tax. However, if you pay the employee an advance amount without withholding personal income tax, then at the end of the month a situation may arise when you will not be able to transfer personal income tax to the budget, since you will have nothing to withhold tax from. For example, you paid an advance to an employee, but personal income tax was not withheld from him. And then it turned out that for the second half of the month the employee was not entitled to a salary for some reason (for example, he got sick or was on vacation at his own expense). And it turns out that you simply have nothing to withhold personal income tax from. And transfer personal income tax to the budget at the expense of own funds you cannot, it is expressly prohibited by the Code clause 9 art. 226 Tax Code of the Russian Federation. There are three options to solve this problem:

- <или>pay wages for the first half of the month minus the personal income tax calculated from it, but do not accrue personal income tax (do not post Dt account 70 - Kt account 68) and do not withhold. Then at the end of the month you can always withhold the entire personal income tax for the month from the employee’s income;

- <или>calculate (post Dt account 70 - Kt account 68) and withhold personal income tax from the advance, but do not immediately transfer it to the budget. And transfer the amount of tax withheld from the entire salary for the month once - when paying salaries at the end of the month. However, this option may raise unnecessary questions from tax authorities when on-site inspection(they say, since they withheld the tax, why didn’t they transfer it, there was an opportunity);

- <или>calculate, withhold and transfer personal income tax with each salary payment, that is, twice a month (make entries: when calculating personal income tax - Dt account 70 - Kt account 68, and when transferring tax - Dt account 68 - Kt account 51).

Date of personal income tax transfer and payment details

This is the date indicated in the bank’s mark on the payment slip for the transfer of personal income tax. Let us remind you that the period within which the tax must be transferred to the budget depends on the method of payment of income in clause 6 art. 226 Tax Code of the Russian Federation.

If you pay income (except for wages for the first half of the month) to an employee by bank transfer and transfer the tax on time, then the date of payment of income, the date of tax withholding and the date of its transfer will coincide.

Everyone knows that personal income tax is transferred to the budget immediately for all employees of the organization (or employees of one department) in one payment. Therefore, if the withheld personal income tax is transferred to the budget in full, then in the tax register each employee will have the same payment slip number and its date.

General rules for maintaining a register

RULE 1. A separate register must be created annually for each employee. Art. 216, paragraph 1, art. 230 Tax Code of the Russian Federation. It must reflect all income paid to the employee, regardless of the rate at which they are taxed. Taxable according to different rates(9, 13, 15, 30 or 35%) income must be reflected separately, for example in different sections of the register pp. 1, 3 tbsp. 226, Art. 224, paragraph 1, art. 230 Tax Code of the Russian Federation. By the way, this is exactly the principle that applies when filling out 2-NDFL certificates (for each rate - separate sections 3-5) section II Recommendations.

RULE 2. In the register, all income paid to the employee, taxed at a rate of 13%, and deductions provided are reflected both monthly and on an accrual basis from the beginning of the year. After all, personal income tax on these incomes is calculated on an accrual basis from the beginning of the year based on the results of each month, minus personal income tax withheld in previous months current year A clause 3 art. 226 Tax Code of the Russian Federation.

But income taxed at other rates can only be reflected monthly. In this case, personal income tax is calculated separately for each amount of income without providing a deduction for pp. 3, 4 tbsp. 210, paragraph 3 of Art. 226 Tax Code of the Russian Federation.

RULE 3. If the employee was hired not from the beginning of the year, then the following information can be indicated at the beginning of the register.

The amount of income is taken from the 2-NDFL certificate from the previous place of work. clause 3 art. 218 Tax Code of the Russian Federation. This information is needed to decide whether to give the employee deductions for children or not. After all, if income from the beginning of the year exceeds 280,000 rubles, then deductions are no longer provided subp. 4 paragraphs 1 art. 218 Tax Code of the Russian Federation.

If the employee has the right to child deductions, then it is better to make another sign at the beginning of the register.

It will immediately be clear from which month you should start providing deductions and when to stop doing so, what deduction amount to provide and what deduction code to assign.

Attention

Deductions for children are provided to an employee for each month of the calendar year, regardless of whether in these months there was income taxed at a rate of 13% or not. subp. 4 paragraphs 1 art. 218, paragraph 3 of Art. 210, paragraph 3 of Art. 226, Art. 216 Tax Code of the Russian Federation; Letter of the Ministry of Finance dated January 19, 2012 No. 03-04-05/8-36; Resolution of the Presidium of the Supreme Arbitration Court of July 14, 2009 No. 4431/09.

RULE 4. The register may not reflect income that is not fully subject to personal income tax, for example, maternity benefits, monthly allowance child care up to one and a half years old Art. 217 Tax Code of the Russian Federation.

But income that is not subject to personal income tax within the limits established limit(for example, daily allowance over 700 rubles, material aid and gifts taxable in excess of 4,000 rubles. per year, etc.), in the register reflect above pp. 3, 28 art. 217 Tax Code of the Russian Federation; Letter of the Ministry of Finance dated July 20, 2010 No. 03-04-06/6-155. Moreover, income must be reflected in the register in full, and non-taxable amount indicate deduction code a Letter of the Ministry of Finance dated March 2, 2012 No. 03-04-06/9-54.

