Maintenance algorithm separate accounting is not defined in the Tax Code of the Russian Federation, so it must be developed independently and stated in the accounting policy.

Persons combining modes must organize separately:

- Accounting for income received from activities on UTII and from activities on the simplified tax system;

- Accounting for costs aimed at the simplified tax system, activities on UTII, as well as those distributed between UTII and the simplified tax system.

- Separate accounting of costs aimed at paying employees and insurance premiums from them.

Separate accounting of income when combining simplified taxation system and UTII in 1C 8.3

In case of combining UTII and simplified tax system, the taxpayer is obliged to carry out separate accounting of income received:

- from activities on the simplified tax system;

- from activities on UTII.

Separate accounting of income must be maintained to determine:

- tax base when calculating the simplified tax system;

- shares of income under the simplified tax system and UTII in the total volume of income for the purpose of dividing expenses.

In 1C 8.3 Accounting ed. 3.0 there are various sub-accounts for accounting for income under UTII and simplified tax system:

- for simplified tax system

- 01.1 – Revenue under the simplified tax system;

- for UTII– second-order subaccounts ending in 2;

- 01.2 – Revenue with UTII:

Income accounts in 1C 8.3 are entered in the document “Sales (acts, invoices)”:

The share of income from activities under the simplified tax system for the purpose of dividing expenses in the total amount of income is determined by the formula:

What method is used to determine income?

To determine income under the simplified tax system, the cash method is used. For UTII, data is used accounting using the cash method.

In the same way, in 1C 8.3, to calculate the share of income, the amount of income is determined, that is:

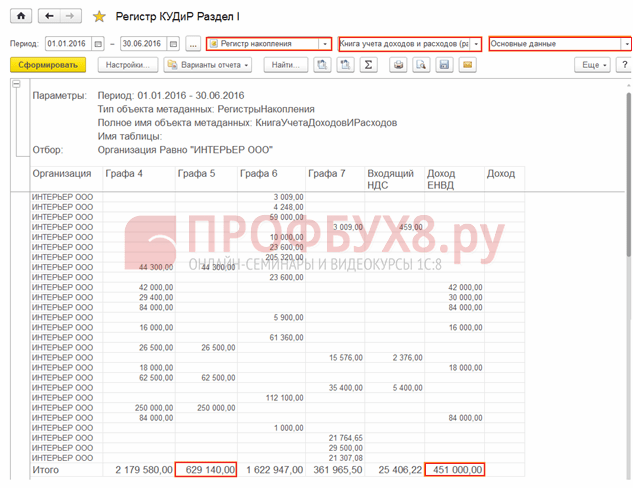

- income under the simplified tax system can be determined on the basis of column 4 of the “KUDiR” Report, and in the register “KUDiR (Section I)” This is the “Income” column(gr. 5):

- income for UTII is determined according to accounting data using the cash method - This is the column “UTII income” in the register “KUDiR (section I)” (Universal report, for the same register):

For what period are incomes taken into account?

Income is determined:

- for the simplified tax system – on an accrual basis for the year;

- for UTII - per quarter.

For comparability of indicators, the Ministry of Finance advises in letter dated November 26, 2015 N 03-11-11/68786 to consider income as an accrual total both under the simplified tax system and under UTII.

In 1C 8.3, income is considered a cumulative total from the beginning of the year, and when calculating the share of income, an adjustment occurs every quarter.

You can see in 1C 8.3 Accounting how the share of income was calculated in the report “Analysis of accounting according to the simplified tax system” - link “Distributed expenses of the simplified tax system / UTII”:

The coefficient in 1C 8.3 is calculated for UTII.

What is the composition of income?

According to clarifications of the Ministry of Finance dated April 28, 2010 No. 03-11-11/121, as part of income under the simplified tax system and under UTII taken into account:

- income from sales (Article 249 of the Tax Code), non-operating income(Article 250 of the Tax Code), except for income not taken into account in the National Tax Code (Article 251 of the Tax Code).

If “other income” is received, for example, in the form of bonuses, bonuses and it cannot be attributed to a specific regime (UTII or simplified tax system), then it must also be divided according to the separate accounting method. “Other income” in 1C 8.3 is not automatically distributed. It must be distributed manually according to the principle established in the accounting policy and entered into the program as separate entries.

For more details on how income is reflected under the simplified tax system in 1C 8.3 and how to avoid mistakes when reflecting the costs of purchasing an OS, see our video:

Separate accounting of expenses when combining simplified taxation system and UTII in 1C 8.3

When combining modes, it is important to consider the following points:

- Expenses under the simplified tax system reduce income when calculating the simplified tax system for the object “Income minus expenses” according to the “closed” list in Article 346.16 of the Tax Code of the Russian Federation.

- AccountingexpenseDov on UTII maintained for accounting purposes only. accounting. Tax accounting of expenses is not required.

- Expenses that cannot be attributed to a specific tax regime (STS or UTII), should be distributed in proportion to the shares of income in the total amount of income attributable to the simplified tax system or UTII (clause 8 of article 346.18 of the Tax Code of the Russian Federation).

How to reflect expenses when combining simplified taxation system and UTII in 1C 8.3

There are various sub-accounts for accounting for expenses under the simplified tax system and UTII:

- for simplified tax system– second-order subaccounts ending in 1;

- 02.1 – Cost of sales under the simplified tax system;

- 07.1 – Selling expenses under the simplified tax system;

- 08.1 – Administrative expenses with simplified tax system;

- for UTII– second-order subaccounts ending in 2:

Expense accounts in the 1C 8.3 Accounting program ed. 3.0 are also entered in the document “Implementation (acts, invoices)”.

Distribution of expenses when combining UTII and simplified tax system in 1C 8.3

Filling out cost items in the “Cost Items” and “Other Income and Expenses” directories:

- Costs related only to the simplified tax system – check the box “For activities with the main taxation system (general or simplified)”:

- Costs related only to UTII – when filling out this element of the directory, it is necessary in the section Organizational cost accounting item check the "By certain species activities with a special taxation procedure":

- Costs that cannot be attributed to the simplified tax system or UTII, that is, subject to distribution - when filling out this element of the directory, it is necessary in the section Organizational cost accounting item check the "By different types activities":

Setting a cost attribute in documents

In the document form, when reflecting costs, the following value can be selected:

- Accepted– only for costs related to the simplified tax system, if they can be taken into account in the KUDiR in accordance with Article 346.16 of the Tax Code of the Russian Federation;

- Not accepted– for all costs under UTII and for costs under the simplified tax system that are not listed in Article 346.16 of the Tax Code of the Russian Federation and cannot be reflected in the KUDiR;

- Distributed– for costs that cannot be attributed to a specific regime (STS or UTII), subject to distribution:

“Total” distributed expenses attributable to the simplified tax system are determined by the formula:

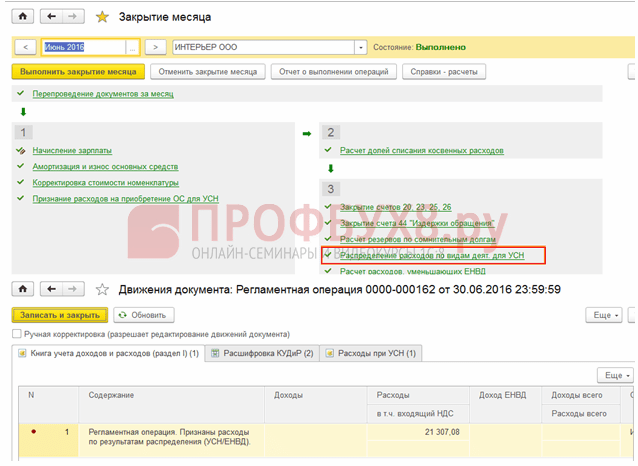

In the 1C 8.3 program, they are automatically distributed during the month-end closing procedure for the quarter - the document “Distribution of expenses by type of activity. for simplified tax system":

This amount will be reflected in the report “Book of Income and Expenses of the simplified tax system”:

You can check the calculation of the share of income for the distribution of expenses attributable to the simplified tax system using the report:

- Report “Analysis of accounting according to the simplified tax system”;

- Universal report on the accumulation register “Book of Income and Expenses (Section I)” – “Basic Data”:

- column 5 – the amount of income received under the simplified tax system (equal to column 4 of Section I of the report “KUDiR simplified tax system”);

- column “UTI Income” – the amount of income received under UTII, calculated using the cash method.

