2016-09-06 3507 6 Often, when providing loans to organizations, banks are asked to provide data on the status of the organization’s receivables and payables. To collect such information in a convenient form, this report was made. The report discloses receivables and payables (balance sheet lines 1230 and 1520) by counterparties and contracts, determining the date the debt arose. The report also displays information about the date of planned repayment of the debt (taken from the term of the contract), for which specific works and services the debt arose (comment from the contract), and also determines the nature of the debt: current or overdue. To do this, the validity period of the contract is compared with the date of the report - if on the date of generation of the report it has expired, but the debt remains, then it is considered overdue. Selections in the report by date and organization.

How to view accounts receivable in 1C correctly?

To return Money you need to send a letter to within two weeks from the date of purchase See also: This report displays summary information for the period on the amount of revenue (with and without VAT), the amount of VAT, cost and profit by organization, counterparties, items, contracts and documents sales 2015-09-03 3120 0 Summary report on all expenses of the enterprise for a certain period (accounts 20,25,26,44) broken down by month showing the percentage change in the amount compared to the previous month (according to this analytics) 2016-06- 05 2105 0 The module allows you to configure the automatic sending of letters to e-mail according to arbitrary rules with the ability to attach printed forms of documents.

Program 1c: accounts receivable and payable

Federal Law No. 119-FZ dated July 22, 2005 determines the procedure for inclusion in tax base funds received to repay accounts receivable that arose before January 1, 2006, as well as the procedure for deducting amounts of value added tax presented by the supplier and unpaid before January 1, 2006. Thus, the use of a standard configuration reporting mechanism allows for systematic monitoring and analysis of mutual settlements with buyers and suppliers, obtaining the necessary data to assess the status of receivables and payables and timely accept necessary actions to optimize it, improve performance financial condition, and also allows you to comply with the requirements of constantly changing legislation. Implementation Center "Domino Soft" tel.

Accounts receivable and payable in 1s 8.3 accounting

Filling out a bookmark Accounts receivable according to the example: Filling out the Accounts payable tab according to the example: On the Settlement accounts tab, enter a list of accounting accounts for which we carry out an inventory: An example of filling out the Inventory bookmark is shown in the figure: Making a bookmark Inventory commission according to the example: Step 4. Let's take a closer look at the accounts receivable for account 60. Let's create a balance sheet for account 60 in the section Reports - Standard reports - Account balance sheet: Let's assume that the supplier "SERVICE" LLC did not fulfill the terms of the contract, and upon expiration limitation period accounts receivable were rightfully recognized as uncollectible and written off against the formed reserve for doubtful debts.

Accounting for receivables and payables in "1s:accounting 7.7"

On subaccount 60.02 in the “debit” column there will be accounts receivable - “how much we are owed.” Reconciliation reports generated for suppliers will completely coincide with the received data. Another way to find out information about counterparties is to create a table within the “Purchasing Management” or “Sales Management” interface.

Here you need to select “Mutual settlements with counterparties” - “Debt due to counterparties”. You can also request the contract number, but there will be no turnover for the period - only data for a certain date. It is important to note that the data in this table may not coincide with the reconciliation report.

This is due to the peculiarities of documentation. If data on the receipt of inventory items is entered into the program by a storekeeper, and the “posting” is carried out by an accountant, then these several hours or days between operations can lead to a discrepancy in the final figures.

Decoding of accounts receivable and payable (to the bank)

Table 2 Counterparty Agreement (invoice) Amount Computer store Invoice No. 19 dated 01/10/2005 4,161.90 Manufactory S/f No. 122 dated 01/04/2005 S/f No. 65 dated 02/24/2005 15,000.0026 379.00 Textiles plus Invoice No. 55 dated 01/18/2005 243,836.59 Telephone installation S/f No. 2005/2 dated 02/25/2005 858.00 Garment factory Agreement No. 2 dated 01/05/2004 Agreement No. 8 dated 01/10/2005 3,900.0010,000.00 Total: 30 3,896 .09 Based on this information, we can conclude that the existing accounts receivable are not enough to cover accounts payable. Even if buyers transfer funds to the company’s accounts, this amount will not cover accounts payable and the company will need to find additional sources working capital to repay debts to suppliers. Accounts receivable are among the most quickly realized current assets.