RULE 5. If an organization has separate divisions, then tax registers for personal income tax must be maintained in each OP separately.

And if an employee simultaneously receives income from both the GP and the OP, then two personal income tax registers must be opened for him. In this case, for the correct calculation of personal income tax, it is more convenient to provide deductions for children in one place - either in the GP or in the OP.

It is necessary to maintain registers in each OP so that there are no problems with the transfer of personal income tax and the submission of 2-personal income tax certificates. After all, personal income tax withheld from the income of employees of OPs must be transferred to the budget exactly at the location of each OP clause 7 art. 226 Tax Code of the Russian Federation. And as the Ministry of Finance and the Federal Tax Service have repeatedly explained, 2-NDFL certificates must be submitted to where the personal income tax is transferred Letters of the Federal Tax Service dated May 30, 2012 No. ED-4-3/8816@; Ministry of Finance dated 08/07/2012 No. 03-04-06/3-222, dated 03/23/2012 No. 03-04-08/8-58. That is, 2-NDFL certificates on the income of SE employees must be submitted to the Federal Tax Service at the location of the SE, and 2-NDFL certificates on the income of SE employees - to the Federal Tax Service at the location of the SE section II Recommendations.

RULE 6. Personal income tax amounts are reflected in the register in whole rubles, and all other amounts are in rubles and kopecks x clause 4 art. 225 Tax Code of the Russian Federation.

RULE 7. It is better to approve the personal income tax register form by order of the manager.

Filling out the personal income tax register

We'll show you how to do this with an example.

Example. Filling out the personal income tax register

/ condition / Cheerful Ivan Petrovich works in the organization. His salary is 20,000 rubles. Deadlines for payment of wages: for the first half of the month - the 22nd day of the current month, for the second half of the month - the 7th day of the next month.

The employee has a daughter aged 10 years. In this regard, he brought to the accounting department an application for a deduction and a copy of the child’s birth certificate.

From February 4 to February 8, the employee was sick. After Cheerful I.P. brought sick leave, he was awarded an allowance in the amount of 4,000 rubles, which was paid on the 22nd along with his salary for the first half of February clause 1 art. 15 of the Law of December 29, 2006 No. 255-FZ.

From March 11 to March 24, the employee was on vacation. The amount of vacation pay was paid to the employee on March 5 before the start of the vacation along with the salary for February Art. 136 Labor Code of the Russian Federation.

In addition, Cheerful I.P. The organization presented two gifts:

- January 25, in connection with his anniversary - in the amount of 3,000 rubles;

- On February 22, in connection with the holiday - in the amount of 1,500 rubles.

Personal income tax withheld from employees' salaries was transferred to the budget on the day the money was received from the bank to pay salaries.

/ solution / In the register we provide only the data that is needed to calculate the tax.

Tax register for personal income tax

07.02.2013

07.03.2013

| 1. The amount of personal income tax, excessively withheld at the end of the year (column 9 – column 8) | |

| 2. The amount of personal income tax not withheld at the end of the year (column 8 – column 9) |

ATTENTION: similar article on 1C ZUP 2.5 -

Hello dear site visitors. Today in the next article we will talk about how in the program 1C 8.3 ZUP 3.1 The process of accounting for various types of personal income tax has been organized:

- Calculated personal income tax

- Withheld personal income tax

- Listed personal income tax

We will take a detailed look at what documents the data is taken into account types of personal income tax and in what registers they are reflected. Let's look at specific example how to register in the program employee's right to receive a standard tax deduction and how it will be taken into account when calculating personal income tax. Let's consider some other settings that must be taken into account for the correct calculation of personal income tax in the 1C ZUP program, edition 3.

✅

✅

First we'll talk about calculated personal income tax. In the ZUP 3.0 (3.1) program, this personal income tax is calculated in the documents “Accrual of salaries and contributions”, as well as in various inter-account documents, such as “Vacation”, “Business trip”, “Sick leave”, “Bonuses”, “One-time accruals” and in some others. First, let's talk about how it is calculated Personal income tax in interpayment documents. I will analyze today’s material on the basis of the information base that we have formed as a result of previous publications, where I talked about and.

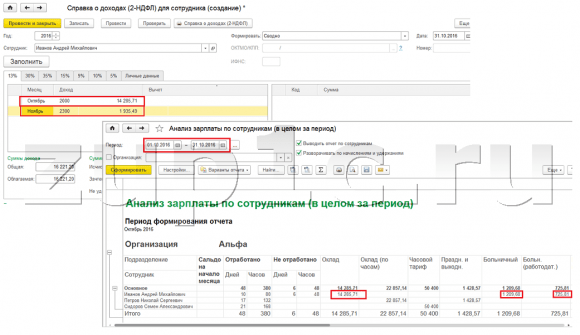

Let's look at the inter-account document “Sick leave” for employee A.M. Ivanov. for October. This document is a personnel accounting document and when filled out, the program automatically determines average earnings employee for two calendar years preceding the year of onset of temporary disability. Here, sick leave is completely calculated based on average earnings, and calculated by personal income tax. You can view the details of the calculation of this tax by clicking on the button with the image of a green pencil.