Accounting for labor costs and insurance premiums

When “simplified” (Object “Income minus expenses”):

- Labor costs (including withheld personal income tax) are included in expenses at the time of debit from the bank account or payment Money from the cash register, and with another method - at the time of payment of the debt (Article 346.17 of the Tax Code of the Russian Federation);

- Insurance premiums are taken into account in tax accounting as expenses only after they have been paid.

For UTII:

- Accounting for expenses is carried out only for accounting purposes. Tax accounting of expenses for salaries and insurance contributions is not required.

It is necessary to organize separate accounting for the payment of wages to employees and insurance contributions from them. To do this, you need to divide employees by type of activity. And if such a division is not possible, then labor costs must be distributed in proportion to the shares of income in the total amount of income received from combining the simplified tax system and UTII. This is important because:

- under the simplified tax system (“Income”) and UTII insurance premiums reduce the tax (clause 3.1 of article 346.21 and clause 2 of article 346.32 of the Tax Code);

- under the simplified tax system (“Income minus expenses”), insurance premiums are taken into account as expenses.

Organization of separate accounting for employee benefits in 1C 8.3

Step 1. Determine the relationship of each employee to activities on UTII

In the Employees directory you can set the following values:

- “Fully on UTII” - the employee is fully engaged in activities on UTII;

- “Does not apply to UTII” - the employee is fully engaged in activities on the simplified tax system;

- “Determined monthly by percentage” - it is impossible to unambiguously determine what type of activity (UTII or simplified tax system) the employee is engaged in:

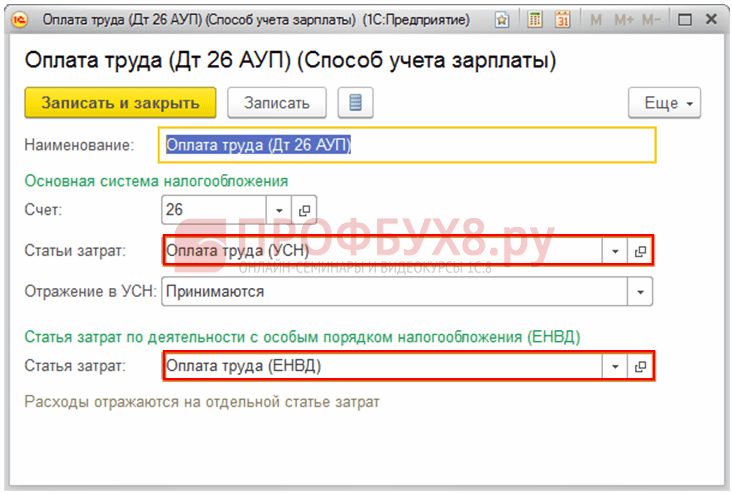

Step 2. Set a template for accounting entries for payroll and the procedure for recognizing expenses for activities under the simplified tax system for each employee

Directory Method of salary accounting:

With this setup, you will not need to create elements for each type of accounting in the Accruals directory. The directory element in this case will look like this:

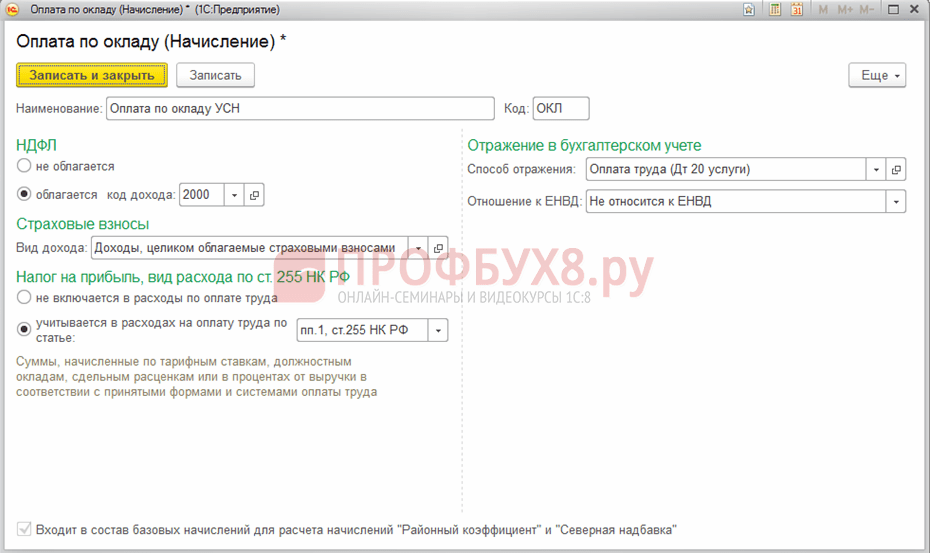

The accounting reflection parameters are not filled in. This data is filled in on the employee’s card.

There is another option for organizing separate accounting for employee benefits in 1C 8.3. The relationship to accounting types can be indicated in the Accruals directory. Then, to calculate “Payment by salary”, for example, you will need to create three elements:

Today, accounting in almost every enterprise is automated. The program "1C: Enterprise Accounting" is comprehensive solution to reflect business transactions and is suitable for enterprises with any taxation system.

There are often cases when an organization, together with the main taxation system, uses a taxation system in the form of a single tax on imputed income. In such cases, accountants have questions about how to divide income and expenses for each tax system in the 1C: Enterprise Accounting program.

This article discusses the features of accounting of a company using a simplified taxation system and UTII, using the example software product"1C: Enterprise Accounting, edition 2.0."

The division of income and expenses for each type of activity is necessary for the correct calculation of the amount of tax under the simplified taxation system. The amount of the single tax on imputed income does not depend on the amount of income and expenses.

Setting up accounting policies

In order for business transactions to be reflected in the 1C: Enterprise Accounting program correctly and accurately, you must first set up an accounting policy. To do this, use the “Enterprise” menu item and select “Accounting Policy” from the drop-down list.In the window that opens, the user sees a list of all saved accounting policies. To check basic settings accounting policy You should open the record for the current reporting period.

On the tab " General information» contains information about the applied taxation systems and the types of activities used.

The “UTII” tab contains information about the method and basis for the distribution of expenses with the main and special taxation procedures, and also establishes accounts for income and expenses for activities falling under UTII.

The “UTII” tab contains information about the method and basis for the distribution of expenses with the main and special taxation procedures, and also establishes accounts for income and expenses for activities falling under UTII. The default cost allocation method is “per quarter”. This means that in last month every quarter regulatory operation expenses to be distributed are recognized in order to include them in the ledger of income and expenses. It is also possible to set up “cumulative total from the beginning of the year”.

When you click on the link “Set up income and expense accounts,” a list of accounts opens that will record income and expenses for UTII activities. By default, the program suggests reflecting income and expenses for UTII activities in accounts 90.07.2, 90.08.2, 90.01.2 and 90.02.2. This list can be supplemented with other accounts by using the “Add” button.

The “Accounting for Expenses” tab contains information about the procedure for recognizing expenses for activities that fall under the simplified taxation system.

The “Accounting for Expenses” tab contains information about the procedure for recognizing expenses for activities that fall under the simplified taxation system.  According to the above setting, expenses for the purchase of goods will be recognized to create a book of income and expenses under the following conditions:

According to the above setting, expenses for the purchase of goods will be recognized to create a book of income and expenses under the following conditions: - Receipt of goods, i.e. the fact of receipt of goods is reflected in the corresponding document “Receipt of goods and services”;

- Payment for goods to the supplier, i.e. the fact of payment for goods is reflected in the relevant documents “Write-off from the current account” or “Expense cash order»;

- Sales of goods, i.e. the fact of shipment of goods to the buyer is reflected in the corresponding document “Sales of goods and services”.