The details “Date of occurrence of the obligation” and “Date of repayment of the obligation” are used to divide debt into long-term, short-term and overdue debt when preparing regulated reporting. The type of agreement is indicated so that in specialized reports it is possible to group information about settlements with counterparties by type (Fig. 2). Rice. 2 We will use the “Account balance sheet” report to perform the tasks of accounting for receivables and payables.

In the report settings, select account 62.1, select “Counterparties” in the “Subaccount Type 1” field, and “Agreements” in the “Subaccount Type 2” field. This setting will allow you to see in the generated report opening balances, turnover and final balances of mutual settlements with customers by accounts (agreements).

How to decipher accounts receivable in 1c

Let's fill out the header of the document:

- in the line Type of operation we indicate Debt write-off;

- In the Write off line we indicate the buyer's debt.

Let's fill in the Buyer's debt (accounts receivable) tab:

- Using the Fill button, we will fill in the balances for mutual settlements, and we will fill out the tabular part automatically:

Fill in the Write-off account tab:

- in the line Account we indicate the account 91.02;

- in the line Other income and expenses we indicate Write-off of receivables (payables):

To reflect bad debt on the balance sheet in 1C 8.3, we create a document Transactions entered manually in the section Transactions - Accounting - Transactions entered manually. An example of creating a document is shown in the figure: Step 6.

Ministry of Finance dated October 31, 2000 No. 94n). Login to OSV is possible through:

- menu “Desktop” - “SALT by account” (select from the list);

- menu “Purchases and sales” - “Standard reports” - “SALT by account” (select from the list).

Read more about such a report as SALT in the article “Turnover balance sheet - sample filling out 2017-2018”. By clicking the “Show settings” button in the report form that opens, you can generate a report as you wish in the following sections:

- groupings - by counterparties, contracts, settlement documents (for example, issued invoices);

- selection - from the groups listed above, you can select only the counterparties of interest;

- indicators - for example, by expanded balance (convenient for those partners who can have both debit and credit balances at the same time).

- Reconciliation report with the counterparty.

If the buyer has a debt at the end of the period, then we can see on which account (agreement) it was formed. If, when analyzing mutual settlements, you do not need to expand turnover by accounts (agreements), then in the report settings, the “Type of subaccount 2” field should be left blank. In this case, the report will reflect general mutual settlements with the buyer without taking into account invoices (agreements) (Table.

1). Table 1 Counterparty Agreement (account) Amount Scalper Account No. 1 dated January 11, 2005 64,530.04 PE Smolyakov Main agreement 22.00 Total: 64,552.04 By specifying account 60.1 in the report settings, we will receive information on the status of mutual settlements with suppliers, on end of period available accounts payable for the following counterparties (see Table 2).

In our world, it is rare that an actively operating enterprise does not have a group of counterparties who owe a certain amount. The natural question would be “How can I look at these debtors in 1C?” Some accountants who have a question about debtors try to find specialized processing or a report in the 1C interface for selecting data on receivables from counterparties. However, the 1C program, in the Accounting configuration, does not have such a tool.

“What to do”: - naturally, the interested reader will say. Let's hasten to calm him down. Of course, such a multifunctional accounting program as 1C Enterprise includes many different scalable tools that allow you to perform a lot of tasks. And information on receivables from counterparties will be no exception.

We will conduct the review in the well-known configuration of 1C Accounting for Ukraine.

First, let's look at the subject area. Let's determine where the information about current receivables for products (goods, work, services) is actually stored. “Instructions for using the Chart of Accounts accounting assets, capital, liabilities and business transactions enterprises and organizations" to account for these funds allocates an account “Settlements with buyers and customers”. Moreover, the sub-account is used for settlements with domestic buyers” - “Settlements with foreign buyers”, 363 “Settlements with PFG participants”, 364 “Settlements for guarantee collateral”.

The debit of account 36 “Settlements with buyers and customers” reflects sale price products sold, goods, work performed, services provided (including for the implementation of barter contracts), which includes VAT, excise taxes and other taxes, fees ( obligatory payments), to be transferred to budgets and extra-budgetary funds and included in the sales price, for a loan - the amount of payments received to the enterprise's accounts in banking institutions, to the cash desk, and other types of payments. The account balance reflects buyers and customers for the products (work, services) received.