In the window that opens “More details about personal income tax calculation” we will see the amount of calculated tax, date of receipt of income, for which it is calculated, possible standard and property deductions, if they are registered for the employee. In our example, Ivanov A.M. on this moment no deductions for personal income tax. Personal income tax was calculated correctly - 252 rubles, which is 13% of the amount of income of 1,935.49 rubles.

I would like to draw Special attention for props "payment date" in the document “Sick leave”. The fact is that it is very important to correctly indicate this date in interpayment documents. For incomes for which the income code is NOT equal to code 2000 or 2530 (and for hospital income code 2300), it is according to "payment date" determined "date of receipt of income", and this date determines which month of the tax period the income and the personal income tax calculated from it will be attributed to.

In the document “Sick leave” the date of payment is indicated 05.11 (payment with salary) and based on it was automatically filled in date of receipt of income Also 05.11 , which is what we actually see in the “More details about personal income tax calculation” window. Accordingly, we will have the month of the tax period for personal income tax accounting purposes November. Where can we see this period? For example, if according to employee Ivanov A.M. generate a “Certificate of Income (2-NDFL)”, it will be seen that income with code 2300 (and these are sick leave, in the amount of 1,935.49 rubles for our example) fell in the month of the tax period November. The same thing will happen in the regulated report “2-NDFL for transfer to the Federal Tax Service” if we generate it.

It should also be said that the date of receipt of income, which will be determined for the calculated personal income tax in the interpayment document, directly affects the filling quarterly report 6-NDFL. I discuss the issue of filling out 6-NDFL in 1C ZUP 3.0 (3.1) in great detail in the article

So this sick leave in tax accounting was registered in November. We are convinced of this. But it is worth noting that the accrual month in the “Sick Leave” document is indicated as October. This means that if we generate salary reports in the program from the Salary (Salary Reports) section, such as “Payslip”, “Full set of accruals, deductions and payments” or “Salary analysis for employees (as a whole for the period)” , then in them this sick leave will be attributed to the month October. Let's look at the example of Salary Analysis for Employees, indicate the period from 01.10 to 31.10 and see that sick leave is included in the report.

Those. there is a difference between what month of the tax period this income is registered (NOVEMBER), and to which month of accrual, he is assigned (OCTOBER). It is worth understanding this difference and keeping in mind that this situation is normal.

Registration of calculated personal income tax with the document “Accrual of salaries and contributions” in 1C ZUP 3.1 (3.0)

Now let's look at the document "Calculation of salaries and contributions" for October. Here, personal income tax is also calculated (the “personal income tax” tab), and the screen below shows that in this example, personal income tax is calculated exactly from the employee income that is accrued in this document. But in fact, the program analyzes all employee income from the beginning of the year, i.e. Personal income tax is calculated on an accrual basis from the beginning of the year. If the program sees that for some reason the tax was not calculated in interpayment documents or in previous months, but should have been, then this personal income tax will be calculated here, i.e. The program will not lose any income.

To illustrate this point, let’s remove the personal income tax in the Sick Leave document and assume that for some reason it was not calculated. Let's spend sick leave in this form.

Now, let’s recalculate personal income tax in the document “Calculation of salaries and contributions.”

Please note that according to employee Ivanov A.M. in the document “Calculation of salaries and contributions” on the personal income tax tab, we now have two lines formed. In the first line, 1857 rubles. - this is the calculated tax on salary payment in the amount of 14,285.71 rubles. Second line, 252 rubles, tax calculated from sick leave and we can determine this by the date of receipt of income 05.11, which corresponds to the date of payment in the “Sick Leave” document.

Thus, the date of receipt of income will be the last day of the month for which it was accrued, i.e. 31.10.

The same goes for other employees. Sidorov S.A. in October, payment was accrued at an hourly rate and a percentage bonus; these types of accrual also have an income code of 2000, respectively, the date of receipt of income is the last day of the month - 10/31.

Employee Petrov N.S. in October, payment was accrued based on salary (by the hour) and payment for work on holidays and weekends, these types of accrual also have an income code of 2000, respectively, the date of receipt of income is the last day of the month - 10/31

Thus, the date of receipt of income is determined in accordance with the income code specified in the accrual type settings. For income with code 2000.2530 “date of receipt of income” is defined as the last day of the month, for which income is accrued, and for other income - by date of payment of income.

For clarity, we will also create a “Vacation” document for employee S.A. Smirnov. If we look at the details of the calculation of this personal income tax, we will see that the “date of receipt of income” was also determined by the “date of payment” specified in the document - 07.11

Therefore, I would like to draw your attention once again to the fact that very important correctly indicate the date of payment of income in interpayment documents. In the document “Accrual of salaries and contributions”, the date of payment does not need to be indicated, since the program automatically determines the date of receipt of income based on the month for which income is accrued and sets the last day of this month.

Let's look again at the “Certificate of Income (2NDFL)” for employee A.M. Ivanov. Here we see that income code 2000 (salary payment) in the amount of 1,4285.71 rubles is assigned to the month of the tax period October, and income code 2300 (Sick leave) in the amount of 1,935.49 rubles - November. But in the salary report “Analysis of salaries by employees” for the period from 01.10 to 31.10, both Salary and Sick Leave are indicated.