Splitting expenses by type of activity

To correctly divide expenses by type of activity, use the “Cost Items” directory. You can find this directory in the “Production” tab or through the “Operations” menu by selecting “Directories”.This directory contains a standard set of cost items proposed by the program by default, but the directory data can be changed by the user.

The card for each cost item provides three expense options:

- For activities with the main taxation system.

Expenses with such a cost item will automatically be considered expenses for activities falling under the simplified tax system. - For certain types of activities with a special taxation procedure.

Expenses with such a cost item will automatically be considered expenses for activities falling under UTII. - For different types of activities.

Expenses with such a cost item cannot be attributed to a specific type of activity. The amount of such expenses at the end of the month is distributed among the types of activities through a routine operation.

When maintaining accounting in the 1C: Enterprise Accounting program, you should remember that these cost items determine whether an expense belongs to a specific type of activity when accepting services from third-party organizations for accounting. When buying and selling goods, various accounts are used to identify types of expenses and income.

Income and expenses related to the simplified tax system from the sale of goods

Since the cost of purchasing a batch mobile phones relate to expenses for activities of the simplified tax system, in the “NU Expenses” column of the “Goods” tabular section, you should select the “Accepted” value.

Since the cost of purchasing a batch mobile phones relate to expenses for activities of the simplified tax system, in the “NU Expenses” column of the “Goods” tabular section, you should select the “Accepted” value. After posting the document, the debt to the supplier is reflected, and the balance on account 41.01 is increased. In addition, the corresponding movements are formed in the “STS Expenses” register.

Payment for received goods in this example is made using the document “Write-off from current account”.

Carrying out of this document reflects the debiting of money from the current account and closes the debt to the supplier. In addition, the “STS Expenses” register is supplemented with the necessary entries.

The document “Write-off from the current account” can be entered on the basis of “Receipt of goods and services”, filled out manually or downloaded from the corresponding “Client-Bank” program.

The last step to recognize expenses under the simplified tax system is to reflect the fact of shipment of goods to the buyer. This business transaction is formed using the document “Sales of goods and services”.

In order to identify expenses and income for activities falling under the simplified taxation system, you should use income account 90.01.1 and expense account 90.02.1.

In order to identify expenses and income for activities falling under the simplified taxation system, you should use income account 90.01.1 and expense account 90.02.1. After the “Sale of Goods and Services” is carried out, the balance of goods in the warehouse is reduced, the buyer’s debt is formed, and movements are also formed on the accounts in which revenue and cost are taken into account. In addition, an entry is created in the book of income and expenses, reflecting the recognition of expenses for the sales amount.

Revenue is recognized for this transaction upon receipt of payment from the buyer. This fact is reflected in the program “Cash receipt order” or “Receipt to current account”. For this example, the document “Receipt to current account” is used. After this document is completed, the balance on the current account increases and the buyer’s debt decreases. In addition, an entry is created in the income and expense ledger to reflect the recognition of income for the amount received from the customer.

Income and expenses related to UTII from the sale of goods

The receipt of goods intended for subsequent sale is documented in the document “Receipt of goods and services”. Since the costs of purchasing a batch of electronic books relate to UTII, in the “Expenses (NU)” column of the tabular part of the document you should select “Not accepted”.

Since the costs of purchasing a batch of electronic books relate to UTII, in the “Expenses (NU)” column of the tabular part of the document you should select “Not accepted”. Identification of expenses for the purchase of goods for UTII activities is determined through the use of the appropriate accounts, which will reflect revenue and cost (90.01.2 and 90.02.2). These accounts are defined in the document “Sales of goods and services”.

Payment of goods to the supplier and receipt of payment from the buyer is reflected in the documents “Write-off from the current account” or “Cash outgoing order” or “Receipt to the current account” or “Cash incoming order”.

Payment of goods to the supplier and receipt of payment from the buyer is reflected in the documents “Write-off from the current account” or “Cash outgoing order” or “Receipt to the current account” or “Cash incoming order”. Reflection of expenses associated with the provision of services by third parties

Expenses associated with the provision of services by third parties are reflected using the “Receipt of goods and services” document. As stated earlier, there are three types of expenses: expenses related to the main activity, i.e. simplified tax system; expenses related to individual activities, i.e. UTII, and expenses subject to distribution.For purposes of this article There are three cost items, each of which corresponds to a specific type of activity:

- Software maintenance.

These expenses relate to the simplified tax system. - Public utilities.

These expenses relate to UTII. - Rent.

These expenses cannot be attributed to a specific type of activity, and the amount of these expenses should be distributed between the types of activities at the end of each month.

Let us consider in detail the procedure for reflecting each type of expense in the program.

Balance sheet before determining income

for each type of activity

After all current business transactions are reflected in the program, you can make a standard report “Turnover balance sheet”.  Based on this report, we can see the amount of expenses generated by the cost of services of third-party organizations (account 44.01), revenue and cost of goods for each type of activity (accounts 90.01 and 90.02), as well as movements on other accounts.

Based on this report, we can see the amount of expenses generated by the cost of services of third-party organizations (account 44.01), revenue and cost of goods for each type of activity (accounts 90.01 and 90.02), as well as movements on other accounts. Determination of profit for each type of activity

Profit for each type of activity is determined using the “Month Closing” document. The routine operations of this document close cost accounts and also determine profit.The routine operation “Closing account 44 “Costs of circulation” writes off the amount of expenses reflected in account 44 to accounts 90.07.1 and 90.07.2, depending on whether the expense belongs to the simplified tax system or UTII. This operation also distributes the amount of expenses related to different types of activities. After the operation, you can generate a calculation certificate, which will indicate the amounts attributed to expenses for each type of activity and the procedure for their calculation.

Organization: LLC "Alisa"

| Help-calculation | Number | date | Period |

| 31.01.2013 | January 2013 |

Write-off of indirect expenses (accounting)

Write-off indirect costs for production and sales related to activities not subject to UTIIWrite-off of indirect costs for production and sales related to different types of activities, distributed in proportion to income

| Current month's expenses | Written off | |||

| Account | Cost item | Sum | By type of activity with the main tax system (gr.3) * 0.615385(**) |

By type of activity with a special taxation procedure (gr.3) * 0.384615(**) |

| 1 | 2 | 3 | 4 | 5 |

| 44.01 | Rent | 5 000,00 | 3 076,92 | 1 923,08 |

| Total: | 5 000,00 | 3 076,92 | 1 923,08 | |

Write-off of indirect costs for production and sales related to activities subject to UTII

** - Calculation of the share of income for each type of activity in the total income for the current month

| For the current month | Share of income in total income | ||

| For activities subject to income tax | For activities not subject to income tax | For activities subject to income tax (gr.1 / (gr. 1 + gr.2) |

For activities not subject to income tax gr.2 / (gr. 1 + gr.2) |

| 1 | 2 | 3 | 4 |

| 80 000,00 | 50 000,00 | 0,61538 | 0,38462 |

After all the regulatory operations of the “Month Closing” document have been successfully completed, you can generate a balance sheet.

Below is a fragment of the balance sheet for accounts 90 and 99.

Based on the balance sheet, the following conclusions can be drawn:

Based on the balance sheet, the following conclusions can be drawn: - Expenses for activities with the main taxation system (USN) amounted to 45,076.92 rubles. (debit balance of account 90.02.1 + debit balance of account 90.07.1);

- Expenses for UTII activities amounted to 33,923.08 rubles. (debit balance of account 90.02.2 + debit balance of account 90.07.2);

- Profit from activities with the main taxation system (USN) amounted to 34,923.08 rubles. (credit balance of account 99.01.1 = credit balance of account 90.01.1 – debit balance of account 90.02.1 – debit balance of account 90.07.1);

- Profit on UTII amounted to 16,076.92 rubles. (credit balance of account 99.01.2 = credit balance of account 90.01.2 – debit balance of account 90.02.2 – debit balance of account 90.07.2).

Book of income and expenses

All recognized income and expenses are included in the income and expense ledger. Part of the expenses subject to distribution, which relate to the simplified tax system, is calculated at the end of each quarter by the regulatory operation “Distribution of expenses by type of activity according to the simplified tax system.” The book of income and expenses has the following form.