So, based on what was described and quoted above, it is enough to determine the balance of the account or subaccount we need in accordance with the counterparty or in general for the organization. This can be done both in the “Turnover Balance Sheet” (SBV) report and using the “” report. So, as we looked at managing the first report, let’s turn to the SALT for the account.

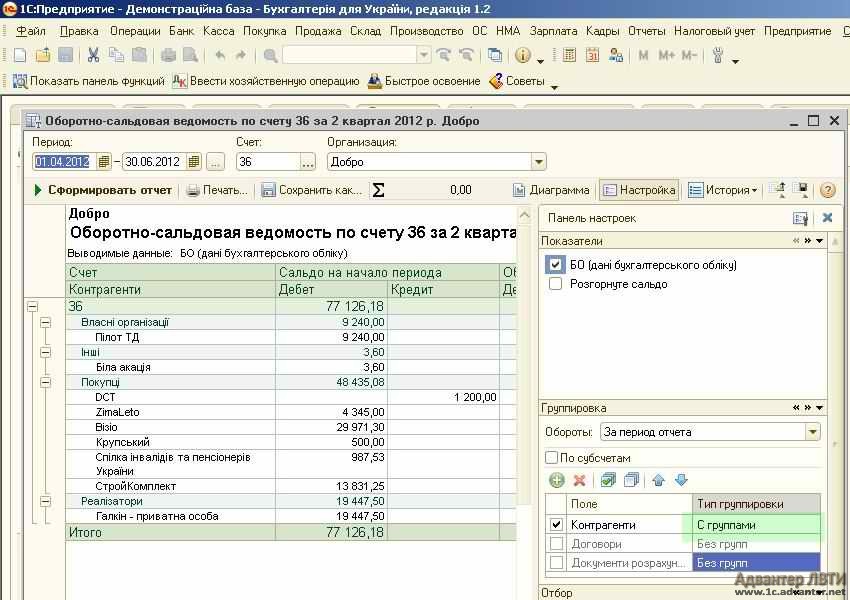

To generate this report, open the 1C main menu item “Reports” and select the subitem of the same name “Account balance sheet”. In the statement that opens, select account 36. To be fair, we note that you can also go to this point in generating the report by selecting the “SALT for account 36” link on the “Sales” tab of the function panel.

So, let's indicate the required period, organization and 36 account. If it is necessary to make a selection of settlements in accordance with the type of counterparties, then you can specify the subaccounts of account 36.

Having finished selecting the parameters, click the “Generate report” button. After a short time, a list of counterparties will be displayed, grouped by all subaccounts of the account.

In general, at this point the creation of SALT for account 36 “Settlements with buyers and customers” can be considered completed. But we will also look at the report’s capabilities in terms of more precise management, grouping and selection of data.

If you look in the upper right corner of the report form, you will notice a menu where the “Chart”, “Settings” and “History” buttons are available. By clicking the “History” button, you can select saved versions of previously used parameters. Clicking on the “Diagram” button will, after rearranging the data, display information in a visual form.

Let’s take a closer look at the capabilities that become available by clicking on the “Settings” button. After this action, an additional panel will open with the parameters “Indicators”, “Grouping” and “Selections”.

For example, let’s create a visual report with grouping only by counterparties. To do this, just uncheck the two unnecessary subaccounts in the “Grouping” panel. We only leave a checkmark next to counterparties. And click the report generation button.

If you select the “With groups” option for counterparties in the “Grouping type” column, the data will be sorted by counterparty groups.

If we need information on a specific counterparty, we need to add a selection by counterparty. This is done in the “Selection” section.

If we need information on a specific counterparty, we need to add a selection by counterparty. This is done in the “Selection” section.

By clicking the “Print” button, the generated statement can be printed to a printer.

This is how the report “Turnover balance sheet for account” 36 or for its subaccounts is generated. We have considered the basic principles of management; in a similar way, manipulation and grouping is carried out according to other parameters, be it, for example, contracts or settlement documents counterparties.

For documentation accounts receivable, there are documents and “Inventory of settlements with counterparties”. Access to them is simplified; these documents are located at the bottom of the “Sale” tab, on the function panel.