I would also like to talk about the technical side of this issue, i.e. tell us in which registers in the 1C ZUP 3.0 (3.1) program it is taken into account counted Personal income tax (by the way, I have already discussed this issue in some detail in the article). So, in order for us to view these registers, it is enough to open the document “Accrual of salaries and contributions”, i.e. the document in which this personal income tax was calculated and directly into the form of this document display all those registers on which this document can make movements. To do this, open the Main menu – View – Setting up the form navigation panel. In the “Available commands” field, select the register we need, it is called “”, and it is taken into account counted Personal income tax, click the “Add” button and this register will go to the “Selected commands” field. Click OK.

A link will appear at the top of the “Payroll and Contributions” document “Calculations of taxpayers with the budget for personal income tax”, when opened, you can view the movement of this document according to this register. In the register Calculations of taxpayers with the budget for personal income tax 4 entries occurred, exactly those that are present on the personal income tax tab in the “Calculation of salaries and contributions” document.

I want to draw your attention to the fact that this movement is done with a plus sign, that is incoming movement, and means that this counted Personal income tax. An expense movement with a minus sign in this register is withheld personal income tax. We'll talk about it further.

Registration of withheld personal income tax with the documents “Vedomost...” in 1C ZUP 3.1 (3.0)

✅

✅ CHECKLIST for checking payroll calculations in 1C ZUP 3.1

VIDEO - monthly self-check accounting:

✅ Payroll calculation in 1C ZUP 3.1

Step-by-step instruction for beginners:

Firstly, it is worth noting that in the 1C ZUP 3.1 (3.0) program registration withheld personal income tax carried out in the documents “Vedomost...”:

- "Statement to the bank"

- “Statement of transfers to accounts”,

- "Statement to the cash register"

- “Payment sheet through the distributor.”

For our example, we will create the document “Statement to the Bank”. The program will automatically fill out the document with those employees whose payment method is assigned in the organization’s settings, i.e. by crediting to the card within salary project(in our example this is employee A.M. Ivanov and N.S. Petrov). You can read more about paying advances and salaries in 1C ZUP in the article.

When filling out this document, the program analyzes not only the balance of debt to the employee (the “Payable” column) and not only indicates the amount to be paid, but also fills out the “Personal Income Tax to be Transferred” column, i.e. the tax that will be withheld when processing the document. When filling out this column, the program analyzes the remainder by register “Calculations of taxpayers with the budget for personal income tax”, is there in this register counted, but also unrestrained tax. Therefore, if for some reason personal income tax for the previous months was not reflected as withheld, then the program will take it into account the next time you fill out the “Vedomost...” document.

Now let’s look in more detail at what it was made up of by employee A.M. Ivanov. To do this, double-click on the amount of 2,109 in the “Personal Income Tax to be transferred” column. The “Editing Employee Personal Income Tax” window will open, where we see personal income tax in the amount of 1,857 rubles. from income from salary (date of receipt of income 10/31) based on the document “Accrual of salaries and contributions” and personal income tax in the amount of 252 rubles from sick leave (date of receipt of income 05/11) based on the document “Sick Leave”.

Next, let’s see what movements the document “Statement to the Bank” will make according to the register. For ease of viewing, we will display a link to this register directly in the document form. In exactly the same way as we did in the document “Calculation of salaries and contributions” (Main menu - View – Setting up the form navigation panel). So let's follow the link “Calculations of taxpayers with the budget for personal income tax.” Now we see that, unlike the document “Calculation of salaries and contributions” (receipt movement with a plus sign), the document “Statement to the bank” does consumable movement with a minus sign. It is the expense movement in this register that reflects the fact withholding personal income tax.

Here it is immediately worth noting that it is precisely according to the expense movements of this register that section 2 in the report “6 Personal Income Tax” is formed (more details in the article). And in this regard very important so that the retention period (date) is indicated correctly. In fact, this is line 110 in section 2 of the “6 personal income tax” report. The retention date (period) in the register is filled in automatically in accordance with the date specified in the “Statement...” document. Therefore, once again I draw your attention, very important To correctly fill out section 2 of report 6 of personal income tax, correctly indicate the date in the document “Statement...”, i.e. exactly the date when wages are actually paid and personal income tax is withheld accordingly.

Registration of the listed personal income tax with the documents “Vedomost...” in 1C ZUP 3.1 (3.0)

✅ Seminar “Lifehacks for 1C ZUP 3.1”

Analysis of 15 life hacks for accounting in 1C ZUP 3.1:

✅ CHECKLIST for checking payroll calculations in 1C ZUP 3.1

VIDEO - monthly self-check of accounting:

✅ Payroll calculation in 1C ZUP 3.1

Step-by-step instructions for beginners:

In the 1C program ZUP 3.1 (3.0) personal income tax listed, as well as withheld, are registered by default in the “Vedomost...” documents. Let's look at the listed tax using the example of the document “Statement to the Bank”. If we follow the link Payment of salaries and transfer of personal income tax, which is located at the bottom of the document, then some more details of this document will open. By default, this checkbox is checked Tax is transferred with salary and that is why the document “Gazette …” registers the fact of personal income tax transfer. In the payment document field, we can immediately indicate the number and date of the payment document by which the personal income tax was transferred.