The book of income and expenses has the following form.  In this report you can see the documents supporting the acceptance of income and expenses, as well as total amounts received income and expenses.

In this report you can see the documents supporting the acceptance of income and expenses, as well as total amounts received income and expenses. Analysis of the state of tax accounting according to the simplified tax system

Condition Analysis tax accounting according to the simplified tax system is a report that indicates the amounts of income and expenses related to the simplified tax system, with their detailed breakdown. When you double-click on the amount, a detailed breakdown of income and expenses is displayed.

When you double-click on the amount, a detailed breakdown of income and expenses is displayed.

We tell you how to"1C:Accounting 8"tax accounting data is adjusted when applying the simplified tax system.

Note:

* How to fix errors current year and previous years when applying the general taxation system, read the articles:

General principles for adjusting tax accounting

The general principles for adjusting tax accounting and reporting are set out in Articles 54 and 81 of the Tax Code of the Russian Federation and do not depend on the taxation system used - general or simplified.

In accordance with paragraph 1 of Article 81 of the Tax Code of the Russian Federation, a taxpayer who discovered in the information submitted by him tax authority declaration non-reflection or incomplete reflection of information, as well as errors:

- must make the necessary changes to the tax return and submit an updated tax return to the tax authority if errors (distortions) led to an understatement of the amount of tax payable;

- has the right make the necessary changes to the tax return and submit an updated tax return to the tax authority if errors (distortions) do not lead to an understatement of the amount of tax payable.

Errors (distortions) that did not lead to an understatement of the amount of tax payable when applying the simplified tax system include failure to reflect or understate expenses, as well as overstatement of income. And, of course, the taxpayer is interested in returning the overpayment of taxes resulting from these situations or offsetting them against future payments. This can be done by filing an amended return or, in some cases, by making changes to tax accounting data in the current period.

IN general case errors (distortions) relating to previous tax (reporting) periods and detected in the current tax (reporting) period are corrected by recalculation tax base and the amount of tax for the period in which the indicated errors (distortions) were committed (clause 1 of Article 54 of the Tax Code of the Russian Federation).

At the same time, the taxpayer has the right to recalculate the tax base and tax amount in the tax (reporting) period in which errors (distortions) were identified if:

- it is impossible to determine the period of commission of these errors (distortions);

- such errors (distortions) led to excessive payment of tax.

When commenting on the taxpayer’s right to correct errors (distortions) in the current period, regulatory authorities draw attention to the fact of the existence of a tax base in the current period. If in the current reporting (tax) period the organization incurred a loss, then in this period recalculation of the tax base is impossible, since the tax base is recognized as equal to zero (clause 8 of Article 274 of the Tax Code of the Russian Federation, letter of the Ministry of Finance of Russia dated March 24, 2017 No. 03-03-06 /1/17177).

As for the condition of excessive tax payment in the previous period, then, in the opinion of the Russian Ministry of Finance, it is not fulfilled if specified period the organization incurred a loss, or the tax base was equal to zero. Therefore, in such situations, corrections must be made during the period of the error (letter dated 05/07/2010 No. 03-02-07/1-225).

The explanations given relate to the adjustment of the tax base for income tax. Despite this, we believe that under the simplified tax system it is also impossible to “edit” tax accounting in the current period if an error in calculating the tax base was made in a “zero” or “unprofitable” declaration, or if a loss was incurred in the current period.

According to Article 346.24 of the Tax Code of the Russian Federation, tax accounting under the simplified tax system is the accounting of income and expenses in the book of income and expenses of organizations and individual entrepreneurs using the simplified taxation system (hereinafter referred to as KUDiR).

In "1C: Accounting 8" report Book of income and expenses of the simplified tax system(chapter Reports) is filled in automatically based on special accumulation registers. Entries in accounting registers for the purposes of the simplified tax system are entered, as a rule, automatically when posting documents that register business transactions. For manual registration of register entries, use the document (chapter Operations - simplified tax system).

The date of receipt of income is the day of receipt of funds, as well as the day of payment to the taxpayer in another way - the cash method (clause 1 of Article 346.17 of the Tax Code of the Russian Federation).

The procedure for recognizing expenses depends on the conditions set out in paragraph 2 of Article 346.17 of the Tax Code of the Russian Federation, mandatory of which is their actual payment.

Thus, when correcting errors (distortions) made when reflecting (non-reflecting) business transactions in the accounting of an organization using the simplified tax system, tax accounting is adjusted in accordance with the provisions of Article 346.17 of the Tax Code of the Russian Federation, that is, taking into account the payment factor.

Accounting adjustments andreporting

Correcting errors (distortions) made when reflecting (non-reflecting) business transactions usually entails simultaneous adjustments to both tax and accounting records. The exception is individual entrepreneurs(IP) who are not required to keep accounting records (Article 6 Federal Law dated December 6, 2011 No. 402?FZ).

In accounting, errors and their consequences must be corrected in accordance with the Accounting Regulations “Correcting Errors in Accounting and Reporting” (PBU 22/2010), approved. by order of the Ministry of Finance of Russia dated June 28, 2010 No. 63n.

The procedure for correcting errors and adjustments financial statements depends on the significance of the error and the moment it was discovered. For example, a significant error from previous years, identified after the date of signing the financial statements, may lead to the fact that in some cases the organization will have to present revised financial statements or, what is much more serious, correct the comparative indicators of the financial statements by retrospective recalculation (clauses 9, 10 of PBU 22/2010).

It should be borne in mind that inaccuracies or omissions in the reflection of facts are not errors. economic activity in accounting (reporting), identified as a result of receiving new information, unavailable at the time of its reflection (clause 2 of PBU 22/2010). The provisions of PBU 22/2010 do not apply to these situations that are not errors, which means that in accounting such distortions must be corrected at the time they are identified without retrospective recalculation. However, it is not always clear how to determine the criterion for information availability.

In any case, small businesses (and these include the majority of simplifiers) are allowed to correct all errors of previous years in a simplified manner, which is established for minor errors, that is, taken into account as part of other income or expenses of the current reporting period without retrospective recalculation (clause 9 PBU 22/2010).

Adjustment of sales for the reporting year

In "1C: Accounting 8" edition 3.0, there are mechanisms for automatically adjusting tax and accounting data (in a simplified manner) through special documents. Let's consider how the program can reflect the adjustment of the reporting year's implementation when applying the simplified tax system.

Example 1

|

Romashka LLC applies the simplified tax system with the object of taxation “income reduced by the amount of expenses.” In December 2016, funds in the amount of RUB 25,000.00 were transferred to the bank account of Romashka LLC. as an advance payment from a wholesale buyer. In the same month, 50 units of goods were sold to this buyer for the amount of RUB 25,000.00. The specified goods have been fully paid to the supplier. In February 2017, a wholesale buyer discovered a hidden defect in 10 units of goods. By agreement with Romashka LLC, the buyer, instead of returning poor quality goods disposed of it, and Romashka LLC transferred the corrected primary document to the buyer. Adjustments to the accounting of Romashka LLC were made before the presentation tax return according to the simplified tax system for 2016 and before signing the financial statements for 2016. |

The receipt of funds from the wholesale buyer is registered in the program with a document Receipt to the current account(chapter Bank and cash desk - Bank statements ) with the type of operation Payment from the buyer. An organization using the simplified tax system in the field Advance to NU must explicitly indicate the accounting procedure for advances for tax accounting purposes. According to the conditions of Example 1, you must specify the value in this field: Income simplified tax system by selecting it from the list offered by the program.

When posting a document, an accounting entry is generated:

Debit 51 Credit 62.02 - for the amount of the prepayment (RUB 25,000.00).

Amount 25,000.00 rub. recorded in the register as income of the simplified tax system.

Sales of goods in wholesale trade reflected standard document Sales (deed, invoice) with the type of operation Goods (invoice).

When posting a document, accounting entries:

Debit 90.02.1 Credit 41.01 - for the cost of goods (RUB 12,500.00); Debit 62.02 Credit 62.01 - for the offset amount of the prepayment (RUB 25,000.00); Debit 62.01 Credit 90.01.1 - for the amount of proceeds from the sale of goods (RUB 25,000.00).

