The estimate is part of the working documentation. It is necessary for any construction, any work. The estimate determines how much money the construction site needs. How many are needed to complete the job? In the article, we tried to tell how the estimate is filled out, where to get the data for this? What are indices and ratios? What is the estimated cost? Everything is not as difficult as it seems.

How can this article help?

The article will help to understand the issue a little. Understand budgeting at an elementary level. Here only general concepts on the composition of the estimate, examples of estimates for installation. A little about indices and coefficients. Details on budgeting for are discussed in MDS 81-35. 2001.

Title page

Consider how to read estimates, using an example. The estimate for the installation of a split system (table in the figure below) contains 13 columns. There are other types of forms that differ in the number of columns. But the principle is similar everywhere and the information in the graphs is similar. The position numbers of the text below correspond to the numbers in the picture of the estimate example. An example of an estimate for installation was compiled for this article and is not tied to any specific object.

1. At the top left is the block - "Agreed". It lists the contractor. The one who does the work. The organization and data of the head are indicated. Here is his signature and seal.

2. At the top right there is a block - "Approve", containing the position, surname, initials and signature of the head of the customer. The “Approve” block is also stamped.

3. Name of construction site - place of performance of work. Several parts of work can be combined in one construction site.

4. Number of estimate. By regulatory documents The following numbering order has been adopted:

- the first 2 digits are the number of the section of the summary estimate calculation;

- the second and third are the line number in its section;

- the third and fourth are the number of the estimate in this object estimate.

In the example, the estimate number is not set. It is not included in any documentation.

5. Name of the object, works and costs. Description of works with indication of the name and address of the object.

6. Foundation. What was the estimate based on? It could be a drawing technical task. We indicate, for example, a technical task.

7. Estimated cost of work. Estimated amount for installation work written in thousands of rubles. The indication of the amount in thousands of rubles is regulated by MDS 81-35.2001.

8. Funds for wages. How much should workers be theoretically paid?

9. Normative labor intensity. The sum of man-hours, excluding downtime, required to complete the work.

10. Rationale estimated cost. The estimate of the example is made in current (forecast) prices for the 1st quarter of 2018 (but there is monthly indexation). All prices are recorded in 2001 prices and then converted to current period prices using coefficients. This method is called the base-index method.

Tabular part of the estimate of an example estimate for the installation of a split system

The estimate header includes columns:

1. Quote number.

2. Code and number of the standard. Indicates in which standards the estimate was drawn up and by what order this regulatory framework operates. IN this case the FER directory is used (federal single construction rates). The numbers in the price title mean the numbers: collection - section - price table.

3. Name of works, costs and price unit. The work itself is described (in the same way as it is written in the price), the price meter (in this case, 1 split system). Further, in the name of the price, coefficients for positions and position indices are written.

4. Quantity. The quantity is affixed, taking into account the price meter. In this example, this is one split system.

Unit cost (block 1). This block includes the current base price and its elements.

5. Total / salary.

6. Operation of machines / including wages (drivers).

7. Materials.

Total cost (block 2). It is obtained by multiplying the unit cost by the quantity.

9. Pay.

10. Operation of machines / including wages (drivers).

11. Materials.

Labor costs of workers (block 3) not related to machine maintenance, pers. hour.

12. Per unit.

There is also a breakdown of the budget into sections. There are no strict rules. Break down logically. A section is always summed up.

What do the numbers in the spreadsheet mean?

The method of compiling the budget under consideration is the base-index one. The prices in it are indicated at the price level of 2001 and are called base. To convert prices to the current level, the base price is multiplied by the index. Direct prices cannot be immediately converted to the current price level, since there is no index for them. There are indexes for cost elements. The estimate is made in cost elements.

There are four in total:

- wages of workers - OZP;

- operation of machines - EM;

- remuneration of machinists - ZPM;

- Cost of materials.

Where in the table to look for direct costs:

Where to look for cost elements in the table:

As in the FER 20-06-018-04 standard, cost elements are spelled out. Here you can also see which materials are included in the price, and which remained unaccounted for.

Therefore, in order to find out the real price of the work, it is necessary to multiply the prices of the cost elements of 2001 by the indices and sum them up. If the "Materials" column is filled in the price, it means that this amount of materials is in the price unit. This can be seen in the example of the price for installing a split system (line No. 1). There are materials that are not included in the price. Then they are called unaccounted for and fit on a separate line(positions 3 to 9 of this estimate).