Now let's talk about registers. Listed personal income tax reflected in the register. Let's display a link to the register Calculations tax agents with a personal income tax budget to the form of the document Statement to the Bank (Main menu – View – Setting up the form navigation panel) and see its contents. In this register income movement with plus now registers fact retention Personal income tax, and with a minus - consumable movement registers listed tax.

Now let's talk about alternative way registration of the fact of personal income tax transfer to the budget. If we do not want to reflect the fact of personal income tax transfer in the “Vedomosti...” document itself, then the program contains a document « Transfer of personal income tax to the budget". But why might we not want this?

In this situation, if we reflect the enumeration personal income tax document“Sheet ...”, then in fact in the program this transfer is registered on the date that appears in the Sheet itself, i.e. in our example, the fact of transfer was registered on the date 05.11. If we actually transferred this personal income tax the next day, i.e. 6.11 (we have the right to transfer personal income tax no later than the next day after payment wages, and personal income tax on sick leave and vacation pay no later than the end of the month), and not 5.11, then it turns out that we store not entirely reliable information in the program. Therefore, for more correct accounting, this listing should be reflected in 6.11.

But, nevertheless, I will show how to reflect the transfer of tax in a document “Transfer of personal income tax to the budget”.

Let’s uncheck the checkbox in the “Statement to the Bank” document “The tax is transferred along with the salary” and we will make a statement. Let's follow the link Calculation of tax agents with the personal income tax budget and we will see that now the document only does income movement with a plus sign, i.e. registers only held Personal income tax, but the one listed was not recorded.

Next, please note that a new link has appeared in the document “Statement to the Bank” Enter personal income tax transfer data. Let's use it, and the program will transfer us to the document log Transfer of personal income tax to the budget. Let's create new document. We will transfer the tax on 06.11. In the Amount field, we will enter the amount of tax that is indicated in the document Statement to the bank in the column “Personal income tax to be transferred” in the amount of 5,266 rubles, i.e. We will remit any tax withheld on this statement. Click the spend button.

The program begins to analyze the register Calculations of taxpayers with the budget for personal income tax in the document “Statement to the Bank”. She sees that there is an incoming movement of the withheld tax, but there is no outgoing movement transferred tax. That is, there is a remainder in this register. The amount of 5,266 rubles is distributed in proportions between all these balances (by Employee and Date of receipt of income) and is formed consumable movement, i.e. fact of personal income tax transfer. Accordingly, we list what is withheld. You can compare. Let's open the register Calculations of taxpayers with the budget for personal income tax in the document “Statement to the Bank” and in the document “Transfer of personal income tax to the budget”. That's right, all the tax has now been transferred to us.

So, we've run out of lengthy questions. We have sorted out which documents are in the program 1C ZUP 3.0 (3.1) registered calculated, withheld and transferred tax, as well as in which registers these taxes are recorded. Now we will talk about tax deductions for personal income tax. We considered the examples given above without taking into account tax deductions.

Registration of an employee’s right to provide a standard tax deduction in the 1C ZUP 3.1 (3.0) program

The tax base is determined as the amount of income minus the amount of tax deductions provided. There are five types of tax deductions:

- Standard

- Property

- Professional

- Social

- For partially taxable income

In today's article we will talk about how to register an employee's right to provide a standard deduction in the program. Let’s go to the “Taxes and Contributions” section in the “Application for Deductions” journal. Let's open it, here we can create documents such as an application for deductions for personal income tax, Cancellation of standard personal income tax deductions, Notification of the DO about the right to deductions. Let's create a document “Application for personal income tax deductions”. The deduction is provided to employee Petrov N.S., we indicate the date of the document - 01.11, the month from which this deduction will be applied November. Click the “Add” button and from the list of types of personal income tax deductions proposed by the program, select deduction with code 114 (for the first child under the age of 18, for a full-time student, graduate student, resident, student, cadet, under the age of 24). We indicate the month until which the deduction is provided - December. We carry out the document.

Also in the program, we can view information about the deductions provided directly in the employee’s card (section Personnel - Employees directory). Let’s open N.S. Petrov’s card. and follow the link "Income tax". A window will open where we will see the deduction provided to this employee, which we just entered in the document "Application for deductions." If we need to change something in the application, we can follow the link “Correct the application for standard deductions» directly from the employee’s card.

Now let's go to the link Income from previous place of work, In the tabular section, you should indicate the employee’s income from his previous place of work, if he has been working in our organization for more than a year and worked somewhere else this year. This information is necessary for the program to track excess income for the year for the purposes of accounting for deductions, i.e. stopped providing the deduction in a timely manner if the income was exceeded.

Also in this window there is a field where the taxpayer status is indicated. I did not mention this right away in order to present material about where and how to register different kinds personal income tax and proceeded from the fact that all our employees have taxpayer status - Resident(13%, personal income tax is considered a cumulative total). However, the program supports personal income tax accounting for employees with other taxpayer statuses, such as non-residents, highly qualified foreign specialists and others. And this status is selected for the employee here. Depending on the selected status, the tax rate and the algorithm for calculating personal income tax are determined. But this is a topic for other publications.