Let us note, in the context of the raised topic “How to look at debtors in 1C?” that the solution is another solution from the 1C company - “Management manufacturing enterprise» (UPP) has significantly greater capabilities for working with accounts receivable management.

If you have any difficulties, we will definitely help.

You can discuss the operation and ask questions about it at.

Leave your name and phone number, an operator will contact you during business hours within 2 hours.

I want to receive news about promotions, discounts and events from 1C:Franchisee Victoria

The program has various ways debt analysis. For example, you can use the following tools:

If you need to analyze the debt for accounting purposes, you can create the document “Settlements Inventory Act” for the required date (Section Purchases or Sales - Settlements with counterparties - Settlements Inventory Acts). In the document, the Accounts Receivable and Accounts Payable tabs are filled in using the accounting data collected on settlement accounts with counterparties. From the document you can print the “Act of Inventory of Settlements with Buyers, Suppliers and Other Debtors and Creditors.”

If it is necessary to analyze debt for purposes tax accounting, then you should create a tax accounting register “Receivables and payables” (Section Reports – Income Tax – Tax accounting registers – 3. Registers for recording the status of a tax accounting unit – 3.10 Accounts receivable and payable).

The generated report is shown in the figure. In the report settings, you can select the type of debt Receivable or Payable.

A convenient tool for analyzing debt simultaneously for both accounting (AC) and tax accounting (TA) purposes is the standard “Subconto Analysis” report (Section Reports – Standard reports – Subconto Analysis).

In addition, the report allows you to evaluate settlements with counterparties by agreement. To build a report in the context of counterparties and contracts, you need to specify the subconto: Counterparties and Contracts in the report settings (the “Show settings” button) on the “Types of subaccount” tab.

By clicking on the Send button, I consent to the processing of personal data

Hotline with professional consultants without waiting.

Questions and answers to frequently asked questions.

1C courses. Schedule, programs and costs of upcoming courses.

Budget accounting. Information about our proposals for servicing budgetary institutions.

Articles and advice on 1C. A series of publications of interesting articles dedicated to 1C.

Programs

Regions

Product

Statistics

The rights to the information in the sections "UPP Help", "BP Help" and "ZUP Help" belong to 1C (http://1c.ru)

Rights to information in the section " Practical experience"belong to Mutovkin A.M.

Document "Inventory of settlements with counterparties"

Document "Inventory of settlements with counterparties"

Purchase (Sale) ® Inventory of settlements with counterparties

The document is intended for conducting an inventory of settlements with counterparties.

The purpose of the inventory of settlements with customers, suppliers, other debtors and creditors is to verify the validity of the amounts listed in the accounting accounts.

When entering a document, the bookmarks are filled in:

On the bookmark Accounts receivable information on the results of the accounts receivable inventory is filled in:

Accounts receivable amounts are filled in automatically using the button Fill - Fill accounts receivable

On the bookmark Accounts payable information about the results of the accounts payable inventory is filled in:

Accounts payable amounts are filled in automatically using the button Fill - Fill accounts payable. When filled automatically, all debt is considered confirmed by counterparties.

On the bookmark Settlement accounts a list of accounting accounts is indicated for which an inventory of settlements is carried out. By default, the list is filled with all accounts for settlements with counterparties.

On the bookmark Additionally the details of the order to carry out an inventory of calculations and the composition of the inventory commission are indicated.

Document Inventory of settlements with counterparties is not reflected in accounting and tax accounting, however, based on the inventory results, it is possible to carry out transactions to write off debt for which the statute of limitations has expired. To write off debt, you should use the Debt Adjustment document.

For document Inventory of settlements with counterparties The following printed forms are provided.

The program has various ways to analyze debt. For example, you can use the following tools:

If you need to analyze the debt for accounting purposes, you can create the document “Settlements Inventory Act” for the required date (Section Purchases or Sales - Settlements with counterparties - Settlements Inventory Acts). In the document, the Accounts Receivable and Accounts Payable tabs are filled in using the accounting data collected on settlement accounts with counterparties. From the document you can print the “Act of Inventory of Settlements with Buyers, Suppliers and Other Debtors and Creditors.”