Estimated coefficients

In addition to indices, there are coefficients. They are charged on the elements of unit prices. They are indicated in column 3. The coefficients may be different (for wooden structures, for earthworks, for dismantling, for work in winter conditions ...). All of them can be found in magazines, collections of prices and in MDS 81-35.2001. The coefficients are charged on the elements of unit prices. They can be both lowering (for example, for dismantling) and increasing (for example, constraint).

At the end of the estimate, all costs are summed up. In this option for filling out the estimate, the line of costs in 2001 prices comes first. Then a line with current prices, where all price indexes are taken into account. Then comes the column - "Labor costs".

Next two lines:

- SP (estimated profit).

- HP (overhead).

The coefficients for them are indicated in the prices. You can learn more about the calculation of the joint venture from MDS 81-25.2001, and about the calculation of HP - from MDS 81-33.2004.

After the "Total" section is broken down into cost elements.

There are unforeseen expenses.

If there are sections in the estimate, then the totals of the estimates are made up of the totals of the sections.

At the end, signatures are put and deciphered:

Compiled by (engineer full name).

Checked (engineer full name).

Estimated documentation is one of the most important elements in the design of any structure or system and, as a rule, in design organizations there are even whole special departments involved in budgeting.

The very concept of estimated cost arose even during the planned economy and, in fact, was the equivalent of the construction price, but one should not think that in a market economy this concept has become irrelevant, although the functions of the estimated cost have changed, but the need for it remains, and the role even to some extent increased, this is due to the fact that the estimate documentation is a guideline for setting the contract price for the customer and the contractor, and in this role is necessary for optimal planning and cost analysis for both parties, as well as for intermediate cash settlements between them.

The estimated cost of construction is the planned amount of expenses necessary to create an object in strict accordance with the project. Based on the full estimated cost, allocation is made capital investments by years of construction, determined sources of financing, negotiated prices for construction products are formed.

It should be noted that when concluding a work contract, estimate documentation is not mandatory, only a protocol of agreement on the contract price is required. However, the customer has the right to request estimate documentation in any form, with any degree of detail, and most customers usually use this right in practice, especially if the customer is a government organization.

Estimated documentation, covering the entire complex of objects under construction, is called "summary", since it usually summarizes the documentation for individual objects. If it covers only a specific object or part of it (type of work), it is called "objective" or "local", respectively. An estimate document, which is calculated without detailed detail using aggregated indicators, is usually referred to as an "estimate calculation". If a detailed calculation of the cost is made according to working drawings without enlargement, then the resulting document is usually referred to as an "estimate".

The estimated cost is established at each design stage, in connection with which its phased detailing and refinement is ensured.

At the pre-project stage, when compiling the "Investment Feasibility Study", on the instructions of the investor, the preliminary (estimated) cost of construction is determined . It is compiled according to extremely aggregated indicators (per 1 hectare of reclaimed land, per 1 m3 of construction volume, per 1 m2 of living space, etc.), because there is no project at this stage yet. In the absence of such indicators, data on the cost of analogue objects can be used.

At the "project" stage, enlarged, but more accurate estimates. They are based on the drawings of this design stage and include the "Consolidated construction cost estimate", object and local estimates, cost estimates for certain types works, including survey and design (compiled prior to the start of these works), etc. For several types of construction (and, accordingly, several sources of financing), a "Summary of costs" is also compiled by type of construction (for example, hydro-reclamation, industrial, housing, etc. .).

The basis for estimates at this stage, as noted, is project documentation and the current estimate and normative base of 1991, or prices of 1984. with the introduction of appropriate correction factors. With absence estimated standards individual rates are used, compiled specifically for such cases.

On the stage " working documentation"(RD) are compiled objective and local estimates, and SNiP 11.01-95 allows them not to be drawn up, if this is not provided for in the contract for the implementation of the design documentation.

IN market conditions The Russian Federation uses four methods for calculating the estimated cost:

resource

Resource index

Basis-index

Basic compensatory

The resource method is a calculation in current (forecast) prices and tariffs of resources (cost elements). With this method, the costs of materials and products, the time spent on the operation of machines, the labor costs of workers are set separately in natural measurements (m3, ton, piece, man-hour, etc.), and the prices for these resources are taken current (for time of budgeting). Normative indicators of material consumption (NPRM) are used as a regulatory framework. This method allows in the future to fairly accurately recalculate the estimated cost for new prices.

The resource-index method is a combination of the resource method with a system of resource price indices. Price indices are the ratio of current prices to base prices. As noted, the prices as of January 1, 1991 are accepted as base prices, and it is permissible to use the prices of 1984. with amendments.