So, all necessary information into the program for providing a tax deduction to employee N.S. Petrov. we have contributed, and now we just have to see how it will be taken into account when calculating personal income tax. We will generate a document “Calculation of salaries and contributions” for November. The employee is paid a salary of 30,000 rubles; on the personal income tax tab we see the calculated tax in the amount of 3,718 rubles, taking into account the applied deduction of 1,400 rubles. The calculation will be as follows: (30,000 - 1,400)*0.13 = 3,718 rubles.

In today's article we reviewed quite a lot of material. We talked about where and how to register calculated, withheld and transferred personal income tax. We sorted out which ones tax deductions are provided to employees. Using a specific example, we registered an employee’s right to provide a standard tax deduction.

In the next article I will talk in detail about how contributions are taken into account in 1C ZUP 3.0 (3.1). Follow the publications. All the best!)

In this article I want to consider aspects of the calculation and withholding of personal income tax in 1C 8.3, as well as the preparation of reports in forms 2-NDFL and 6-NDFL.

Setting up registration with the tax authority

This is the most important setting; without it, you will not be able to submit reports to regulatory authorities. Let's go to the "Organizations" directory (menu "Main" - "Organizations"). Having selected the desired organization, click the “More...” button. From the drop-down list, select “Registration with tax authorities”:

You must carefully fill out all the details.

Setting up payroll accounting

These settings are made in the “Salary and Personnel” section – “Salary Settings”.

Let’s go to “General Settings” and indicate that accounting is maintained in our program, and not in an external one, otherwise all sections related to personnel and salary accounting will not be available:

On the “Personal Income Tax” tab, you need to indicate in what order standard deductions are applied:

On the “ ” tab, you need to indicate at what rate insurance premiums are calculated:

Any accruals to individuals are made according to the income code. For this purpose, the program has a reference book “Types of personal income tax" To view and, if necessary, adjust the reference book, you need to return to the “Salary Settings” window. Let’s expand the “Classifiers” section and click on the “NDFL” link:

The personal income tax calculation parameters settings window will open. The reference book is located on the corresponding tab:

To set up personal income tax taxation for each type of accrual and deduction, you need to expand the “Salary calculation” section in the “Salary settings” window:

In most cases, these settings are enough to start accounting for salaries and personal income tax. I will only note that the directories can be updated when the program configuration is updated, depending on changes in legislation.

Personal income tax accounting in 1C: accrual and deduction

Personal income tax is calculated for each amount of income actually received separately for the period (month).

The personal income tax amount is calculated and accrued using documents such as “ “, “ “, “ “ and so on.

As an example, let’s take the “Payroll” document:

Get 267 video lessons on 1C for free:

On the “Personal Income Tax” tab we see the calculated tax amount. After posting the document, the following personal income tax transactions are created:

The document also creates entries in the “Income Accounting for personal income tax calculations”, according to which reporting forms are subsequently filled out:

In fact, the tax withheld from the employee is reflected in the accounting when posting documents:

- Personal income tax accounting operation.

Unlike accrual, the tax withholding date is the date of the posted document.

Separately, you should consider the document “Personal Income Tax Accounting Operation”. It is provided for calculating personal income tax on dividends, vacation pay and other material benefits.

The document is created in the “Salaries and Personnel” menu in the “Personal Income Tax” section, link “All documents on personal income tax”. In the window with a list of documents, when you click the “Create” button, a drop-down list appears:

Almost all documents that in one way or another affect personal income tax create entries in the register “Calculations of taxpayers with the budget for personal income tax.”

As an example, consider the formation of register entries tax accounting document “Write-off from current account”.

Let's add the document "" (menu "Salaries and Personnel" - link "Statements to the Bank") and based on it we will create a "Write-off from the current account":

After this, let’s look at the postings and movements in the registers that the document generated:

Formation of personal income tax reporting

Above, I described the main registers that are involved in the generation of basic personal income tax reports, namely:

In the window with a list of documents, click the create button and fill out the employee certificate:

The document does not generate transactions and entries in registers, but is only used for printing.

- (section 2):

The report relates to regulated reporting. You can also proceed to its registration from the “Personal Income Tax” section, the “Salaries and Personnel” menu, or through the “Reports” menu, the “1C Reporting” section, “Regulated Reports”.

An example of filling out the second section:

Checking withheld and accrued personal income tax

To check the correctness of tax accrual and payment to the budget, you can use “ “. It is located in the “Reports” menu, section – “Standard reports”.

Since 2011, a number of changes made to Chapter 23 of the Tax Code of the Russian Federation have come into force. Federal law dated July 27, 2010 No. 229-FZ. In particular, starting from 2011, keep records of Personal income tax agents are prescribed in tax registers, the forms of which are proposed to be developed independently. In the program "1C: Salaries and Personnel Management 8" (release 2.5.32) the tax register form has already been implemented. ABOUT new form and changes related to the accounting and calculation of personal income tax, says E.A. Gryanina, independent consultant.

paragraph 1 of article 230 of the Tax Code of the Russian Federation

Tax amount calculated

Amount of tax withheld

Tax amount transferred

.