For the purposes of tax paid in connection with the application of the simplified tax system, entries are made in the accumulation registers Book of income and expenses (section I), Decoding KUDiR And Expenses under the simplified tax system.

Since the goods sold were paid to the supplier, the amount is RUB 12,500.00. recorded in the register Book of income and expenses (section I) as expenses of the simplified tax system.

Amounts of income and expenses from the result of this transaction reflected in the register Book of income and expenses (section I), automatically fall into Section I of KUDiR for 2016:

- in the column “Income taken into account when calculating the tax base” - the amount of payment for goods sold (RUB 25,000.00);

- in the column “Expenses taken into account when calculating the tax base” - the cost of goods sold, paid to the supplier (RUB 12,500.00).

Let's say in February 2017 accounting service Romashka LLC received information that the buyer discovered that the registered goods were defective and disposed of them by agreement with the seller.

In this case, the program must reflect changes in accounting and tax accounting and generate the corresponding primary document*.

Note:

* 1C experts talked about the procedure for correcting and adjusting primary accounting documents using the program, as well as how to reflect changes made in the accounting of the seller and the buyer, in the article Correction and adjustment of primary records in “1C: Accounting 8” (rev. 3.0).

To adjust accounting and tax accounting data, as well as to generate corrected primary documents transferred to the buyer, the document is intended in 1C: Accounting 8 Implementation adjustments(chapter Sales). It is most convenient to create a document based on a document Sales (deed, invoice)(button Enter based on). On the bookmark Main in field Type of operation The following operations are available:

- - registers the change in the cost of previously sold goods, works and services, agreed upon between the seller and the buyer, that is, an independent event that relates to the current period. If the supplier is a VAT payer, then he must in this case issue an adjustment invoice to the buyer;

- - used to reflect the correction of errors made by the supplier when preparing documents. Correction in primary documents is not an independent event and refers to the same period as the document being corrected. The VAT payer supplier, correcting the primary documents, issues a corrected invoice to the buyer.

The correct qualification of these transactions is extremely important for VAT accounting purposes. For accounting entries and entries in tax registers for the purposes of the simplified tax system, the selected type of transaction in the document Implementation adjustments does not affect.

According to the conditions of Example 1, at the time of sale of the goods, Romashka LLC had no information about the presence of hidden defects in it.

Therefore in the document Implementation adjustments you must select the type of operation Adjustment by agreement of the parties, which reliably reflects the essence business transaction(Fig. 1).

Rice. 1. Implementation adjustments

In field Reflect adjustment you must leave the default value In all sections of accounting, then after posting the document, movements in the accounting and tax accounting registers will be generated.

Tabular part of the bookmark Goods filled in automatically based on the selected document Sales (deed, invoice). Each line of the source document corresponds to two lines in the adjustment document:

- before change;

- after change.

To line before change The quantity and amounts from the source document are transferred and this line is not edited. In line after change you need to indicate the corrected quantitative indicators, and the new total indicators will be recalculated automatically.

Document form Implementation adjustments on the bookmark Calculations varies depending on the period of making changes to the basis document.

If the document Implementation adjustments adjusts the implementation:

- current year - additional parameters for reflecting income and expenses from the adjustment are not required, since all adjustments will be made in the current year.

- last year - bookmarked Calculations in Group Reflection of income and expenses an additional parameter appears: .

Under the terms of Example 1, corrections to accounting data are made in 2017, but before the signing of the financial statements for 2016, so the flag Last year's accounting is closed for adjustments (reporting has been signed) no need to install.

Even though the document Implementation adjustments dated February 2017, after the document is processed, part of the transactions is formed with the date December 31, 2016, namely:

REVERSE Debit 90.02.1 Credit 41.K - for the cost of defective goods (-2,500.00 rub.); REVERSE Debit 76.K Credit 90.01.1 - for the amount of proceeds from the sale of goods (-5,000.00 rub.); Debit 99.01.1 Credit 90.09 - for the amount of the adjustment financial result(RUB 2,500.00).

Accounting data adjusted in this way will automatically be included in the financial statements for 2016.

As of document date Implementation adjustments(02/27/2017) the following accounting entries are generated:

REVERSE Debit 41.K Credit 41.01 - for the amount of adjustment of goods (-2,500.00 rub.); REVERSE Debit 62.01 Credit 76.K - for the amount of adjustment of settlements with the buyer (-5,000.00 rub.); Debit 62.01 Credit 62.02 - for the allocation of an advance received from the buyer (RUB 5,000.00).

Account 76.K “Adjustment of calculations of the previous period” serves to take into account the result of adjustments to settlements with counterparties that were made after the end of the reporting period. Debt for settlements with counterparties is recorded on the account from the date of the transaction that is subject to adjustment to the date of the correcting transaction.

Account 41.K “Adjustment of goods of the previous period” serves to take into account the result of adjustments to inventory balances that were made after the end of the reporting period. Adjustment of inventory balances and (or) their value is taken into account on the account from the date of the transaction that is subject to adjustment to the date of the adjusting transaction. It is easy to see that the amounts in accounts 76.K and 41.K are in transit, so why are they needed then? Thanks to special accounts 76.K and 41.K, information on settlements with counterparties and product balances falls into the required section of the reporting, but at the same time this information cannot be used until the adjustment is reflected. When this moment comes, settlements with counterparties and goods balances are transferred to “regular” settlement or goods accounts.

For example, goods credited to account 41.K as a result of last year’s adjustment are reflected in line 1210 “Inventories” balance sheet, but cannot be used in transactions until the adjustment is reflected in the current year.

For the purposes of tax paid in connection with the application of the simplified tax system, to accumulation registers Book of income and expenses (section I), Decoding KUDiR And Expenses under the simplified tax system adjusting entries are also entered.

In the register Book of income and expenses (section I) the expense of the simplified tax system is reversed in the amount of 2,500.00 rubles, and in Section I of the report Book of income and expenses of the simplified tax system for 2016, a record of a decrease in consumption is automatically reflected in the last line (Fig. 2).

Rice. 2. Book of income and expenses for the fourth quarter of 2016

Document for income recognition Implementation adjustments does not have any effect, since the simplified tax system uses the cash method, and income is recognized at the time of receipt of funds from the buyer.

To form a separate primary document that records the new cost of goods sold, you can use one of the printed forms that the program offers as part of commands called by button Seal:

- Cost change agreement;

- with status 2.

The printed form of the agreement (UCD) indicates the number and date of the adjustment, as well as the number and date of the initial certificate of service provision (UPD).

When choosing the type of operation Correction in primary documents in the document Implementation adjustments Printed forms of primary documents are available:

- Bill of lading (CAKE?12) with corrections made;

- Universal adjustment document (UCD) with status 2.

When automatically filling out a tax return under the simplified tax system for 2016, the adjustment made will be reflected in the indicators in Section 2.2.

Ten units of goods capitalized as a result of adjustment and actually disposed of by the buyer must be written off. Depending on the conditions of a particular business transaction, defective goods are written off either as other expenses, or as settlements for claims presented to the supplier, or as settlements with personnel for compensation for material damage.

Adjustment of sales from previous years

Now let's look at how adjustments to sales from previous years are reflected in accounting and tax accounting. Let's change the conditions of the previous example:

Example 2

In this case, on the tab Calculations document Implementation adjustments need to set a flag Last year's accounting is closed for adjustments (reporting has been signed) and indicate the item of other income and expenses, for example, Profit (loss) of previous years.

After completing the document Implementation adjustments With the specified settings, the following accounting entries will be generated:

Debit 41.01 Credit 91.01 - for the amount of other income identified as a result of adjusting the sale of goods (RUB 2,500.00); Debit 91.02 Credit 62.01 - for the amount of other expenses (RUB 5,000.00); Debit 62.01 Credit 62.02 - for the allocation of an advance received from the buyer (RUB 5,000.00).

The posting date corresponds to the document date Implementation adjustments(May 2017).