The base-index method is the use of a system of current and forecast price indices in relation to the value determined at the base level or the level of the previous period. Unlike the resource-index method, a separate determination of resource consumption in natural terms is usually not done. Reduction to current prices is carried out by multiplying the basic cost for each line of the estimate by the corresponding index.

The basis-compensation method consists in the fact that the basic cost is determined taking into account the expected changes in prices and tariffs, and during the construction process it is specified depending on the actual changes in these prices and tariffs.

Choice of compilation method budget documentation legislation is not regulated and is carried out in each specific case, depending on the terms of the agreement (contract) and the general economic situation. The most promising is the resource and resource-index methods, however, at present, the basic-index method prevails in construction.

The estimated cost of construction and installation works is divided into three main parts:

Direct costs

Overheads

Estimated profit (planned savings)

Direct costs include the cost of materials, products, the cost of operating machines and mechanisms, the wages of workers. They are determined on the basis of estimated norms and prices, volumes of structures or types of work, i.e. any of the above calculation methods.

Overhead reflects the costs associated with creating general conditions construction industry, i.e. include expenses for the organization, management and maintenance of the construction site. They are determined most often as a percentage of direct costs in accordance with federal overhead standards, or according to the individual standards of a particular construction organization. It is also possible to determine them using a system of indicators of overhead costs by types of construction and installation works or aggregated indicators for the main types of construction.

Estimated profit (planned savings) is the amount of funds necessary to cover expenses not directly related to this construction, but necessary for the further functioning of the construction organization. These are the costs of paying taxes, developing production and its infrastructure, providing material incentives and providing favorable living conditions for workers. Estimated profit is usually defined as a percentage of the total costs or labor costs of workers (for example, 50% of labor costs or 12% of the estimated cost of work). For this, industry-wide standards are used or individual norms specific organization.

The estimated cost of individual facilities and types of work included in the summary estimates for industrial and civil construction is determined according to price lists, according to estimates for standard and reusable economical and individual projects, tied to local construction conditions, and in their absence - according to estimates drawn up according to working drawings.

At the same time, it must be borne in mind that for unique buildings and structures, as well as for objects, the construction of which will be carried out according to experimental or for the first time individual projects using standard design solutions, standard structures and parts (for which there are no list prices and cannot be be used estimates for previously developed projects for similar buildings and structures), the estimated cost is determined by the estimates for the technical project, drawn up, as a rule, according to the consolidated estimated norms (USN), and only in exceptional cases, in the absence of consolidated estimated norms - according to unit rates on construction works, entered into force on January 1, 1969, and price tags for the installation of equipment, entered into force on January 1, 1972, and for technical working projects - according to estimates drawn up according to working drawings.

The cost of certain types of construction (general construction) special (plumbing, electrical, etc.) and general area (vertical planning of the territory, landscaping, etc.) works, as well as certain types of costs (according to an organized recruitment of workers, compensation in connection with the withdrawal of land for development and etc.) are calculated according to the estimate f. No. 3.

Agreed and accepted contractor before the start of construction of facilities, the estimated cost of construction and installation works, determined in summary estimate on the basis of object estimates f. No. 2, as well as estimates and estimates for certain types of work and costs (f. No. 3) ", is final and is not subject to clarification at the stage of development of working drawings, serves as the main document for settlement between the contractor and the customer for the work performed.

The estimated cost of the equipment required for the facilities under construction and the costs associated with its installation are reflected in the estimate f. No. 4, for housing and civil construction.

Since in f. No. 4 amount wages for installation work is calculated for each item of the estimate by calculation and is labor-intensive work, then from January 1, 1973 it was established new order wage determination. So, when drawing up estimates for electrical work, the amount of wages is determined using coefficients from the estimated cost of these works, calculated at the prices of sections 1-6 and 16-24.

The use of these coefficients makes it possible to link wages (basic and for the operation of machines) to local conditions of work. Estimated cost increase electrical work due to increased salary due to difficult local conditions for performing work, is determined by the following formula: Ds \u003d C x (P-1) x K

Expenses should always be planned! It is for this purpose that estimates are drawn up, which reflect preliminary cost items.

Without this document, which can be adjusted more than once, it is impossible to properly organize expenses.

What is this document for?

First of all, the estimate is a preliminary layout of the costs that are necessary for any event.

Even a simple business meeting is not complete without it! And it is right:

Even a simple business meeting is not complete without it! And it is right:

- estimate makes it possible to foresee all expenses;

- with her help subtracted those costs that can be dispensed with;

- she helps identify the causes of deviations in expenses incurred as a result of the past event.