In the register Calculations of tax agents with the personal income tax budget Coming Consumption Transfer of personal income tax to the budget.

List of documents Transfer of personal income tax to the budget of the Russian Federation can be called from the menu Taxes and contributions -> Transfer of personal income tax to the budget of the Russian Federation Taxes, paragraph Transfer of personal income tax to the budget of the Russian Federation(see Fig. 1).

Rice. 1

In the header of the document Transfer of personal income tax to the budget of the Russian Federation

In the tabular section Employees Fill in -> Individuals

Fill in -> Tax amounts

When posting a document Transfer of personal income tax to the budget of the Russian Federation Calculations of tax agents with the personal income tax budget.

Accounting for transferred personal income tax amounts for each taxpayer

The form of the tax register for personal income tax is not regulated by law, however, the new version of paragraph 1 of Article 230 of the Tax Code of the Russian Federation lists information that must be contained in the tax register. The composition of this information has been expanded compared to the data in Form 1-NDFL, which was used previously. In particular, tax agents now need to additionally take into account the amounts actually transferred for each individual person personal income tax indicating the date of transfer and details of the payment document. This amount will also need to be indicated in the information on the income of individuals in Form 2-NDFL for 2011. Thus, since 2011, tax agents must take into account three tax amounts for each individual:

Tax amount calculated- how much tax was accrued to be withheld from income individual;

Amount of tax withheld- how much tax was actually withheld when paying income to an individual;

Tax amount transferred- how much tax was actually transferred to budget system.

To register the amounts of the transferred tax in the program "1C: Salary and Personnel Management 8" a new document has been created Transfer of personal income tax to the budget of the Russian Federation. To record the amounts subject to transfer and actually transferred to the budget for each individual - a new accumulation register Calculations of tax agents with the personal income tax budget.

In the register Calculations of tax agents with the personal income tax budget with a "+" sign (by type of movement Coming) the amounts of tax withheld from individuals, subject to transfer to the budget, are reflected with a “-” sign (by type of movement Consumption) - transferred tax amounts. The balance in the register shows the amount of tax withheld from employees, but not yet transferred to the budget - it is this data that is used to automatically fill out the program document Transfer of personal income tax to the budget.

Please note that the document date and payment date must be no earlier than the first day of the month following the billing period.

After updating the program version, in information base it is necessary to register the transfer of personal income tax in relation to all income received by taxpayers starting from 01/01/2011. It is recommended to register personal income tax transfer upon payment.

List of documents Transfer of personal income tax to the budget of the Russian Federation can be called from the menu Taxes and contributions -> Transfer of personal income tax to the budget of the Russian Federation or from the program desktop: bookmark Taxes, paragraph Transfer of personal income tax to the budget of the Russian Federation(see Fig. 1).

Rice. 1

Personal income tax transfers are registered in the program separately for each month of the tax period, for each tax rate and OKATO+KPP code.

In the header of the document Transfer of personal income tax to the budget of the Russian Federation you should indicate: the date of payment, the month of the tax period for which the tax was transferred, details of the payment order for payment of the tax, the tax rate, in the case of separate divisions - specify the OKATO/KPP code, and enter the total amount of the transferred tax at this tax rate and code OKATO/KPP.

In the tabular section Employees- indicate how much tax was transferred for each specific taxpayer. The list of employees can be filled in automatically by command Fill in -> Individuals who received income. The list will include all individuals for whom tax amounts for transfer are registered in the program. The amount for each individual will be calculated by proportional distribution of the total amount indicated in the header of the document. If necessary, the amounts in the tabular section can be adjusted manually. The total tax amount for all taxpayers must coincide with the amount indicated in the header of the document.

If the list of employees in the document is selected manually, then the command is used to distribute the total tax amount between employees Fill in -> Tax amounts(allows you to fill out tax amounts without refilling the list of individuals).

When posting a document Transfer of personal income tax to the budget of the Russian Federation the amounts of transferred tax for each individual indicated in the tabular part are recorded in the accumulation register Calculations of tax agents with the personal income tax budget.

The distribution is made in proportion to the amount of tax to be transferred for each individual (the balance according to the accumulation register Calculations of tax agents with the budget for personal income tax). For example, if, for some reason, only 50% of the total withholding from employees is paid to the budget personal income tax amounts, then for each individual the transfer of half the amount of tax withheld from him will be registered.

Tax accounting register for personal income tax

To compile a tax accounting register for personal income tax, a new report has been added to the program Tax accounting register for personal income tax. The report can be called using the submenu item of the same name Taxes and fees or from bookmarks Taxes program desktop.

Using this report, you can generate tax accounting registers for personal income tax for the selected taxable period immediately for all employees of the organization or only for a selected list of individuals.

The personal income tax register form implemented in the program fully complies with the requirements for the composition of information specified in paragraph 1 of Article 230 of the Tax Code of the Russian Federation. Let us recall that in accordance with paragraph 1 of Article 230 of the Tax Code of the Russian Federation, the tax register must contain information that allows identification of the taxpayer, the type of income paid to the taxpayer and tax deductions provided in accordance with established codes, the amount of income and the date of their payment, the status of the taxpayer, the dates of withholding and tax transfers to the budget system of the Russian Federation, details of the corresponding payment document.