In tax accounting, compared to Example 1, nothing will change: in the register Book of income and expenses (section I) expenses for the purchase of goods recognized in the previous period are reversed, and in Section I of the report Book of income and expenses of the simplified tax system for 2016, the entry about the decrease in consumption is reflected in the last line. But, unlike Example 1, the declaration under the simplified tax system was submitted before adjustments made.

Because the expenses of the past are inflated tax period, and, therefore, the amount of tax is underestimated, then the organization is obliged to submit an updated declaration under the simplified tax system for 2016.

When automatically filling out an updated tax return, the adjustment made will be reflected in the indicators in Section 2.2.

For additional charge tax paid in connection with the application of the simplified tax system, in connection with the increase in the tax base that occurred as a result of corrections made to tax accounting, in the period when the error was discovered (in May 2017) you need to enter into the program accounting entry using document Operation:

Debit 99.01.1 Credit 68.12 - for the amount of additional tax (2,500.00 x 15% = 375 rubles).

Such an entry needs to be made only if the amount of tax calculated for the tax period in general procedure(taking into account the adjustments made) exceeds the minimum tax.

If the due amounts of taxes are paid on time later than those established by the legislation on taxes and fees, then the organization must independently calculate and pay penalties (clause 1 of Article 75 of the Tax Code of the Russian Federation).

Adjustment of expenses for the reporting year

Let's look at how in the 1C: Accounting 8 version 3.0 program you can correct a technical error made when registering a current year receipt document if the taxpayer uses a simplified taxation system with the object “Income minus expenses”.

Example 3

The costs of renting office space are reflected in the program using a document Receipt (act, invoice) with the type of operation Services (act). As a result of the document, accounting entries were generated:

Debit 60.01 Credit 60.02 - for the amount of the offset prepayment for the rental of the premises (RUB 200,000); Debit 26 Credit 60.01 - for the cost of renting the premises (200,000 rubles).

The amount of 200,000.00 is reflected in the register Book of income and expenses (section I) as an expense of the simplified tax system.

To reflect accounting errors made by the user when registering primary documents received from the supplier, we will use the document Adjustment of receipts, which we will generate based on the document Receipt (act, invoice).

Document form Adjustment of receipts on the bookmark Main varies depending on the selected type of operation, as well as on the period of making changes to the basis document.

According to paragraph 6 of PBU 22/2010, an error in the reporting year identified after the end of this year, but before the date of signing the financial statements for this year, should be corrected by entries in the corresponding accounting accounts for December of the reporting year. Therefore, in our case the document Adjustment of receipts should be dated December 2016 (field from).

On the bookmark Main in field Type of operation The following operations are available:

- Correction in primary documents;

- Adjustment by agreement of the parties;

- . This operation is intended to correct data entry errors made by the user when registering primary documents and (or) a received invoice, and allows you to correct erroneously entered invoice details, including totals. The correction refers to the same period as the incorrectly entered document itself.

Since, according to the conditions of Example 3, the organization’s accounting included a technical error, then you need to select the type of operation Correcting your own mistake(Fig. 3).

Rice. 3. Adjustment of receipts

Tabular part on the tab Services is filled in automatically according to the document specified in the field Base. In line after change You must indicate the corrected totals.

After completing the document Adjustment of receipts The following accounting entries will be generated:

Debit 60.02 Credit 60.01 - for the resulting amount of advance payment to the supplier (RUB 100,000.00), paid as a security payment; REVERSE Debit 26 Credit 60.01 - for erroneously inflating the cost of renting the premises (-100,000.00 rubles).

accumulation hysteres Book of income and expenses (section I) And Decoding KUDiR.

In the register Book of income and expenses (section I) the expense of the simplified tax system is reversed in the amount of 100,000.00 rubles, and in Section I of the report Book of income and expenses of the simplified tax system for 2016, a record of a decrease in consumption is automatically reflected in chronological order by document date Adjustment of receipts, that is, December 31, 2016.

Adjustment of expenses from previous years

To simplify accounting for taxes paid in connection with the use of the simplified tax system, the following mechanism for automatically adjusting tax accounting in the document is implemented in the 1C: Accounting 8 program, edition 3.0 Adjustment of receipts.

If errors (distortions) led to:

- to overstate the expenses of the previous tax period, then changes to the tax accounting data are made for the tax period to which these expenses relate. In this case, it is necessary to submit an updated declaration for the previous tax period;

- to understate expenses of the previous tax period, then changes to tax accounting data are made in the current period, that is, the date of adjustment. An adjusted return for the previous tax period is not required, but the program does not check whether there was a loss in the previous tax period.

According to these rules, if a sales adjustment was associated with an increase in the number of goods sold, then adjustments in tax accounting will always be made in the current period, regardless of the period of the changes.

It is necessary to keep in mind the following: if an error associated with understating expenses of the previous tax period is automatically corrected in the current period, but a loss is incurred in the current period or in the period to which the error relates, then the user will have to adjust the tax accounting data manually and submit an updated return for the previous tax period.

Example 4

To correct errors that led to overestimation of costs of the previous tax period, the document is also used Adjustment of receipts with the type of operation Correcting your own mistake. The difference is that the date of the foundation document and the date of the adjustment document refer to different years: in the field from document Adjustment of receipts indicate the date the error was discovered, for example, 05/22/2017.

After this, the document form Adjustment of receipts on the bookmark Main modified: in the area of details Reflection of income and expenses field appears Item of other income and expenses:. In this field you need to indicate the desired article - Profit (loss) of previous years by selecting it from the directory Other income and expenses.

The procedure for filling out the tabular part Services does not differ from the order described in Example 3.

After completing the document Adjustment of receipts accounting entries dated 05/22/2017 will be generated:

Debit 60.02 Credit 60.01 - for the resulting amount of advance payment to the supplier (RUB 100,000.00), paid as a security payment; Debit 60.01 Credit 91.01 - for the amount of other income identified as a result of adjusting last year’s receipts (RUB 100,000.00).

And in tax accounting for the purposes of the simplified tax system, the adjustments made are reflected as follows:

- in the accumulation register Book of income and expenses (section I) rental expenses recognized in the previous period are reversed;

- in Section I of the report Book of income and expenses of the simplified tax system for 2016, the entry about the decrease in consumption is reflected in the last line, and in the report Book of income and expenses of the simplified tax system for 2017 this adjustment does not apply;

- when automatically filling out an updated tax return under the simplified tax system for 2016, the adjustment made will be reflected in the indicators of Section 2.2.

Now let’s look at an example where expenses relating to the previous tax period increase.

Example 5

After completing the document Adjustment of receipts accounting entries will be generated:

Debit 60.01 Credit 60.02 - for the amount of the offset prepayment for the rental of premises (RUB 100,000); Debit 91.02 Credit 60.01 - for the amount of other expenses identified as a result of adjusting last year’s receipts (RUB 100,000.00).

For the purposes of the tax paid in connection with the application of the simplified tax system, corrective entries are entered in the re-

accumulation hysteres Book of income and expenses (section I), Decoding KUDiR And Expenses under the simplified tax system.

At the same time, in the register Book of income and expenses (section I) in the current period, rental expenses are reflected in the amount of RUB 100,000.00.

Accordingly, the specified amount is reflected in Section I of the report Book of income and expenses of the simplified tax system for 2017 as part of expenses taken into account when calculating the tax base. An updated declaration for 2016 is not required.

If documents of the type Implementation adjustments And Adjustment of receipts are not suitable for adjusting tax accounting data under the simplified tax system, then you should use the document Entry of the book of income and expenses (USN).

To enter an entry in Section I of the book of income and expenses, you need to manually fill out the tab I. Income and expenses, where you indicate information corresponding to similar fields of KUDiR - the date and number of the primary document, content, income and expenses taken into account when calculating the simplified tax system. You can also enter entries in Section II KUDiR using bookmarks II. Calculation of costs for purchasing an OS And II. Calculation of costs for the acquisition of intangible assets.