IN general view an estimate is a document that lists the types of expenses, indicates their monetary value item by item and the total cost of spending is displayed. In addition, the estimate additionally provides information on the nature and scope of the necessary work.

Any strict unified form does not exist for budgeting.

Therefore, enterprises develop this form themselves, based on the federal law"On Accounting" No. 402-FZ and guided by its requirements for the details of primary documents. But this may not be done, since the estimate is not - it is only a cost plan that needs to be approved by order for the enterprise. Therefore, it can be presented in any form. Confirmation of the costs themselves according to the estimate will serve precisely source documents- , etc.

However, the estimate itself serves as an indirect confirmation of the costs - their target orientation. To do this, when drawing up an estimate document in its title event is indicated to which the transferred expenses are related. For example, "Estimates for servicing negotiations on the supply of goods." Such a link helps to correctly classify costs and attribute them to accounting accounts, and accept them for tax accounting purposes.

In what cases is it made up?

estimate is always drawn up and in any enterprise, regardless of legal form and form of ownership, as well as the type of its activity:

estimate is always drawn up and in any enterprise, regardless of legal form and form of ownership, as well as the type of its activity:

- for any types of events that the company plans to organize for its own non-production needs (for example, a corporate holiday) and for production needs (for example, a business meeting to conclude a contract);

- for any types of work or services that the enterprise is going to perform in relation to its consumer.

In the second case, the budget document bears official confirmation:

- the volume and types of work that are implemented under the contract;

- finished product or other end result;

- the time it takes to achieve the end result.

In the case of drawing up an estimate for an event, its purpose is to list future expenses and indicate the reason for their occurrence. Those. for which payment is made.

For example, for participation in negotiations of an interpreter, banquet services, delivery of guests to a meeting place, etc. But very often in this type of estimates there is a line “Source of payment”, which indicates the source of financing for the event.

Usually, necessity this arises:

- when the event is held by several companies at once and the estimate indicates the amount of those expenses that each of them agrees to pay;

- if the event is organized by the city, and its payment is made from different sources - sponsors, which can even be a private person;

- if, on the contrary, the event is held by a company, but the source of funding is state, regional or municipal budget, etc.

If you have not yet registered an organization, then easiest way do it with online services, which will help you generate all the necessary documents for free: If you already have an organization, and you are thinking about how to facilitate and automate accounting and reporting, then the following online services come to the rescue, which will completely replace an accountant in your enterprise and save a lot money and time. All reporting is generated automatically, signed electronic signature and sent automatically online. It is ideal for an individual entrepreneur or LLC on the simplified tax system, UTII, PSN, TS, OSNO.

Everything happens in a few clicks, without queues and stress. Try it and you will be surprised how easy it got!

Compilation rules

The estimate is made by person or persons who are appointed for this purpose by order of the enterprise. As a rule, those who are responsible for organizing and holding the event are appointed in this capacity. And, as soon as this order is issued, they begin to draw up the estimate itself.

The composition of the costs included in the estimate, in some cases, may be regulated. For example, very often hospitality expenses are indicated by name and fixed in. But basically the list of expenses depends on the nature of the event and usually changes several times before being finally approved.

As for the sources of income, if they need to be indicated, they usually appear after the preparation of the cost estimate, which is approved by all investor participants.

The hardest part about budgeting is cost estimate. That is why, after the main types of expenses are indicated, the best options implementation of these costs.

For example, for banquet services, the following are provided:

- renting a hall and organizing lunch there with the involvement of restaurant services;

- room rental directly in the restaurant;

- use of the enterprise hall with the involvement of catering services from the restaurant (i.e. with a visit to the customer).

In the first two cases, organizing a banquet will require transport, and this is another expense item. And in the case of catering services, all delivery to the destination is carried out at the expense of the restaurant.

To decide which option is better, they call all the good restaurants in the city and transport companies and compare the cost of their services, choosing the most profitable proposition. This is how other cost items are defined. Therefore, usually the preparation of estimates is delayed not for one day or even for one week.

Once the estimate is ready, she submitted for approval the head of the company or the person who is in charge of the finances of the company. And after him - to the top management. For the final approval of the estimate, a comparative report for each item of expenditure is often attached to it. This report clearly shows why such an option and such a cost was chosen.

After reviewing the estimate, it is either approved by order or sent for revision with comments.