The Register includes 7 sections.

Section 1 contains information about the tax agent.

Section 2 contains information about the taxpayer (recipient of income). Paragraph 2.9 provides information about the tax status of the taxpayer in table form. For designation, the same taxpayer status codes are used as for form 2-NDFL: 1 - tax resident, 2 - non-resident, 3 - highly qualified foreign specialist.

Section 3 provides information about a taxpayer's right to standard tax deductions. This information is filled in based on the deduction data specified for the individual in the form Entering data for personal income tax(see Fig. 2).

Rice. 2

Section 4 provides calculation information tax base and personal income tax. Section 4 is formed separately for each OKATO/KPP code. If during the tax period an employee worked and received income in various separate divisions, then the Register of this employee will contain several sections 4. Section 4 consists of several subsections.

Subsection Calculation of personal income tax at the rate of __% is formed separately for each tax rate. In the subsection, by month of the tax period, the codes and amounts of income received by the taxpayer, the amount of taxable income and calculated tax are given. For income taxed at a rate of 13%, an additional table is displayed with information about the tax deductions actually provided to the taxpayer.

In subsections Tax calculated, Tax withheld And Tax transferred the amounts of calculated, withheld and transferred tax are given accordingly by month of the tax period and tax rates. A separate column indicates the date of the transaction: calculation, deduction, transfer of tax. For the amounts of the transferred tax, details of the payment order are additionally displayed (see Fig. 3).

Rice. 3

Section 5 indicates total amounts tax deductions actually provided to the taxpayer as a whole for the tax period. The information is displayed in the context of OKATO/KPP codes and deduction codes.

Section 6 provides the total amounts of income and tax based on the results of the tax period, broken down by OKATO/KPP codes and tax rates.

Section 7 specifies information about the submission of taxpayer income certificates in Form 2-NDFL.

Changes in the calculation of personal income tax related to changes in the Tax Code of the Russian Federation

Since 2011, the procedure for calculating personal income tax for individual cases has changed.

Newly in 2011, tax is calculated if an employee is provided with property deductions. The changes apply to the month from which the deduction begins to apply. In accordance with the new edition of Article 220 of the Tax Code of the Russian Federation, property tax deductions are provided for employee income received starting from the month the employee submitted an application for such a deduction. Previously, the deduction was provided for income from the beginning of the tax period, regardless of the month in which the employee submitted the application. When calculating personal income tax in the month of submission of the application, the program recalculated the tax from the beginning of the year, and it was possible to return or offset the amount of tax on income for previous months. In 2011, tax recalculation for the months of 2011 preceding the month the employee submitted the application is not performed.

In addition, the procedure for calculating tax when an employee acquires the status of a tax resident of the Russian Federation has changed. In accordance with the new edition of Article 231 of the Tax Code of the Russian Federation, recalculation and refund of tax when a taxpayer acquires tax resident status is carried out by the tax office. Previously, the tax agent could recalculate and return the tax in this case, so the program recalculated the tax at a rate of 13% for the entire tax period. In 2011, when an employee acquires the status of a tax resident of the Russian Federation, the tax from the beginning of the year is not recalculated, but begins to be calculated at a rate of 13% from the month of change of status.

Examples of tax calculation for these cases are discussed in the ITS reference book “Maintaining personnel records and settlements with personnel in 1C programs.”

Change in personal income tax calculation related to the personal income tax calculation subsystem

Let us note one more change in the program related to the personal income tax calculation subsystem. The location where information about an employee's tax status is entered has changed. Previously, input was carried out in the form of entering data on the citizenship of an individual. Now the taxpayer status is indicated on a special page of the form Entering data for personal income tax(called from the individual’s data form using the button Personal income tax, or from the field Status directory Employees) - see fig. 4.

2016-12-08T15:29:55+00:00Question from reader Marina Vasilievna:

Put new program 1 C 8.3 Accounting. I'm not quite familiar with this program yet.

We rent a car from an individual, I rent I register through manual transactions DT 44.1 CT 76.5 and also charge personal income tax DT 76.5 CT 68.1.

But the accrued personal income tax does not fall into the personal income tax register. In 1C Accounting 7.7, I carried out this personal income tax through Adjusting personal income tax data,

But in 1C 8.3 I can’t find such a function. If possible, please help me.

Answer:

To reflect settlements with the budget for personal income tax in tax accounting an accumulation register is provided: " Calculations of tax agents with the personal income tax budget".

If we open this register using the " " menu:

then we will see something like this:

All these are movements according to the register, formed when paying salaries to employees.

But our task is to reflect these same movements when withholding personal income tax from the individual from whom we rent the car, directly in a manual transaction. How to do it?

Let's open a manual operation in which we reflect our transactions:

DT 44.1 KT 76.5

DT 76.5 KT 68.1

I have everything very schematically:

And from the topmost item “More” select the item “Select registers”:

A list of registers will open; we need to check the boxes for those whose movements we want to display:

Click "OK" and see that "Operation" appears in the document additional tab to edit register:

Click the “Add” button and fill out the line for personal income tax receipt for the individual we need:

Sincerely, Vladimir Milkin(teacher and developer).