The simplified taxation system, despite its name, is far from easy to apply. Many problems arise when accounting for expenses: the closed list of expenses in Chapter 26.2 of the Tax Code sometimes creates many difficulties for accountants. When forming a simplified tax base, is it possible to take into account the costs of installing a program for electronic reporting, the costs of creating a website, and investments in landscaping? Svetlana Borisovna Pakhalueva, leading adviser to the department of special tax regimes of the Russian Ministry of Finance, helped us find answers to these and other questions.

Svetlana Borisovna, now the municipal authorities are ordering organizations to improve the territory, tidy up the flower beds, and plant flowers. Can such expenses be taken into account when calculating tax under the simplified tax system?

The list of expenses taken into account when determining the tax base under the simplified tax system by payers who have chosen income reduced by the amount of expenses as an object of taxation is established by paragraph 1 of Article 346.16 of the Tax Code. This list of expenses is closed. Costs associated with landscaping are not included.

So, organizations and entrepreneurs who are on the simplified tax system and who have chosen income reduced by the amount of expenses as an object of taxation do not have the right to take into account expenses for improving the territory as expenses when determining the tax base for the tax.

Is it possible to take into account the costs of installing a program for electronic reporting when forming the tax base?

When determining the object of taxation under the simplified tax system, payers reduce the income received by expenses associated with the acquisition of the right to use computer programs and databases under agreements with the copyright holder (according to license agreements) . These costs also include costs for updating computer programs and databases.

Accordingly, funds spent on installing a program for electronic submission of reports under agreements with the copyright holder may be included in the costs taken into account when determining the tax base for the tax paid in connection with the use of the simplified taxation system.

Question in continuation of the "electronic" topic. If a company using the simplified tax system with the object “income reduced by the amount of expenses” ordered services to create a website from a third party, can these expenses, as well as the costs of maintaining the site, be included as expenses?

It all depends on whether you have exclusive rights to the site or not, and whether the site can be classified as an intangible asset.

Organizations that apply the simplified tax system with the object of taxation “income reduced by the amount of expenses” reduce the income received by acquisition costs intangible assets, as well as the creation of intangible assets by the taxpayer himself.

Expenses for the acquisition of intangible assets during the period of application of the simplified tax system are taken into account from the moment these assets are accepted for accounting. The definition of the concept “intangible asset” is given in PBU 14/2007.

To account for the costs of creating a website as part of these costs, it is necessary that the site meets the criteria established in the PBU for classifying it as an intangible asset. At the same time, let me remind you that the company must have exclusive rights to the created third party the site and these rights must be documented. Subject to these conditions, the costs of creating a website are considered expenses for the acquisition of intangible assets.

When there are no exclusive rights, it should be borne in mind that for tax purposes under the simplified tax system, advertising costs for manufactured, purchased and sold goods, trademarks and service marks are taken into account. In this case, these costs are accepted in the manner prescribed for calculating corporate income tax in Article 264 of the Tax Code. An organization's advertising expenses include, in particular, expenses for promotional activities through means mass media(including advertisements in print, broadcast on radio and television) and telecommunication networks.

Thus, the costs of paying for an order for the development, creation and maintenance of a website intended for promoting services on the market and not owned by the taxpayer can be taken into account as expenses when determining the tax base for the tax paid in connection with the application of the simplified tax system, as advertising expenses.

A company using the simplified tax system purchases fixed assets for production needs. The facility was registered and put into operation in February 2010. Payment is made by installments. In what order is the cost of a fixed asset taken into account as an expense when calculating the single tax according to the simplified tax system?

Organizations using the simplified tax system, when determining the object of taxation, take into account, in particular, the costs of acquiring fixed assets.

Expenses for the acquisition of fixed assets are reflected on the last day of the reporting (tax) period in the amount of amounts paid. In this case, these expenses are taken into account only for fixed assets used in entrepreneurial activity.

Costs for the acquisition of fixed assets during the period of application of the simplified taxation system are taken into account from the moment these fixed assets are put into operation. During the tax period, expenses are accepted for reporting periods in equal shares.

In this regard, expenses for fixed assets put into operation in February 2010 and paid in installments can be taken into account when determining the tax base for the tax paid in connection with the application of the simplified tax system during 2010 in the amount of amounts paid.

E.N. Strelkova,

auditor of the company "Anesta Audit"

The list of expenses that reduce income received under the simplified tax system is reflected in paragraph 1 of Article 346.16 of the Tax Code. This list is closed, and there are no costs associated with landscaping the territory.

In addition, if the territory being improved belongs to the territory municipality, its improvement relates to the public legal responsibilities of local governments (Article 6 of the Federal Law of August 28, 1995 N 154-FZ). In our opinion, in this situation, the costs of improving the territory of the municipality are nothing more than the gratuitous performance of work (provision of services), the costs of which do not reduce the tax base (clause 16 of Article 270 of the Tax Code of the Russian Federation). In addition, these expenses do not correspond to expenses within the meaning of Article 252 of the Tax Code.

In what order can you take into account the costs of repairing a rented premises? Moreover, as part of the lease agreement, capital investments are also made in inseparable improvements (installation of air conditioning, installation of a computer network, etc.). The landlord does not reimburse the tenant for these expenses.

As I have already said, organizations that apply the simplified tax system with the object “income reduced by the amount of expenses”, when determining the object of taxation, reduce the income received by expenses associated with the acquisition, construction and production of fixed assets, as well as with the completion, additional equipment, reconstruction, modernization and technical re-equipment of fixed assets. Fixed assets include fixed assets that are recognized as depreciable property in accordance with Chapter 25 of the Tax Code.

Paragraph 1 of Article 256 of the Tax Code provides that depreciable property also includes capital investments in fixed assets leased in the form of inseparable improvements made by the tenant with the consent of the lessor.

Based on this cost capital investments in the form of inseparable improvements can be taken into account by the tenant as part of expenses when determining the tax base for the tax paid in connection with the application of the simplified tax system, on the basis of subparagraph 1 of paragraph 1 of Article 346.16 of the Tax Code, provided that the lease agreement does not provide for reimbursement of these costs by the lessor. These expenses are taken into account by the lessee from the moment the fixed assets are put into operation after the relevant work has been carried out. These expenses are reflected in tax accounting on the last day of the reporting (tax) period in the amount of amounts paid. In this case, these expenses are taken into account only for fixed assets that are used in business activities.

Svetlana Borisovna, a lot of questions also arise about the possibility of offsetting excess advance payments of tax paid in connection with the application of the simplified taxation system against the payment of the minimum tax. For example, 2009 ended with a loss. Minimum tax charged. At the same time, advance payments were made for the first quarter and half of 2009, but at the end of 9 months a loss was incurred. Can they be offset against the minimum tax for 2009?

The amount of overpaid tax is subject to offset against the taxpayer's upcoming payments for this or other taxes, repayment of arrears for other taxes, debts for penalties and fines for tax offenses or return in a certain order.

Offset of amounts overpaid federal taxes and fees, regional and local taxes is carried out for the corresponding types of taxes and fees, as well as for penalties accrued for the corresponding taxes and fees.

The tax paid in connection with the application of the simplified taxation system and the minimum tax relate to federal taxes.

Based on this, the amount of excess tax advances paid in connection with the application of the simplified tax system can be offset against the payment of the minimum tax.

At the same time, the offset of the amount of overpaid advance payments of tax paid in connection with the application of the simplified tax system against upcoming payments of the minimum tax must be carried out on the basis of a written application from the organization by decision of the tax inspectorate.

A.A. Zhigina,

senior lawyer at Pepelyaev Group

Recognition of expenses when calculating tax paid in connection with the application of the simplified tax system is possible subject to compliance with general requirements paragraph 1 of article 252 of the Tax Code to their economic feasibility and documentary evidence (clause 2 of article 346.16 of the Tax Code of the Russian Federation), but only after their actual payment (clause 2 of article 346.17 of the Tax Code of the Russian Federation).

Thus, in order to recognize expenses when calculating the tax paid in connection with the application of the simplified tax system, it is necessary to have the amounts issued by the supplier - to fulfill the requirements of paragraph 1 of Article 252 of the Tax Code, as well as the availability of payment documents - to confirm the fact of payment.

The absence of any of these documents does not allow reducing the income received by the corresponding amount of expenses.