When approving the budget the order appoints persons who are entrusted with the functions of performing specific types of work provided for in the estimate. For example, in the text of the order, it may look like this: “Assign Ivanov V.V. Responsible for organizing banquet services. In addition, the order must indicate from which sources the financing of one or another part of the estimate comes from.

When approving the budget the order appoints persons who are entrusted with the functions of performing specific types of work provided for in the estimate. For example, in the text of the order, it may look like this: “Assign Ivanov V.V. Responsible for organizing banquet services. In addition, the order must indicate from which sources the financing of one or another part of the estimate comes from.

What costs are included in the event budget?

Conventionally, all estimated costs can be divided into two parts:

- main

- these are the costs that are associated with the direct organization and holding of the event:

- rental of premises or territory for the event itself and for banquet services;

- transportation costs - for the transportation of guests to and from their destination, equipment, industrial designs, etc.

- banquet service itself (coffee break, business lunch, breakfasts, treats for spectators, etc.);

- Internet, electricity and communications - these costs may not be included in the rent;

- remuneration of own employees and non-staff personnel participating in the event or helping to organize and conduct it;

- decoration of a room or a platform for receiving guests;

- awards, bonuses or other remuneration;

- production of printing - business cards, programs, invitations, and more;

- loading and unloading operations;

- consumables - stationery, etc.

- overheads - These are costs that are associated with the event, but without which it would be possible to do without. For example, souvenirs, flowers, etc.

The composition of all these costs depends on the nature of the event and its scale. In addition, a certain percentage of unforeseen expenses is necessarily added to any estimate so as not to get out of the plan. Its size is also individual.

Compilation methods

Index Method- in the calculation, normative indicators are used, which are adjusted for the current price index. This method can be used provided that there are exact standard costs. As a rule, they are provided for construction purposes.

Index Method- in the calculation, normative indicators are used, which are adjusted for the current price index. This method can be used provided that there are exact standard costs. As a rule, they are provided for construction purposes.

analog method- when prices are taken from estimates for similar events. But this method is approximate, which means that there is a risk of not meeting the estimate.

resource method is based on planning expenses based on the real cost of each type of expenses and the subsequent summation of the estimates obtained. It is this method that is used most often: it provides accurate and up-to-date information about the total cost of the event.

When compiling budget for sporting events important to point out:

- type of competition;

- date and place of its holding;

- accommodation of participants in a hotel;

- rental of sports equipment;

- medical care during the competition.

When planning expenses to a festive event(any) in the estimate reflect:

- the cost of gifts and treats - for this, the number of guests by invitation must be known;

- the cost of the concert - the services of invited artists, equipment and venue rental, etc.

- protection of the event;

- festive decoration.

When preparing the budget with hospitality important to point out:

When preparing the budget with hospitality important to point out:

- accommodation of business partners, if they are from other cities;

- technical support of the meeting room;

- business lunch;

- copying works and translation services.

In general, any estimate at a commercial enterprise, as a document, consists of:

At budget organizations everything is more complicated - they can spend funds only on those areas that are provided for in Article 70 of the Budget Code of the Russian Federation. Those. for the remuneration of public sector employees, for their business trips, payment for goods and services for state needs, for taxes and fees, and compensation for damage caused budget institution in the course of their activities. The estimates reflect only these costs based on fiscal year! In addition, the estimate itself is compiled according to the rules and in the form approved by the Ministry of Finance of the Russian Federation in its Order No. 112n dated November 20, 2007.

Performance report

This report is required to identify deviations from the planned level of expenses and their reasons, and for the transfer to the accounting department of all documents confirming the expenses for the purpose of their further acceptance for accounting.

What is a cost estimate and how to draw it up correctly is described in the following video:

Before any expenses are incurred, they are almost always planned. In fact, the determination of approximate amounts directed to certain cost items is the preparation of estimates upcoming expenses. Moreover, this may concern both the solution of everyday issues in human life, and, to an even greater extent, the activities of enterprises and organizations. Almost everyone is involved in cost planning in one form or another.

Determining the cost estimate

The cost estimate is usually understood as the calculation of all the costs necessary to carry out the planned work, release the product, implement activities related to the achievement of the intended goals of the organization and other similar situations. Sometimes the drafting of a document is done on a voluntary basis. However, quite often the development of cost estimates, as well as its subsequent approval and approval, are a requirement of Russian legislation. For example, drawing up a balance of expenses and income (which is a kind of cost estimate) is one of the prerequisites for the work of any non-profit organization. Considering that their number is quite large, it becomes clear why so much attention is paid to the issue of how to make a cost estimate correctly and as accurately as possible.