If it is necessary to analyze the debt for tax accounting purposes, then you should create a tax accounting register “Accounts receivable and payable” (Section Reports – Income Tax – Tax accounting registers – 3. Registers for recording the status of a tax accounting unit – 3.10 Accounts receivable and payable).

The generated report is shown in the figure. In the report settings, you can select the type of debt Receivable or Payable.

A convenient tool for analyzing debt simultaneously for both accounting (AC) and tax accounting (TA) purposes is the standard “Subconto Analysis” report (Section Reports – Standard reports – Subconto Analysis).

In addition, the report allows you to evaluate settlements with counterparties by agreement. To build a report in the context of counterparties and contracts, you need to specify the subconto: Counterparties and Contracts in the report settings (the “Show settings” button) on the “Types of subaccount” tab.

In the process of carrying out the activities of an enterprise, the need arises to take into account mutual settlements with debtors and creditors. Correct reflection in the accounting of receivables and payables is exclusively important, since the amounts of balance sheets for these debts and the turnover periods of each of them affect the assessment of the financial condition of the organization. In addition, in some cases, debt analysis is also necessary for fiscal purposes.* E.V. talks about debt management in the Accounting configuration (rev. 4.5) for 1C:Enterprise 7.7. Baryshnikova, head of the Domino Soft training center.

Note:

* Let us recall that Federal Law No. 119-FZ dated July 22, 2005 requires an inventory of receivables and payables for the calculation and deduction of VAT in transition period, read more.

Debt control

The main task of any commercial organization is to make a profit, therefore the financial services and management of the enterprise are faced with the question of reducing accounts receivable and payable, high level which can reduce financial stability enterprises.

Monitoring the movement of receivables and payables is necessary to improve settlement and payment discipline. An important factor control is the turnover of receivables and payables.

High accounts receivable turnover reflects an improvement in the payment discipline of buyers (as well as other counterparties) - timely repayment by buyers of debt to the enterprise and (or) a reduction in sales with deferred payment (commercial loans to buyers). The dynamics of this indicator largely depends on credit policy enterprises, on the effectiveness of the control system, ensuring timely receipt of payment.

A high turnover of accounts payable may indicate an improvement in the payment discipline of the enterprise in relations with suppliers, the budget, off-budget funds, personnel of the enterprise, other creditors - timely repayment by the enterprise of its debt to creditors and (or) reduction of purchases with deferred payment (commercial credit from suppliers).

The immediate tasks of accounting for receivables and payables include the following:

- accurate, complete and timely accounting of cash flows and cash flow transactions;

- control over compliance with cash and payment and settlement discipline;

- determining the structure of accounts payable and receivable by maturity, by type of debt, and by the degree of justification of the debt;

- determination of the composition and structure of overdue receivables and payables, its share in the total volume of receivables and payables;

- identifying the structure of data on suppliers for unpaid settlement documents, suppliers for overdue bills of exchange, suppliers for received commercial loans, establishing their feasibility and legality;

- identification of the volume and structure of debt on bills of exchange, on claims, on advances issued and received, on property and personnel insurance, debt arising as a result of settlements with other debtors and creditors, debt on bank loans etc. Determination of the causes of their occurrence and possible ways to eliminate them;

- determining the correct use of bank loans;

- identification of incorrect transfer or receipt of advances and payments on non-commodity accounts, etc. operations;

- determining the correctness of settlements with employees for wages, with suppliers and contractors, with other debtors and creditors and identifying reserves for repaying existing debt under obligations to creditors, as well as possibilities for collecting debts (through monetary or non-monetary settlements or going to court) from debtors.

Analysis of the movement of receivables and payables in the standard configuration "1C: Accounting 7.7" is possible using the reporting mechanism. Using the reporting mechanism, the user has the opportunity to analyze the status of receivables and payables for the selected period. Using the example of the demonstration base included in the program delivery, we will illustrate the use of the reporting mechanism to assess the status of receivables and payables.