General rules Clause 1 of Article 54 of the Tax Code obliges taxpayers who discover errors (distortions) when calculating the tax base of past periods to submit updated tax returns. The only exceptions are cases where it is impossible to determine the period for the occurrence of expenses.

Since the period for payment of expenses is always known to the taxpayer, then, in our opinion, if documents are received from the supplier in the next tax period, it is necessary to adjust the tax base previous period- exactly the one in which the payment took place.

How to fill out section 1 of the declaration under the simplified tax system, if in the first quarter of the year an organization applying the simplified tax system with an object in the form of income reduced by the amount of expenses received a profit, and at the end of the six months there was a profit, but in a smaller amount than at the end of the first quarter (since there was a loss in the second quarter)? A loss was incurred for 9 months of the year. At the end of the year, the company also made a loss and pays minimal tax.

According to the Procedure for filling out a tax return paid in connection with the application of the simplified tax system, in the case under consideration in section 1 of the declaration for 2009 on line 070 “Amount of tax to be reduced for the tax period”, the value of the indicator should be reflected on line code 040 “Amount of advance payment for tax , calculated for payment for half a year" (since in this case there is no value of the indicator for line code 050 "Amount of advance tax payment calculated for payment for nine months").

What if the company did not take into account expenses for 2009 using the simplified tax system due to the fact that there were no supporting documents, but the documents were received in April 2010? Is it possible not to submit an updated declaration under the simplified tax system, but to recognize expenses in the current period?

According to paragraph 1 of Article 54 of the Tax Code, if errors (distortions) are detected in the calculation of the tax base relating to previous tax (reporting) periods, in the current tax (reporting) period the tax base and tax amount are recalculated for the period in which these errors were made (distortions). If found in the submitted tax office declaration of the fact of non-reflection or incomplete reflection of information, as well as errors leading to an understatement of the amount of tax payable, the taxpayer is obliged to make the necessary changes and submit an updated declaration to the inspectorate.

Therefore, if in 2009 an organization did not take into account, when determining the tax base for the tax paid in connection with the application of the simplified tax system, the expenses provided for in paragraph 1 of Article 346.16 of the Tax Code due to the lack of supporting evidence, then upon receipt of such in 2010 after submitting a tax return for 2009 year, the organization must submit to the inspectorate an updated declaration for this tax for 2009.

Our readers often ask questions about the use of differentiated rates(for the object “income minus expenses”). For example, in 2009, activities were carried out for which a tax rate of 5 percent was in effect (based on the relevant regional law). In 2010, a second type of activity was added, to which the reduced rate does not apply. Is it possible to apply the lowest of tax rates?

Chapter 26.2 of the Tax Code does not provide for the application by one taxpayer of several tax rates established for individual categories payers. Also, the Tax Code does not specify a mechanism for accounting for income and expenses, as well as their distribution for the purposes of calculating the tax base for the tax paid in connection with the application of the simplified taxation system, when the taxpayer applies different tax rates.

In this regard, the Ministry of Finance of Russia sent a letter dated June 2, 2009 No. 03-11-11/96 to the executive authorities of the constituent entities of the Russian Federation, which states that “a taxpayer who is on a simplified taxation system with the object of taxation in the form of income, reduced by the amount of expenses, and having the characteristics of several categories of taxpayers, when applying the law of the subject Russian Federation, providing for different tax rates for such categories of taxpayers, has the right to apply the lowest of these tax rates."

At the same time, the Russian Ministry of Finance pointed out the need to bring it into line with Tax Code relevant laws adopted in the territories of the regions in order to exclude the possibility of applying different tax rates to one taxpayer.

Thank you, Svetlana Borisovna. Here is another question that worries taxpayers involved in intermediary services. An agent with an “income minus expenses” object provides intermediary services to the principal for the sale of goods. If the sale of goods occurred at a price lower than that stipulated by the intermediary agreement, is it possible to take into account the loss reimbursed to the principal as part of the expenses under the simplified tax system?

No. As I said above, the list of expenses taken into account when determining the tax base by organizations applying the simplified tax system with the object of taxation “income reduced by the amount of expenses” is established by paragraph 1 of Article 346.16 of the Tax Code and is closed.

Costs associated with compensation for losses to the principal due to the sale of goods agency agreement at a price lower than stipulated in this agreement, are not included in the above list of expenses.

Taxpayers-agents who are on the simplified tax system with the object of taxation “income reduced by the amount of expenses” do not have the right to take into account as expenses the costs associated with compensating the principal for losses due to the sale of goods under an agency agreement at a price lower provided for by the contract.

"Currency" question. If the “simplistic” person with the object “income” has foreign currency deposit, on which a certain amount of money is listed, is it necessary to re-evaluate its value and include the difference in value when calculating advance payments for single tax and when calculating tax for the year?

Article 346.17 of the Tax Code establishes that organizations, when applying the simplified tax system, use the cash method of accounting for income and expenses.

Chapter 26.2 of the Tax Code does not contain provisions defining the procedure for recognizing income and expenses in the form of positive and negative exchange differences under the simplified taxation system. Article 273 of the Tax Code, which establishes the procedure for recognizing income and expenses under the cash method, also does not contain provisions defining the procedure for recognizing income and expenses in the form of positive and negative exchange differences under the cash method.

Considering that the recalculation of property in the form of currency values into rubles is carried out in order to organize the accounting of income expressed in foreign currency, together with income, the value of which is expressed in rubles, and income in the form of positive exchange rate differences should in this case be taken into account as part of income under the simplified tax system on the basis of paragraph 1 of article 346.15 and paragraph 11 of article 250 of the Tax Code, for organizations applying the simplified tax system, income in in the form of positive exchange rate differences should be taken into account in the manner established in paragraph 8 of Article 271 of the Tax Code: on the date of transfer of ownership of transactions with currency values and (or) on the last date of the reporting (tax) period, depending on what happened earlier.

At the same time, it should be borne in mind that when applying the simplified tax system with the object of taxation in the form of income, expenses, including in the form of negative exchange rate differences, are not taken into account.

And finally, how to stop using the simplified system and switch back to general mode taxation if the company has submitted an application to switch to the simplified tax system since 2010?

In this case, there can be two situations. The first is when an organization submitted an application to switch to the simplified tax system, and then, before the start of its application, decided not to switch to this system taxation. The second situation arises when an organization has submitted an application to switch to a simplified taxation system and began to apply it. In both cases, it should be borne in mind that the organization applying the simplified tax system has the right to switch to a different taxation regime from the beginning calendar year. The tax authority must be notified of this no later than January 15 of the year in which the transition to a different taxation regime is expected.

At the same time, an organization that has submitted an application to switch to the simplified tax system from January 1, 2010 within the deadlines established by the Tax Code is considered to have switched to a simplified taxation system if all the conditions for the transition to the simplified tax system are met. If an organization decides not to apply this tax system, it has the right to switch to the general regime from January 1, 2010, by notifying the inspectorate of the change tax regime no later than January 15, 2010.

In the second case, the organization will have the right to switch to common system taxation only from January 1, 2011, notifying the tax office no later than January 15, 2011.

Conducted the conversation

N.V. Gorshenina,

Deputy Chief Editor,

tax consultant

1 sub. 19 clause 1 art. 346.16 Tax Code of the Russian Federation

2 subp. 2 p. 1 art. 346.16 Tax Code of the Russian Federation

3 subp. 2 p. 3 art. 346.16 Tax Code of the Russian Federation

4 approved by order of the Ministry of Finance of Russia dated December 27, 2007 N 153n

5 clause 3 PBU 14/2007

6 subp. 20 clause 1 art. 346.16 Tax Code of the Russian Federation

7 paragraph 4 art. 264 Tax Code of the Russian Federation

8 subp. 1 clause 1 art. 346.16 Tax Code of the Russian Federation

9 subp. 4 p. 2 tbsp. 346.17 Tax Code of the Russian Federation

10 clause 3 art. 346.16 Tax Code of the Russian Federation

11 clause 4 art. 346.16 Tax Code of the Russian Federation

12 subp. 4 p. 2 tbsp. 346.17 Tax Code of the Russian Federation