Non-profit organizations (NPOs) include:

- educational (university, kindergarten or school), cultural (museum, national park or exhibition) medical (polyclinic, dental center, etc.) public and private institutions;

- HOA, housing construction and consumer cooperatives;

- organizations for the protection of the rights of citizens;

- bodies of local and state administration;

- charitable foundations and organizations;

- religious associations;

- subdivisions of the Ministry of Defence, the Ministry of Emergency Situations and the Ministry of Internal Affairs.

For all of the above organizations, it is necessary to draw up an annual cost and income estimate, as well as a final document containing information on its implementation. Particularly stringent requirements are imposed on state public institutions that are partially or fully funded from the budget. In this case, the entire procedure for drawing up is clearly prescribed, starting from the timing of the development of the document in question and ending with the requirements for its approval and approval.

Scope of the cost estimate

Considering a large number of non-profit organizations, examples of which were given above, it becomes clear the relevance of the issue of competent preparation of cost estimates and their subsequent implementation. In many ways, the quality of these processes determines the level and degree of control over the distribution of a significant part of state budget. It is not surprising that those non-profit organizations are regulated and controlled in the most detail, in the financing of which there are budgetary funds to one degree or another.

At the same time, one should not forget that cost estimates are compiled not only where there is public funding. As an example, we can cite a situation that almost everyone had to face in real life. The level of costs for utility bills in houses that are managed by the HOA is determined, among other things, by drawing up an estimate of costs for next year, as well as analysis of the execution of the document developed in the past calendar period.

In this case, the cost estimate should not only be as accurate as possible, which is important for residents of the house who do not want to overpay, but also accessible and easy to check. It is no secret that some representatives of public utilities prefer to deliberately complicate the calculations performed - it is much easier to confuse payers and present them with larger than necessary amounts for payment.

An equally important area of application of cost estimates is their preparation in commercial organizations, in particular, at industrial enterprises of any form of ownership. In this case, the purpose of issuing a document is usually the calculation of the cost of manufactured products, which is necessary to determine the selling price. Obviously, in today's market conditions, the importance of the competent implementation of this process is difficult to overestimate.

Cost Estimate Example

As noted above, the highest requirements for the preparation of cost estimates are imposed on budgetary institutions. Therefore, it would be logical to consider specific example such a calculation, since the implementation of other options in most cases is much simpler.

As such a simple example, we can cite a variant of the completed estimate of expenses and income of a non-profit organization.

The document consists of two main parts. The first of them indicates the sources of income generation, and the second - the directions of their spending with a clear indication of the amounts by cost items and programs being implemented and distribution by quarters. As a result, after studying the estimate, a clear idea is created as the main parameters of the organization's activities for the planned calendar period.

As can be seen from the above example, the design, approval and approval of the document in question is carried out in an arbitrary form. The requirements for the preparation of an estimate of expenses and income by a budgetary institution are much higher, the form and an example of filling out are given below.

Regulatory acts clearly prescribe the form of the document, its structure, as well as how to draw up a cost estimate in such a way that it corresponds to the current Russian legislation. The header of the document looks like this:

The calculation part of the document consists of four sections: the first three contain data on the main expenses of the organization, which are summarized in the final fourth.

In this example, there are no costs for the second and third sections, so the final one practically repeats the data of the first section in a slightly modified format. The cost estimate is signed by those who compiled it, checked it and the head of the budgetary institution.

Estimates play an important role in planning and design work. Without it, it will not be possible to launch any serious project. Especially often, budgeting is resorted to in the construction industry. Of course, to draw up an estimate correctly is not an easy task, which only specialists can handle. But they also have to resort to different software, often paid, for this task. But, if you have a copy of Excel installed on your PC, then it is quite possible to make a high-quality estimate in it, without buying expensive, narrowly focused software. Let's see how to do this in practice.

A cost estimate is a complete list of all expenses that an organization will incur in the implementation of a specific project or simply for a certain period of time of its activity. For calculations, special normative indicators are used, which, as a rule, are available in open access. The specialist should rely on them when compiling this document. It should also be noted that the estimate is compiled at the initial stage of the project launch. Therefore, this procedure should be taken especially seriously, since it is, in fact, the foundation of the project.

Often, the estimate is divided into two large parts: the cost of materials and the cost of performing work. At the very end of the document, these two types of expenses are summed up and subject to VAT if the company that is the contractor is registered as a payer of this tax.

Stage 1: start compiling

Let's try to make the simplest estimate in practice. Before proceeding with this, you need to receive a technical task from the customer, on the basis of which you will plan it, and also arm yourself with reference books with standard indicators. Instead of directories, you can also use Internet resources.