In accordance with the Chart of Accounts for accounting the financial and economic activities of an organization and the Instructions for its application, receivables and payables can be reflected in the accounts:

- 60 "Settlements with suppliers and contractors";

- 62 "Settlements with buyers and customers";

- 63 “Provisions for doubtful debts”;

- 66 "Calculations according to short-term loans and loans";

- 67 “Settlements for long-term loans and borrowings”;

- 70 “Accounting for settlements with personnel for wages”;

- 71 "Settlements with accountable persons";

- 73 “Settlements with personnel for other operations”;

- 75 “Settlements with founders”, subaccount 1 “Settlements for contributions to the authorized capital”;

- 76 "Settlements with various debtors and creditors";

- and etc.

In accordance with the Instructions for using the chart of accounts, analytical accounting for account 60 “Settlements with suppliers and contractors” is maintained for each supplier or contractor, as well as for each invoice submitted by them. Analytical accounting for account 62 “Settlements with buyers and customers” is carried out for each invoice presented to buyers (customers), and in the order of payments by scheduled payments - for each buyer and customer.

For correct reflection accounts receivable and payable in financial statements it is necessary to divide debt into long-term and short-term.

Let's turn to the chart of accounts of the standard configuration "1C: Accounting 7.7". In account 60 “Settlements with suppliers and contractors”, analytical accounting is maintained for suppliers and contractors (sub-account “Counterparties”) and the basis of settlements (sub-account “Agreements”). Each supplier and contractor is an element of the Contractors directory. Each calculation basis is an element of the "Contracts" directory. Analytical accounting for account 62 “Settlements with buyers and customers” was constructed in a similar way. Analytics for the account as a whole is carried out by buyers and customers (sub-account “Counterparties”) and the basis of settlements (sub-account “Agreements”). Each buyer (customer) is an element of the “Counterparties” directory. Each calculation basis is an element of the "Contracts" directory. This setup of a standard configuration chart of accounts fully complies with the requirements of the Chart of Accounts for accounting the financial and economic activities of an organization (Fig. 1).

Rice. 1

The division of debt into short-term and long-term is carried out in the “Agreements” directory. This directory stores information about invoices for payment issued to the counterparty, invoices for payment received from the counterparty and long-term contracts with the counterparty. The details “Date of occurrence of the obligation” and “Date of repayment of the obligation” are used to divide debt into long-term, short-term and overdue debt when preparing regulated reporting. The type of agreement is indicated so that in specialized reports it is possible to group information about settlements with counterparties by type (Fig. 2).

Rice. 2

Let's use the "Account balance sheet" report to perform the tasks of accounting for receivables and payables. In the report settings, select account 62.1, in the "Subaccount Type 1" field, select "Counterparties", in the "Subaccount Type 2" field - "Agreements". This setting will allow you to see in the generated report the initial balances, turnover and final balances of mutual settlements with customers broken down by accounts (agreements). If the buyer has a debt at the end of the period, then we can see on which account (agreement) it was formed. If, when analyzing mutual settlements, you do not need to expand turnover by accounts (agreements), then in the report settings, the “Type of subaccount 2” field should be left blank. In this case, the report will reflect general mutual settlements with the buyer without taking into account invoices (agreements) (Table 1).

Table 1

By specifying account 60.1 in the report settings, we will receive information on the status of mutual settlements with suppliers; at the end of the period there are accounts payable for the following counterparties (see Table 2).

table 2

Based on this information, we can conclude that the existing accounts receivable are not enough to cover accounts payable. Even if buyers transfer funds to the company’s accounts, this amount will not cover accounts payable and the company will need to find additional sources of working capital to repay debts to suppliers.

Accounts receivable are among the fastest-selling current assets. However, when assessing the possibility of converting receivables into cash, the proportion of bad debts must be taken into account. Determination of the share of bad debts is usually carried out using data from previous periods using the method percentage unpaid bills to their total volume. Let's calculate this share using the data of the current period as a planned value for the next planning period.

The total amount of accounts receivable is RUB 290,762.04. The unpaid amount of receivables is RUB 64,552.04. Percentage of outstanding debt to total amount - 22 %.

Thus, according to the “Turnover balance sheet for account 62.1” we can conclude that 22% of the total amount of receivables remains unpaid at the end of the period and it would be advisable to create a reserve for doubtful debts* for the next planning period.

Note:

* Read about how to do this.