Step 2: drafting Section I

- In the first row of the table we write the name . This name will not fit in one cell, but there is no need to push the boundaries, because after that we will simply remove them, but for now we will leave them as they are.

- Next, we fill in the estimate table itself with the names of materials that are planned to be used to implement the project. In this case, if the names do not fit in the cells, then we move them apart. In the third column we enter the amount of a specific material necessary to perform a given amount of work, in accordance with applicable standards. Next, specify its unit of measurement. In the next column, write the price per unit. Column "Sum" do not touch until we fill the entire table with the above data. Values will be displayed in it using a formula. We also do not touch the first column with the numbering.

- Now let's place the data with the quantity and units in the center of the cells. Select the range in which this data is located, and click on the already familiar icon on the ribbon "Align Center".

- Next, we will number the entered positions. To a column cell "No. p / p", which corresponds to the first name of the material, enter the number "1". We select the element of the sheet in which it was entered given number and set the pointer to its lower right corner. It transforms into a fill handle. Hold down the left mouse button and drag down, inclusive, to the last line, which contains the name of the material.

- But, as you can see, the cells were not numbered in order, since all of them contain the number "1". To change this, click on the icon "Fill Options", which is at the bottom of the selected range. A list of options opens. Move the switch to position "Fill in".

- As you can see, after that the line numbering was set in order.

- After all the items of materials that will be required for the implementation of the project are entered, we proceed to the calculation of the amount of costs for each of them. As you might guess, the calculation will be the multiplication of the quantity by the price for each position separately.

Set the cursor to a column cell "Sum", which corresponds to the first name from the list of materials in the table. We put a sign «=» . Next, in the same line, click on the sheet element in the column "Quantity". As you can see, its coordinates are immediately displayed in the cell for displaying the cost of materials. After that, from the keyboard we put the sign "multiply" (* ). Next, in the same row, click on the element in the column "Price".

In our case, we got the following formula:

But in your specific situation it may have other coordinates.

- To display the result of the calculation, press the button Enter on keyboard.

- But we only displayed the result for one position. Of course, by analogy, you can enter formulas for the remaining cells of the column "Sum", but there is an easier and faster way using the fill handle we talked about above. We put the cursor in the lower right corner of the cell with the formula and after converting it into a fill marker, hold down the left mouse button and drag down to the last name.

- As you can see, the total cost for each individual material in the table is calculated.

- Now let's calculate the total cost of all materials combined. We skip the line and in the first cell of the next line we make an entry "Total by materials".

- Then, with the left mouse button pressed, select the range in the column "Sum" from the first name of the material to the line "Total by materials" inclusive. Being in the tab "Home" click on the icon "Autosum", which is located on the ribbon in the toolbox "Editing".

- As you can see, the calculation total amount costs for the purchase of all materials for the performance of work produced.

- As we know, monetary expressions indicated in rubles are usually used with two decimal places after the decimal point, meaning not only rubles, but also kopecks. In our table of values sums of money are represented exclusively by whole numbers. In order to fix this, select all the numeric values of the columns "Price" And "Sum", including the final row. We make a right-click on the selection. The context menu opens. Select an item in it. "Cell Format...".

- The formatting window is launched. Moving to tab "Number". In the parameter block "Number Formats" set the switch to position "Numerical". On the right side of the window in the field "Number of Decimals" number must be set "2". If this is not the case, then enter the desired number. After that, click on the button OK at the bottom of the window.

- As you can see, now the price and cost values are displayed in the table with two decimal places.

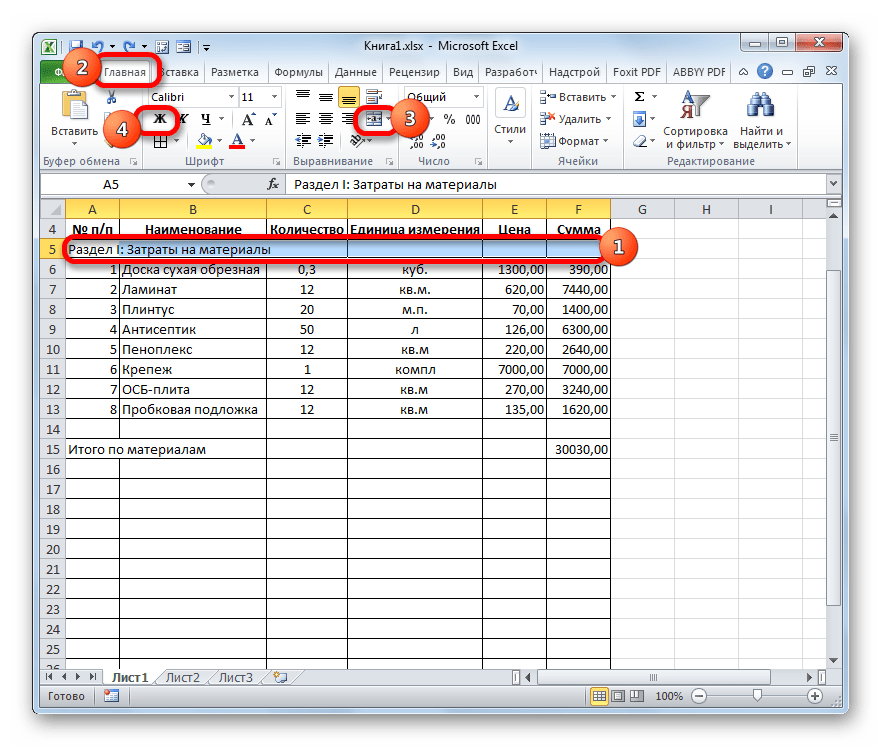

- After that, we will work on appearance this part of the budget. Highlight the line containing the name "Section I: Material Costs". Located in the tab "Home", click on the button in the block "Ribbon Alignment". Then we click on the icon we already know "Bold" in the block "Font".

- After that we go to the line "Total by materials". Select it all the way to the end of the table and click on the button again "Bold".

- Then again we select the cells of this line, but this time we do not include the element in which the total amount is located in the selection. Click on the triangle to the right of the button on the ribbon "Merge and Center". Select an option from the drop-down list of actions "Merge Cells".

- As you can see, the elements of the sheet are combined. At this point, the work with the material cost section can be considered completed.

Step 3: drafting Section II

We proceed to the design of the estimate section, which will reflect the costs of performing direct work.

Stage 4: calculation of the total cost

- Skip the line after the last entry and write in the first cell "Total for the project".

- After that, select a cell in the column in this line "Sum". It is not difficult to guess that the total amount for the project will be calculated by adding the values "Total by materials" And "Total cost of work". Therefore, in the selected cell we put the sign «=»

, and then click on the sheet element containing the value "Total by materials". Then we set the sign from the keyboard «+»

. Next, click on the cell "Total cost of work". We have a formula like this:

But, of course, for each specific case, the coordinates in this formula will have their own form.

- To display the total cost per sheet, click on the button Enter.

- If the contractor is a value added tax payer, then add two more lines at the bottom: "VAT" And .

- As you know, the amount of VAT in Russia is 18% of the tax base. In our case, the tax base is the amount that is written in the line "Total for the project". Thus, we will need to multiply this value by 18% or 0.18. We put in the cell that is at the intersection of the line "VAT" and column "Sum" sign «=»

. Next, click on the cell with the value "Total for the project". Type the expression from the keyboard "*0.18". In our case, we get the following formula:

We click on the key Enter to calculate the result.

- After that, we will need to calculate total cost works, including VAT. There are several options for calculating this value, but in our case it will be easiest to simply add the total cost of work without VAT with the amount of VAT.

So in the line "Project total including VAT" in a column "Sum" add cell addresses "Total for the project" And "VAT" in the same way that we summed up the cost of materials and labor. For our estimate, the following formula is obtained:

Click on the button ENTER. As you can see, we have received a value that indicates that the total cost of the project implementation by the contractor, including VAT, will be 56533.80 rubles.

- Next, we will format the three final lines. Select them completely and click on the icon "Bold" tab "Home".

- After that, to make the totals stand out from other information in the estimate, you can increase the font. Without deselecting a tab "Home", click on the triangle to the right of the field "Font size", which is located on the ribbon in the toolbox "Font". From the drop-down list, select a font size that is larger than the current one.

- Then select all the total rows up to the column "Sum". Being in the tab "Home" click on the triangle, which is located to the right of the button "Merge and Center". Select an option from the dropdown list "Combine by Rows".

Stage 5: finalization of the estimate

Now, to complete the design of the estimate, we only need to make some cosmetic touches.

After that, the design of the estimate in Excel can be considered complete.

We have considered an example of compiling the simplest estimate in the Excel program. As you can see, this spreadsheet has all the tools in its arsenal in order to perfectly cope with this task. Moreover, if necessary, much more complex estimates can be made in this program.