One of the most important points in managing receivables and payables is control over the payment schedule (repayment of receivables and payables) and compliance with settlement and payment discipline. Let's use the report "Turnover between sub-accounts" in order to obtain information about how accounts payable were repaid during the planning period. The report "Turnover between sub-accounts" allows you to analyze the turnover between one or all sub-accounts (analytical sections or objects) of one type, and one or all subcontos (analytical sections or objects) of another type. in this case we will analyze the turnover between the subconto “Counterparties” and the subconto “Types of cash flows”. To do this, in the report settings, in the "Subconto Type" (main) field, select - "Counterparties"; in the "Type of subconto" (corresponding) field, set - "Cash flow", and in the "Subconto" field, additionally select "Payment to supplier". In the generated report, we see the amounts of repayment of accounts payable for all creditors, as well as the procedure for repayment - through a current account, a foreign currency account and through a cash desk. If in the report settings, instead of “Type of cash flow” - “Payment to supplier”, specify - “Receipts from buyers”, then in the report we will see from which buyers the funds were received for current accounts and to the cash desk of the enterprise (Fig. 3).

Rice. 3

In addition to this information, you can build a "Diagram" report, which is a visual analysis tool and can be used by the head of the organization, managers and other specialists who are not directly related to accounting services. In setting up the report on the "Data" tab, we will indicate the account 60.1, select the type of totals - closing balances, credit, amount, and on the "Diagram" tab we will set the parameters necessary for generating the report (Fig. 4). For better clarity, we will create a “Diagram” for the counterparty “Garment Factory”.

Rice. 4

The diagram shows that at the beginning of the planning period, the accounts payable of the Sewing Factory counterparty increased sharply, then was partially repaid, but at the end of the period there is a balance of outstanding debt. Debt repayment occurred unevenly and the balance of debt is carried over to the next planning period. This indicates ineffective work on accounts payable accounting and the need to develop a payment schedule.

Inventory

One of the necessary means for accounting for receivables and payables is inventory.

Inventory is carried out, as a rule, at the end of the planning period and makes it possible to identify the balances of receivables and payables. Carrying out an inventory allows you not only to obtain information for making management decisions, but also for correct accounting of taxes.

In connection with the entry into force Federal Law dated July 22, 2005 No. 119-FZ:

|

In the standard "Accounting" configuration, the report "Inventory of settlements with counterparties" is intended for this purpose (Reports - Specialized - Inventory of settlements with counterparties). The report can be generated either using the unified form INV-17 “Act of Inventory of Settlements with Buyers, Suppliers and Other Debtors and Creditors”, or in a free form.

To generate a unified INV-17 form, you must check the "Use unified form INV-17". On the same tab, the following data is indicated that will be entered into the printed form: number and date of drawing up the act, chairman and members of the commission.

The accounts receivable table can be filled in automatically using accounting data by clicking the "Fill" button. When filling automatically, the debt in the table is reflected either as confirmed or as expired statute of limitations.

The fact that the statute of limitations for the debt has expired is determined using the contract requisite “Date of repayment of the obligation” (3 years must pass from the date on which the debt must be repaid). The “Not confirmed” column is not filled in automatically; it must be filled in manually.

The table for accounts payable is filled out in the same way.

To generate a custom form, you must uncheck the "Use unified form INV-17" checkbox.

In the “Debt type” attribute, indicate the type of debt of the counterparties that the report will reflect. There are three options to choose from:

- accounts receivable and accounts payable;

- accounts receivable;

- creditor.

We will generate this report in any form by selecting the debt type - “receivables and payables”. Let's establish the accounts for which the inventory is carried out - 60 and 62 (see Fig. 5)

Rice. 5

As can be seen from the report, the company has receivables and payables that are subject to repayment in subsequent periods.

Federal Law No. 119-FZ dated July 22, 2005 determines the procedure for including in the tax base funds received to repay accounts receivable that arose before January 1, 2006, as well as the procedure for deducting amounts of value added tax presented by the supplier and unpaid before January 1, 2006.

Thus, the use of a standard configuration reporting mechanism allows for systematic monitoring and analysis of mutual settlements with buyers and suppliers, obtaining the necessary data to assess the status of receivables and payables and timely take the necessary actions to optimize it, improve financial performance indicators, and also allows you to constantly comply with requirements changing legislation.